|

|

|

|

|||||

|

|

|

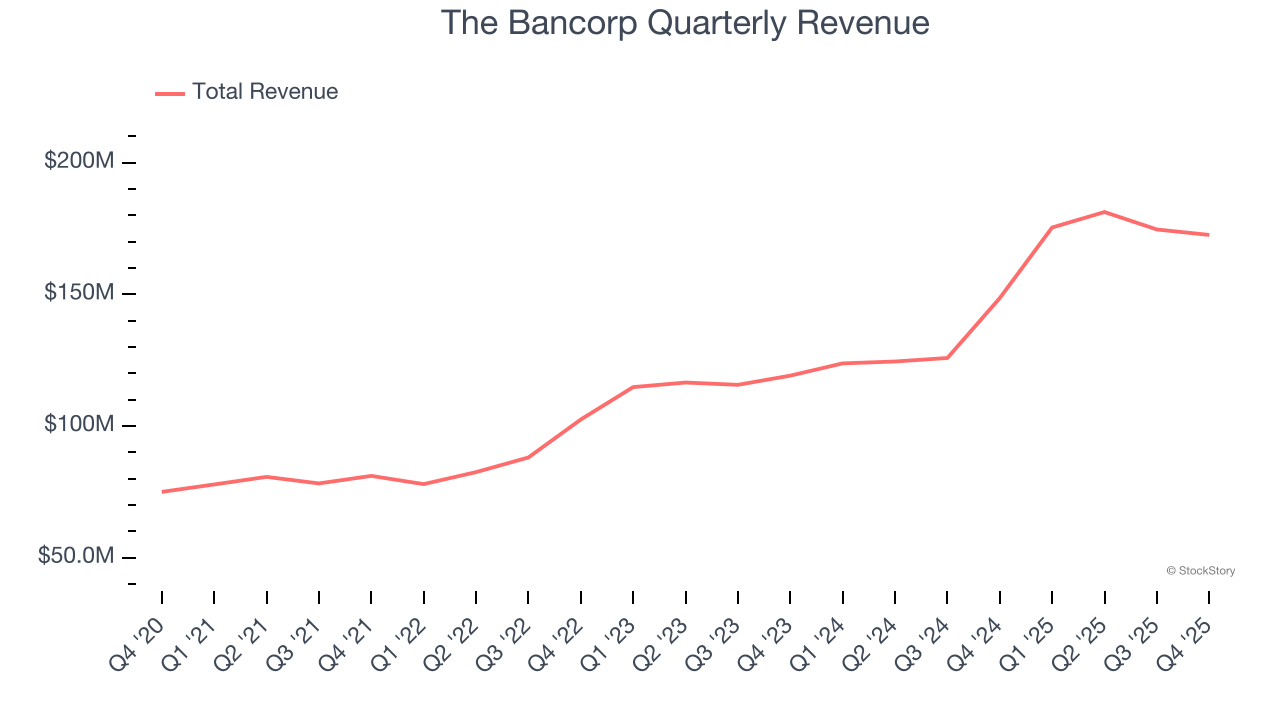

Financial services company The Bancorp (NASDAQ:TBBK) fell short of the markets revenue expectations in Q4 CY2025, but sales rose 16.1% year on year to $172.6 million. Its GAAP profit of $1.28 per share was 9.9% below analysts’ consensus estimates.

Is now the time to buy The Bancorp? Find out by accessing our full research report, it’s free.

“We are pleased with the significant progress made this year in strengthening our platform and deepening and expanding new and existing relationships. While we ended the year with record fourth quarter EPS and ROE, we did fall short of our expectations and guidance due to a culmination of factors, including the prolonged government shutdown’s impact on transaction volume and deposit flows, the strong ramp-up in sponsored credit materializing later than expected, some unanticipated NIM compression, and an unexpected legal settlement cost,” said Damian Kozlowski, CEO and President of The Bancorp.

Operating behind the scenes of many popular fintech apps and prepaid cards you might use daily, The Bancorp (NASDAQ:TBBK) is a bank holding company that specializes in providing banking services to fintech companies and offering specialty lending products.

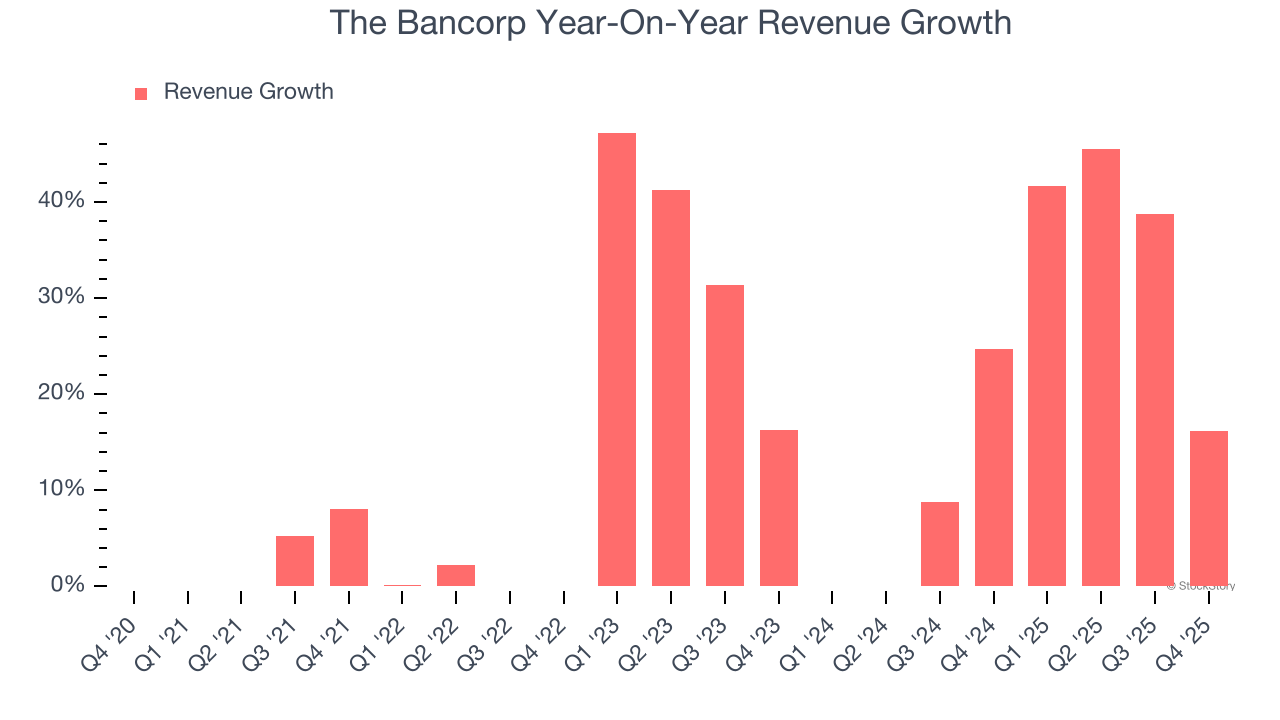

From lending activities to service fees, most banks build their revenue model around two income sources. Interest rate spreads between loans and deposits create the first stream, with the second coming from charges on everything from basic bank accounts to complex investment banking transactions. Luckily, The Bancorp’s revenue grew at an incredible 20.3% compounded annual growth rate over the last five years. Its growth surpassed the average banking company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. The Bancorp’s annualized revenue growth of 22.9% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

This quarter, The Bancorp’s revenue grew by 16.1% year on year to $172.6 million but fell short of Wall Street’s estimates.

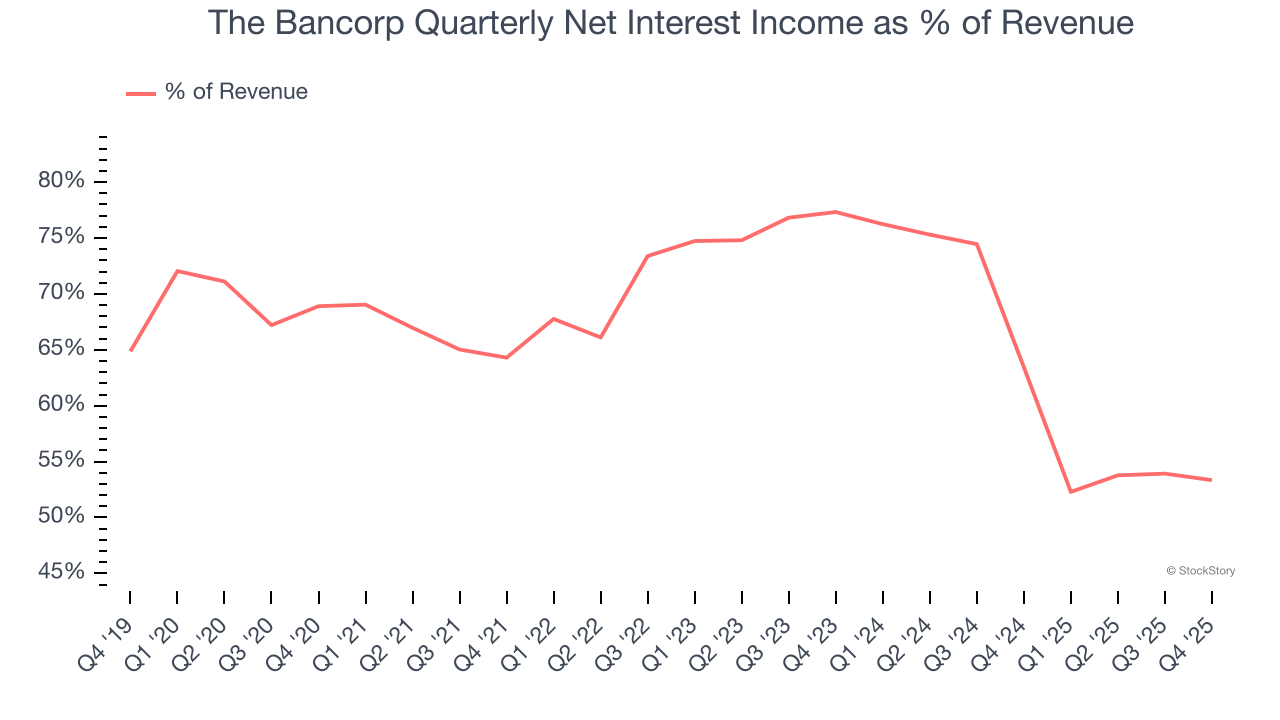

Net interest income made up 67.3% of the company’s total revenue during the last five years, meaning lending operations are The Bancorp’s largest source of revenue.

Our experience and research show the market cares primarily about a bank’s net interest income growth as non-interest income is considered a lower-quality and non-recurring revenue source.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

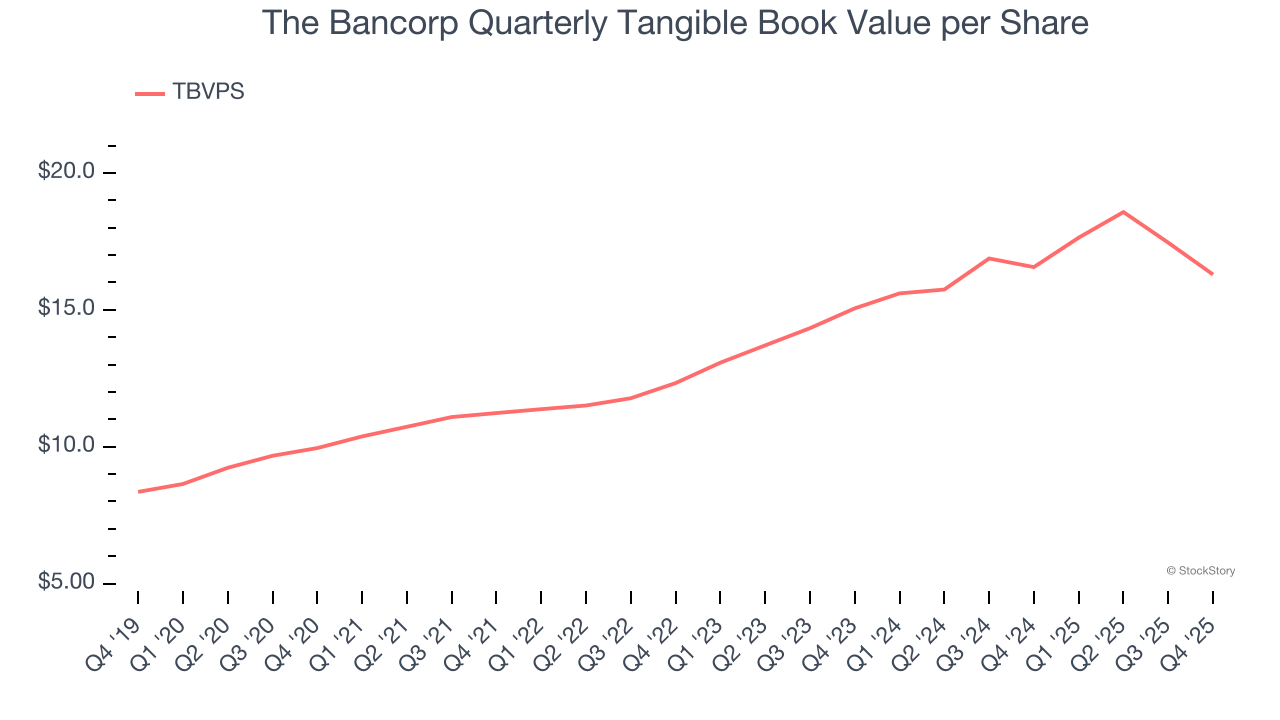

Banks are balance sheet-driven businesses because they generate earnings primarily through borrowing and lending. They’re also valued based on their balance sheet strength and ability to compound book value (another name for shareholders’ equity) over time.

This is why we consider tangible book value per share (TBVPS) the most important metric to track for banks. TBVPS represents the real, liquid net worth per share of a bank, excluding intangible assets that have debatable value upon liquidation. EPS can become murky due to acquisition impacts or accounting flexibility around loan provisions, and TBVPS resists financial engineering manipulation.

The Bancorp’s TBVPS grew at an incredible 10.4% annual clip over the last five years. However, TBVPS growth has recently decelerated to 4% annual growth over the last two years (from $15.05 to $16.29 per share).

Over the next 12 months, Consensus estimates call for The Bancorp’s TBVPS to grow by 16.3% to $18.95, solid growth rate.

We struggled to find many positives in these results. Its revenue missed and its net interest income fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 2.7% to $68.53 immediately following the results.

The Bancorp underperformed this quarter, but does that create an opportunity to invest right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).

| Aug-03 | |

| Jul-31 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-17 | |

| Apr-25 | |

| Apr-24 | |

| Apr-23 | |

| Apr-23 | |

| Apr-10 | |

| Mar-09 | |

| Mar-06 | |

| Mar-04 | |

| Feb-15 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite