|

|

|

|

|||||

|

|

|

City Holding currently trades at $125.22 per share and has shown little upside over the past six months, posting a middling return of 3.5%. The stock also fell short of the S&P 500’s 9.6% gain during that period.

Is there a buying opportunity in City Holding, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

We're sitting this one out for now. Here are three reasons we avoid CHCO and a stock we'd rather own.

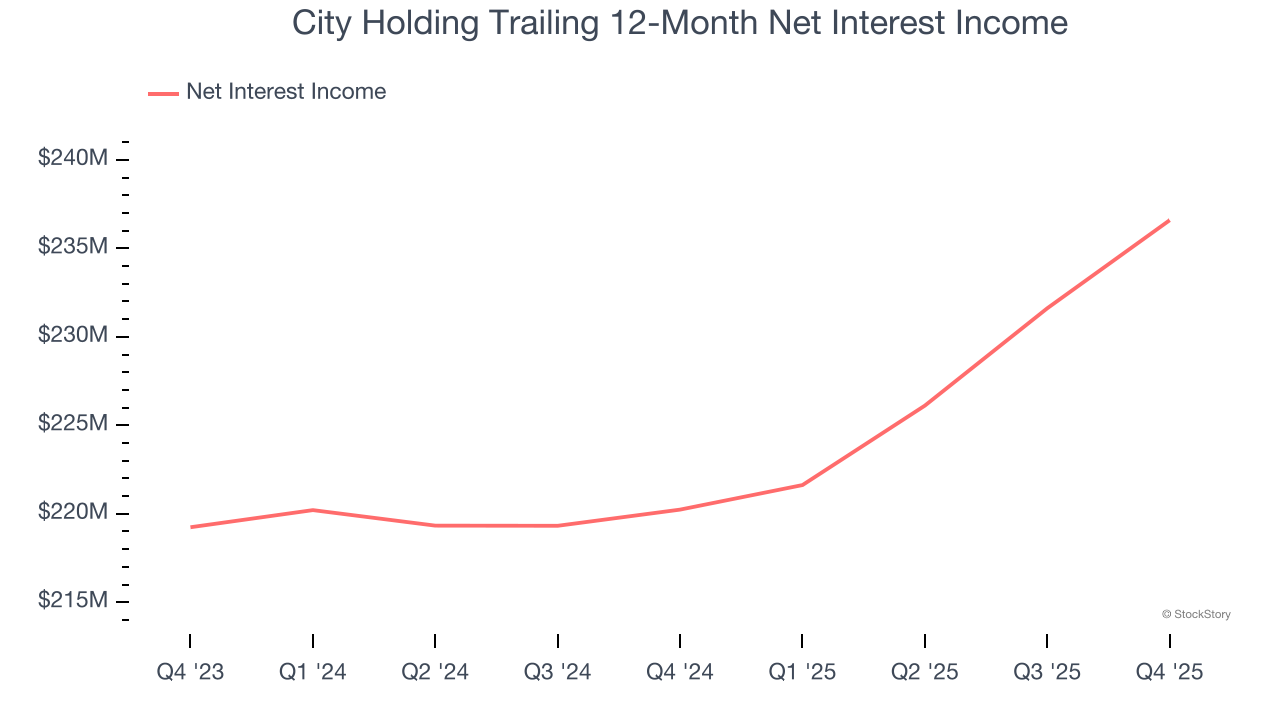

Markets consistently prioritize net interest income over non-recurring fees, recognizing its superior quality compared to the more unpredictable revenue streams.

City Holding’s net interest income has grown at a 8.9% annualized rate over the last five years, slightly worse than the broader banking industry.

Forecasted net interest income by Wall Street analysts signals a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect City Holding’s net interest income to rise by 3.7%, close to its 3.9% annualized growth for the past two years.

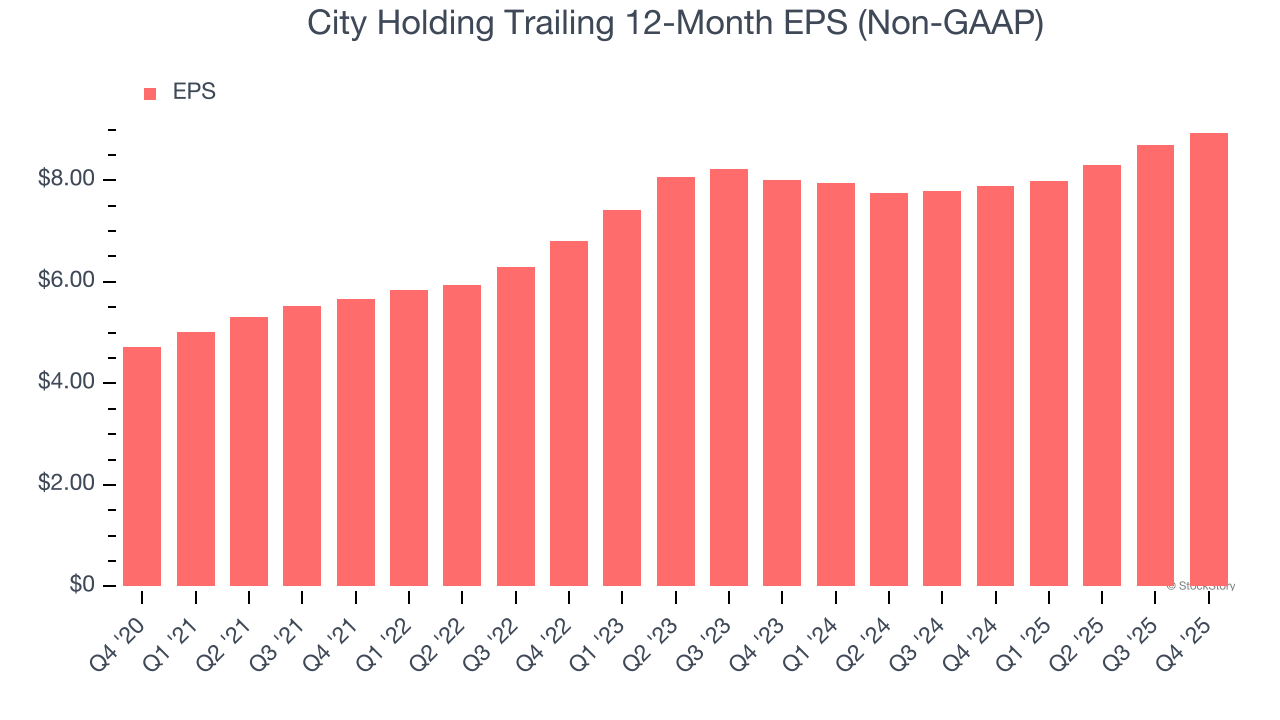

While long-term earnings trends give us the big picture, we also track EPS over a shorter period because it can provide insight into an emerging theme or development for the business.

City Holding’s EPS grew at a weak 5.6% compounded annual growth rate over the last two years. On the bright side, this performance was higher than its 3.3% annualized revenue growth and tells us the company became more profitable on a per-share basis as it expanded.

City Holding’s business quality ultimately falls short of our standards. With its shares lagging the market recently, the stock trades at 2× forward P/B (or $125.22 per share). Beauty is in the eye of the beholder, but we don’t really see a big opportunity at the moment. We're fairly confident there are better stocks to buy right now. Let us point you toward a safe-and-steady industrials business benefiting from an upgrade cycle.

The market’s up big this year - but there’s a catch. Just 4 stocks account for half the S&P 500’s entire gain. That kind of concentration makes investors nervous, and for good reason. While everyone piles into the same crowded names, smart investors are hunting quality where no one’s looking - and paying a fraction of the price. Check out the high-quality names we’ve flagged in our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

| Jul-22 | |

| Jul-22 | |

| Apr-29 | |

| Apr-23 | |

| Apr-23 | |

| Mar-25 | |

| Feb-17 | |

| Feb-02 | |

| Jan-23 | |

| Jan-21 | |

| Jan-21 | |

| Jan-21 | |

| Jan-21 | |

| Jan-21 | |

| Dec-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite