|

|

|

|

|||||

|

|

|

Headquartered in Cambridge, MA, Zacks Rank #5 (Strong Sell) stock HubSpot Inc. (HUBS) is a prominent cloud-based Customer Relationship Management (CRM) platform thathelps primarily small-to-medium-sized businesses (SMBs) grow sales. HubSpot’s all-in-one HubSpot Growth platform combines the following three verticals into one platform: the Marketing Hub, the Service Hub, and the Sales Hub. Below is a breakdown of the capabilities of each:

· Marketing Hub: Helps users create marketing automation emails, Content Optimization Systems (COS), social media outreach and management, and provides CRM reporting and analytics.

· Sales Hub: Features include email engagement notifications, meetings, calling, new lead alerts, and website visit alerts, email templates, and CRM tracking and contact insights.

· Service Hub: Features include automation and routing, live chat and conversations, conversational bots, team emails, help desk and tickets, reporting tools and feedback.

Despite the software industry’s robust long-term performance, the group’s performance has deteriorated dramatically over the past few months. Below are some of the software group’s biggest losers (sorted by drawdown from all-time highs):

· UiPath (PATH): -84%

· Paycom Software (PAYC): -73%

· The Trade Desk (TTD): -70%

· DocuSign (DOCU): -65%

The horrific performance in many former leading software stocks is no accident. With the advent of advanced AI tools, investors are increasingly concerned that AI will disrupt these once-lucrative businesses. In fact, there are plenty of signs that this is already occurring. The latest AI tools, like Anthropic’s “Claude Coworker”, help companies perform tasks much faster than legacy software companies and at a fraction of the cost.

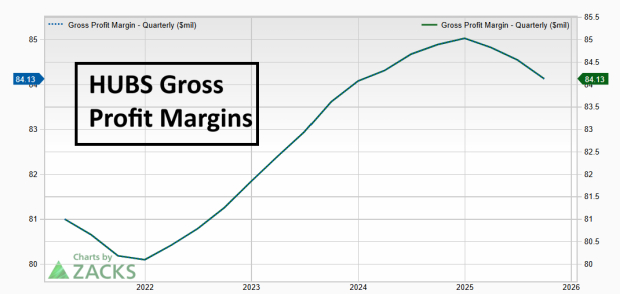

HubSpot has done its best to embrace innovation by investing in data center infrastructure and its AI efforts. However, the new, top-of-the-line AI programs threaten to end the legacy software subscription model that forces companies to pay per user and generates the juicy profits associated with legacy software leaders. HUBS’ gross profit margins peaked in early 2025.

HubSpot recently introduced a low-cost $20 per month starter pack, which includes limited features in an effort to attract new customers. Although the incentive is likely to attract new customers, the effort could cannibalize HubSpot’s premium products.

Although HUBS is still growing at a moderate clip (for now), its price action is telling. The stock is down more than 20% year-to-date, signaling formidable relative weakness. Meanwhile, HUBS shares are below the key moving averages and falling on heavy volume – a crystal-clear sign of heavy distribution.

Bottom Line

Despite its established position as a CRM leader for small-to-medium sized businesses, HubSpot currently faces a challenging crossroads. With the emergence of powerful, AI-driven alternatives, HubSpot’s margins are likely to be threatened.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 3 hours | |

| 8 hours | |

| 10 hours | |

| 11 hours | |

| 11 hours | |

| 12 hours | |

| 12 hours | |

| 12 hours | |

| 12 hours | |

| 14 hours | |

| 14 hours | |

| 14 hours | |

| 15 hours | |

| Aug-06 | |

| Aug-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite