|

|

|

|

|||||

|

|

|

McCormick & Company, Incorporated MKC reported fourth-quarter fiscal 2025 results, wherein both top and bottom lines missed the Zacks Consensus Estimate, while both increased from the year-ago period’s actuals.

Adjusted earnings of 86 cents per share improved from 80 cents in the year-ago quarter. The metric missed the Zacks Consensus Estimate of 87 cents per share. The increase was driven by elevated operating income, lower adjusted effective tax rate and interest expense.

McCormick & Company, Incorporated price-consensus-eps-surprise-chart | McCormick & Company, Incorporated Quote

The global flavor leader generated net sales of $1,850.4 million, up 3% year over year, including a 1% positive currency impact. The top line misses the consensus mark of $1,859 million. Organic sales rose 2%, led by growth in both the Consumer segment and the Flavor Solutions segment.

The gross profit for the quarter was $720.3 million compared with $722.2 million recorded in the prior year, while the gross margin contracted 130 basis points to 38.9%. The adjusted gross margin contracted 120 basis points, stemming from elevated commodity costs, tariffs and costs to support increased capacity for growth. These were partly compensated by savings from McCormick’s Comprehensive Continuous Improvement (“CCI”) program.

Adjusted operating income increased 3% to $316.6 million and included a 1% impact from currency. On a constant-currency basis, adjusted operating income increased 2%, driven by lower selling, general and administrative (SG&A) expenses resulting from reduced employee-related benefit costs and cost savings from the CCI program, including SG&A streamlining initiatives. These gains were partially offset by lower gross profit, continued brand marketing investments and higher technology investments.

Consumer: The segment’s sales advanced 4% year over year to $1,127 million, including a 1% positive currency impact. Organic sales grew 3%, backed by a 2% increase in price reflecting tariff and inflation-related pricing actions, and a 1% increase in volume and product mix. Adjusted operating income rose 1% to $231 million, with minimal impact from currency. The increase was driven by higher sales and lower SG&A expenses, partially offset by higher commodity costs and tariffs.

Flavor Solutions: Sales rose 2% to $723 million, including a 1% favorable impact from currency. Organic sales grew 1%, driven by a 2% contribution from pricing, partially offset by a 1% decline in volume and product mix. Adjusted operating income increased 7% to $86 million, 6% on a constant-currency basis. The increase was driven by elevated sales and lower SG&A expenses, partially offset by higher commodity costs and tariffs.

McCormick ended the quarter with cash and cash equivalents of $95.9 million, long-term debt of $3.11 billion and total shareholders’ equity of $5.77 billion.

In the 12 months ended Nov. 30, 2025, net cash provided by operating activities was $962.2 million. The company continues to expect robust cash generation for fiscal 2026, supported by profit and working capital initiatives, and aims to return a significant portion to its shareholders via dividends.

The company expects net sales growth of 13-17% (12-16% in constant currency or cc) in fiscal 2026, indicating sustained volume growth, pricing actions and a significant contribution from the McCormick de Mexico acquisition.

Adjusted gross margin is expected to expand, implying recovery from 2025, with favorable impacts from organic sales growth, accretion from McCormick de Mexico and benefits from the company’s CCI program, partially offset by higher commodity costs. SG&A expenses are expected to be impacted by cost headwinds, including digital transformation initiatives, the build back of incentive compensation and continued growth investments. These impacts are expected to be partially offset by benefits from the company’s CCI program, including SG&A streamlining initiatives.

Adjusted operating income is projected to rise 16-20% (up 15-19% at cc).

The company expects adjusted EPS between $3.05 and $3.13, indicating 2-5% year-over-year growth or 1-4% growth at cc.

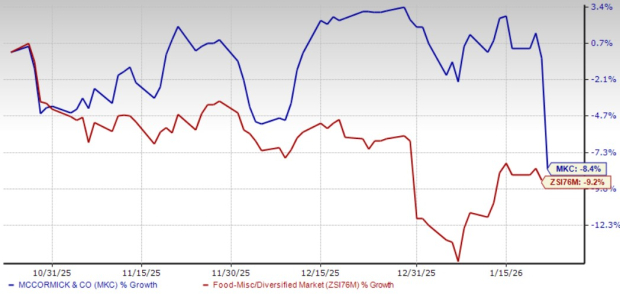

This Zacks Rank #2 (Buy) company has lost 8.4% in the past three months compared with the industry’s decline of 9.2%.

United Natural Foods, Inc. UNFI distributes natural, organic, specialty, produce and conventional grocery and non-food products in the United States and Canada. At present, United Natural flaunts a Zacks Rank of 1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The consensus estimate for United Natural’s current fiscal-year sales and earnings implies growth of 1.4% and 197.2%, respectively, from the year-ago figures. UNFI delivered a trailing four-quarter earnings surprise of 52.1%, on average.

Mama's Creations, Inc. MAMA manufactures and markets fresh deli-prepared foods in the United States. At present, MAMA sports a Zacks Rank of 1. Mama's Creations delivered a trailing four-quarter earnings surprise of 133.3%, on average.

The consensus estimate for Mama's Creations’ current fiscal-year sales and earnings implies growth of 39.9% and 44.4%, respectively, from the year-ago figures.

The Hershey Company HSY engages in the manufacture and sale of confectionery products and pantry items in the United States and internationally. It holds a Zacks Rank #2 at present. HSY delivered a trailing four-quarter earnings surprise of 15%, on average.

The Zacks Consensus Estimate for Hershey’s current fiscal-year sales implies growth of 3.4%, from the year-ago figures.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-07 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite