|

|

|

|

|||||

|

|

|

Micron Technology, Inc.’s MU shares tripled in 2025, far outpacing Wall Street favorite NVIDIA Corporation NVDA. But for investors who haven’t yet jumped in, there is still a chance to invest in the company’s growth story, especially given its attractive valuation. Let’s see in detail –

Surging demand for Micron’s high-bandwidth memory (HBM) chips has lately powered its quarterly performance. Micron’s HBM chips are increasingly valued as they are capable of handling large volumes of workloads while improving power efficiency.

Micron’s first-quarter fiscal 2026 revenues soared 56% year over year to $13.64 billion, and surpassed Wall Street’s projection of $12.88 billion, according to investors.micron.com. In particular, its cloud memory business unit reported sales of $5.28 billion, up a whopping 99.5% from the same period a year ago. Strong revenues helped Micron post a non-GAAP net income of $5.48 billion, surpassing analysts’ estimates.

The demand for Micron’s HBM chips is poised to increase further and shows no signs of easing as supply remains constrained. The expansion of AI infrastructure by hyperscalers and data center operators has increased the demand for HBM chips. Micron’s CEO, Sanjay Mehrotra, added that HBM supply constraints are expected to persist amid strong demand, creating a supply-demand imbalance that could lead to higher prices, benefiting Micron in the near future.

The total addressable market for HBM is expected to expand at a CAGR of around 40% from $35 billion in 2025 to nearly $100 billion by 2028, according to Micron. Against this backdrop, the company expects its financial performance to strengthen, with second-quarter fiscal 2026 revenues projected in the range of $18.3 billion to $19.1 billion, and net income also expected to increase.

Incessant demand for Micron’s HBM chips amid AI infrastructure growth has positioned it for further gains. The supply constraint and rapidly expanding market will surely boost Micron’s profit margins.

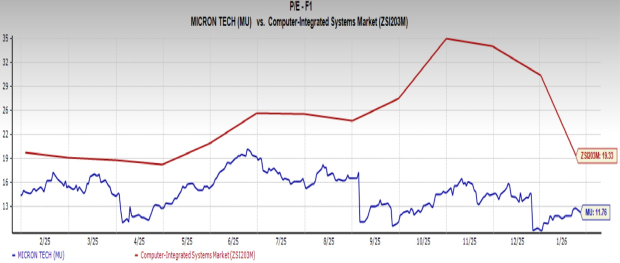

Interestingly, the market appears to be underestimating Micron’s growth potential. With a forward price-to-earnings (P/E) ratio of 11.76, well below the Computer-Integrated Systems industry’s average of 19.33, Micron presents an alluring buying opportunity without overpaying. The company’s high growth potential with healthy operating margins enhances its appeal to investors (read more: Micron vs. Palantir: Which AI Stock Is the Better Buy for 2026?).

Image Source: Zacks Investment Research

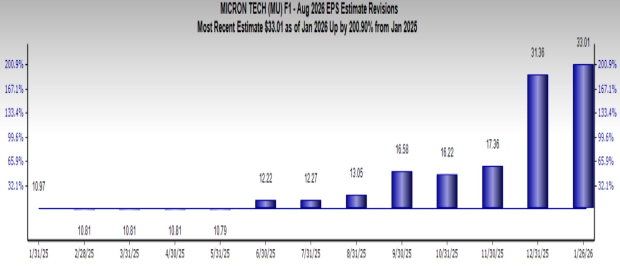

Micron currently sports a Zacks Rank #1 (Strong Buy), and its $33.01 Zacks Consensus Estimate for earnings per share implies growth of 200.9% year over year. You can see the complete list of today’s Zacks #1 Rank stocks here.

Image Source: Zacks Investment Research

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 55 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 5 hours | |

| Aug-09 | |

| Aug-09 | |

| Aug-09 | |

| Aug-09 | |

| Aug-09 | |

| Aug-09 | |

| Aug-09 | |

| Aug-09 | |

| Aug-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite