|

|

|

|

|||||

|

|

|

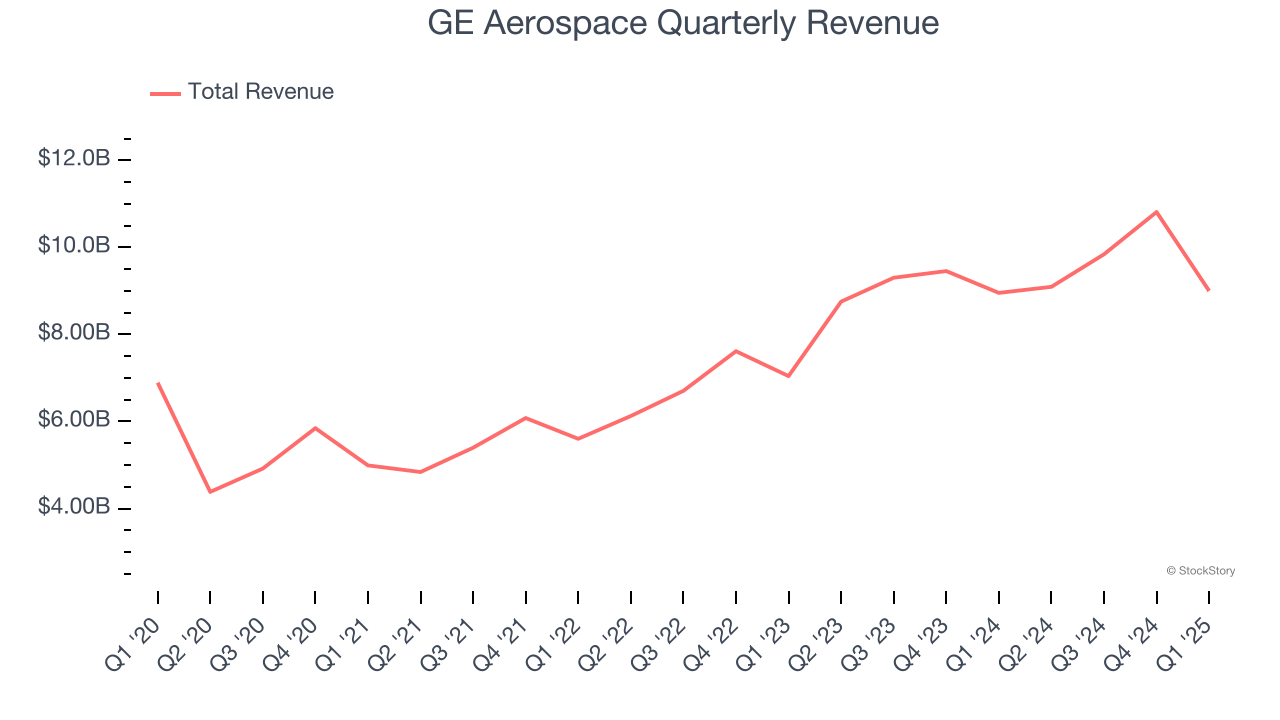

Industrial conglomerate GE Aerospace (NYSE:GE) missed Wall Street’s revenue expectations in Q1 CY2025, with sales flat year on year at $9.00 billion. Its non-GAAP profit of $1.49 per share was 17.3% above analysts’ consensus estimates.

Is now the time to buy GE Aerospace? Find out by accessing our full research report, it’s free.

One of the original 12 companies on the Dow Jones Industrial Average, General Electric (NYSE:GE) is a multinational conglomerate providing technologies for various sectors including aviation, power, renewable energy, and healthcare.

Automation that increases efficiency and connected equipment that collects analyzable data have been trending, creating new demand for general industrial machinery companies. Those who innovate and create digitized solutions can spur sales and speed up replacement cycles, but all general industrial machinery companies are still at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

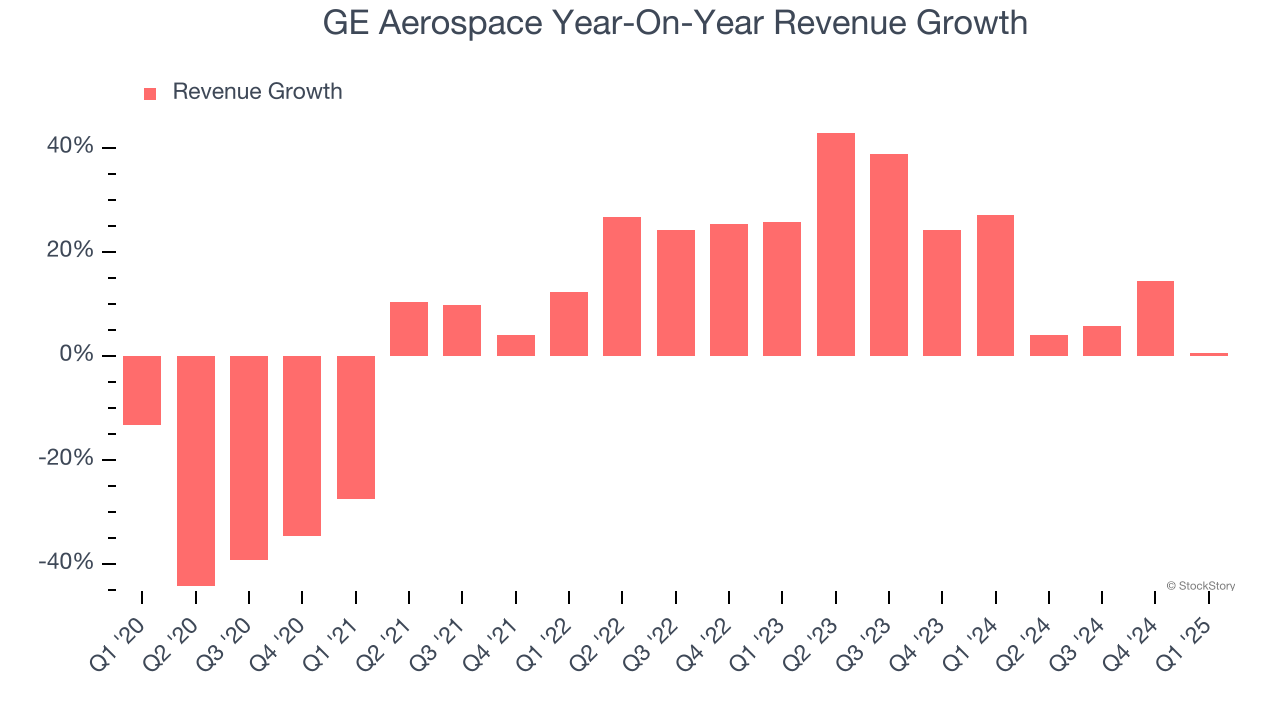

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years. Regrettably, GE Aerospace’s sales grew at a sluggish 4% compounded annual growth rate over the last five years. This wasn’t a great result compared to the rest of the industrials sector, but there are still things to like about GE Aerospace.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. GE Aerospace’s annualized revenue growth of 18.7% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

This quarter, GE Aerospace’s $9.00 billion of revenue was flat year on year, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 11.8% over the next 12 months, a deceleration versus the last two years. We still think its growth trajectory is attractive given its scale and implies the market is baking in success for its products and services.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

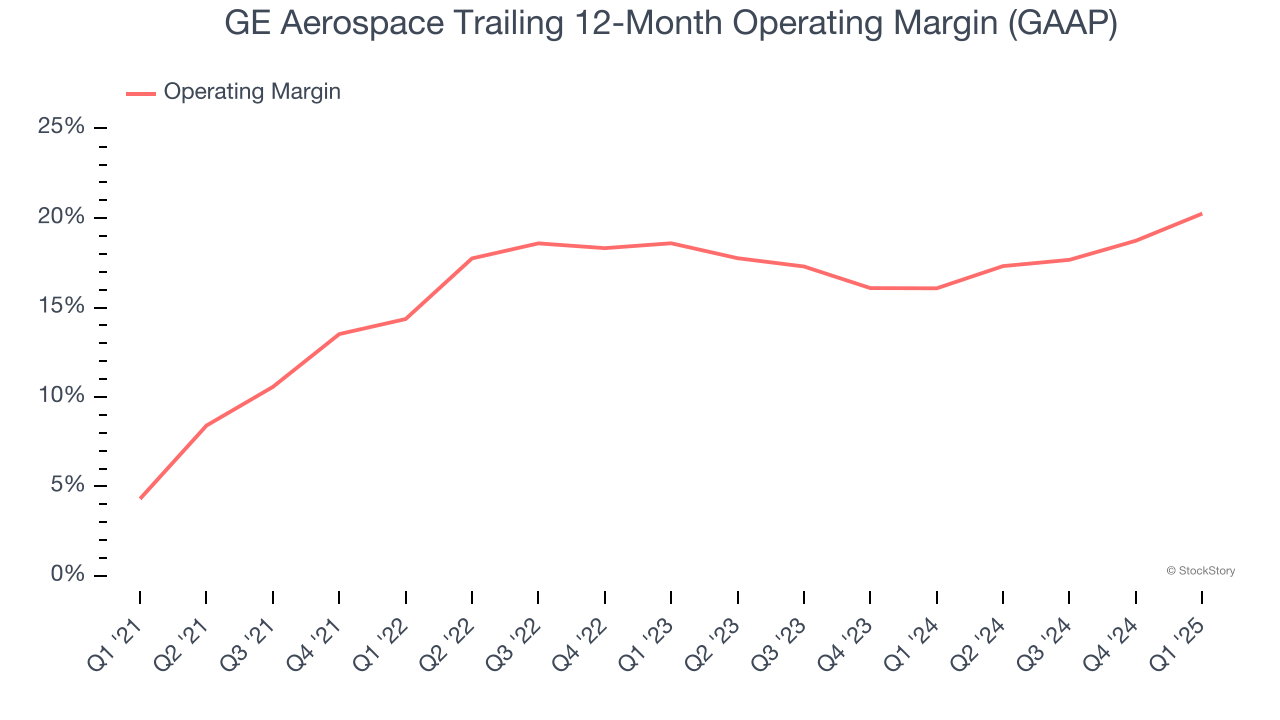

GE Aerospace has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 15.8%. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Analyzing the trend in its profitability, GE Aerospace’s operating margin rose by 15.9 percentage points over the last five years, as its sales growth gave it operating leverage.

This quarter, GE Aerospace generated an operating profit margin of 23.8%, up 6.5 percentage points year on year. The increase was solid and shows its expenses recently grew slower than its revenue, leading to higher efficiency.

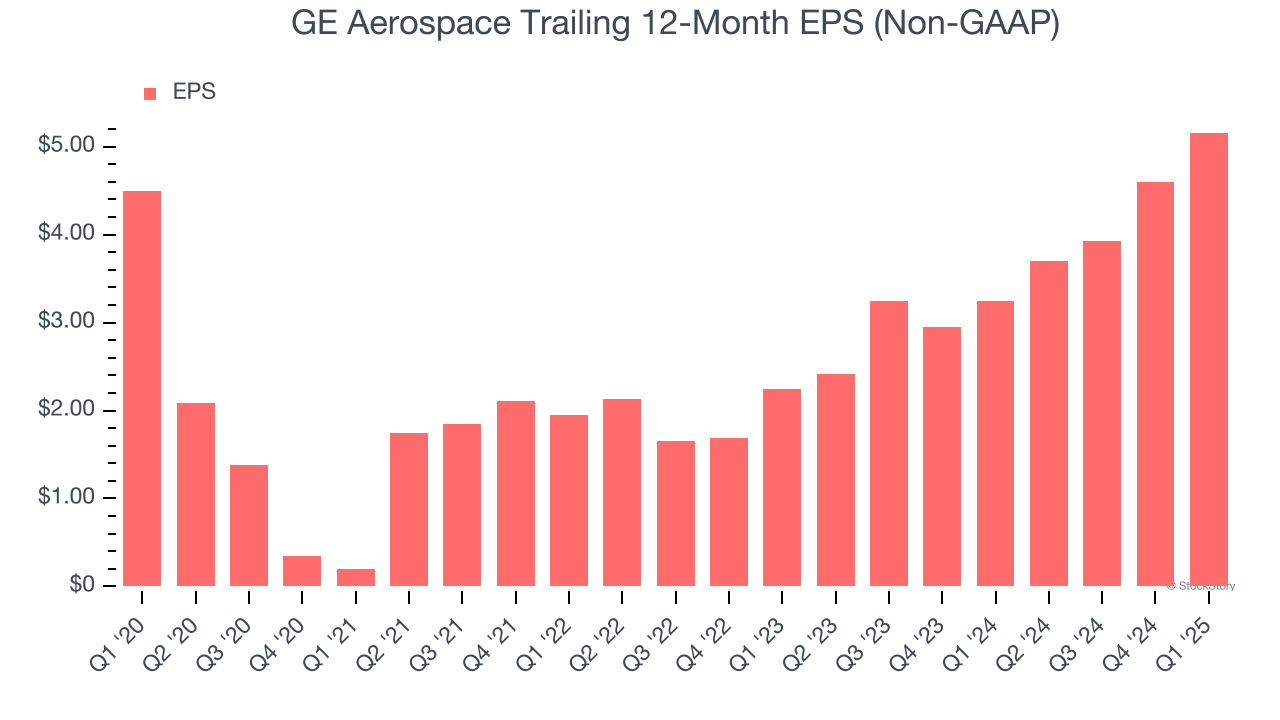

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

GE Aerospace’s EPS grew at a weak 2.8% compounded annual growth rate over the last five years, lower than its 4% annualized revenue growth. We can see the difference stemmed from higher taxes as the company actually grew its operating margin and repurchased its shares during this time.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

GE Aerospace’s two-year annual EPS growth of 51.5% was fantastic and topped its 18.7% two-year revenue growth.

In Q1, GE Aerospace reported EPS at $1.49, up from $0.93 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects GE Aerospace’s full-year EPS of $5.16 to grow 8.8%.

We enjoyed seeing GE Aerospace beat analysts’ EPS expectations this quarter. The company also reaffirmed its full-year EPS guidance. On the other hand, its revenue missed. Management stated that the "macroeconomic dynamics we are operating in today require us to take a number of strategic actions, such as controlling costs, and leveraging available trade programs." Overall, this was a mixed quarter. The stock remained flat at $180 immediately following the results.

So do we think GE Aerospace is an attractive buy at the current price? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-25 | |

| Feb-24 |

Dow Jones AI Giant Nvidia Eyes Buy Point With Earnings Set To Surge 72%

GE

Investor's Business Daily

|

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-22 | |

| Feb-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite