|

|

|

|

|||||

|

|

|

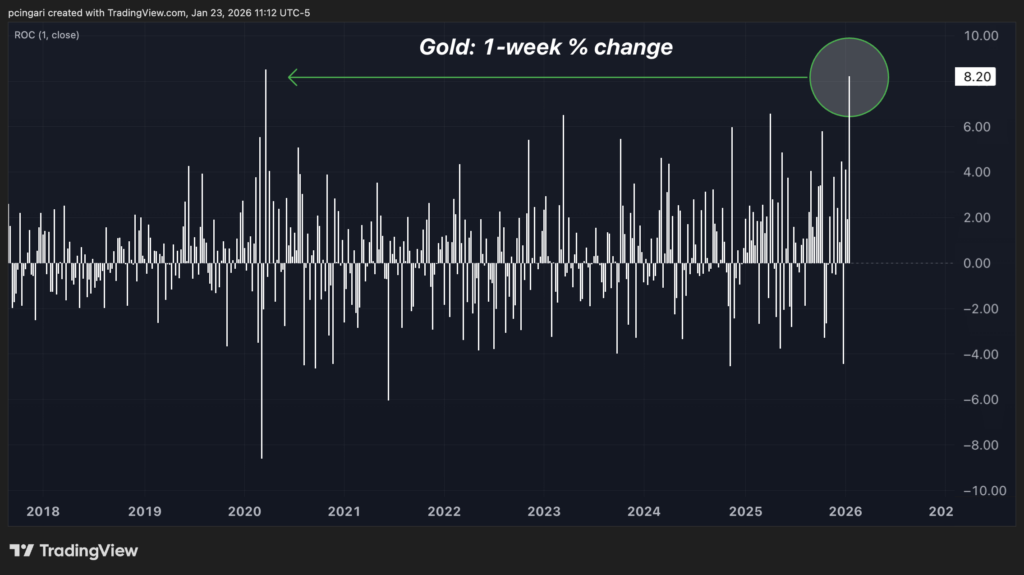

Gold rose for its fourth straight session to $4,988 per ounce on Friday, nearing the $5,000-per-ounce milestone and capping its strongest week in five years as a relentless precious-metals rally also propelled silver to a record $100 in the same session.

The yellow metal – tracked by the SPDR Gold Shares (NYSE:GLD) – is up over 8% on the week — its best performance since March 2020 and nearly 15% year to date, an advance few expected after gold surged 64% in 2025, its strongest annual gain since 1979.

Gold's climb to $5,000 is pushing investors to reassess whether the move reflects late-cycle excess after a historic run or the early phase of a structural shift in portfolio construction.

At the same time, major Wall Street banks increasingly treat $5,000 gold as a base case rather than a stretch scenario.

Jeremy Schwartz, global chief investment officer at WisdomTree, said gold should no longer be viewed as a niche hedge.

According to Schwartz, gold has become a "missing strategic allocation" in many portfolios rather than an alternative asset.

Central bank demand has reshaped the market. Since 2022, central bank gold purchases have quadrupled, averaging around 60 tonnes per month, far above the pre-2022 average of 17 tonnes.

Emerging market central banks continue diversifying reserves as geopolitical and monetary neutrality concerns persist.

Demand is no longer limited to official buyers. New, largely price-insensitive participants have entered the market. These include Chinese insurers, Indian pension funds and corporate buyers such as Tether.

Despite its surge, gold remains under-owned by many investors. “Most diversified portfolios still hold just 0–3% in gold versus a market-implied allocation closer to ~10–12%, creating asymmetric upside if even modest reallocations occur,” Schwartz said.

WisdomTree's base-case outlook aligns with several major banks projecting gold near $5,000 by the end of 2026, with upside scenarios approaching $6,000 if real yields fall and inflation pressures re-accelerate.

Earlier this week, Goldman Sachs raised its December 2026 gold forecast to $5,400 an ounce, up from $4,900, highlighting that “private sector diversification into gold has started to realize.”

Goldman noted that while central bank purchases drove gains in 2023 and 2024, the rally intensified in 2025 as private investors, ETFs and physical buyers began competing more aggressively for bullion.

The firm expects central bank buying to remain elevated through 2026, while lower interest rates and persistent macro policy risks continue to support investor demand.

"We assume private sector diversification buyers, whose purchases hedge global policy risks and have driven the upside surprise to our price forecast, don’t liquidate their gold holdings in 2026," Goldman’s Daan Struyven said.

"We see the risks to our upgraded gold price forecast as two-sided but still significantly skewed to the upside," he added.

The bank highlighted that gold supply is largely price-inelastic. Mine output adds only about 1% annually to global stocks, meaning rallies typically end only when demand fades rather than when supply responds.

Image created using artificial intelligence via Midjourney.

| Mar-18 | |

| Mar-18 | |

| Mar-18 | |

| Mar-16 | |

| Mar-16 | |

| Mar-13 | |

| Mar-12 | |

| Mar-11 | |

| Mar-11 | |

| Mar-10 | |

| Mar-10 | |

| Mar-10 | |

| Mar-09 | |

| Mar-09 | |

| Mar-07 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about Finviz Elite