|

|

|

|

|||||

|

|

|

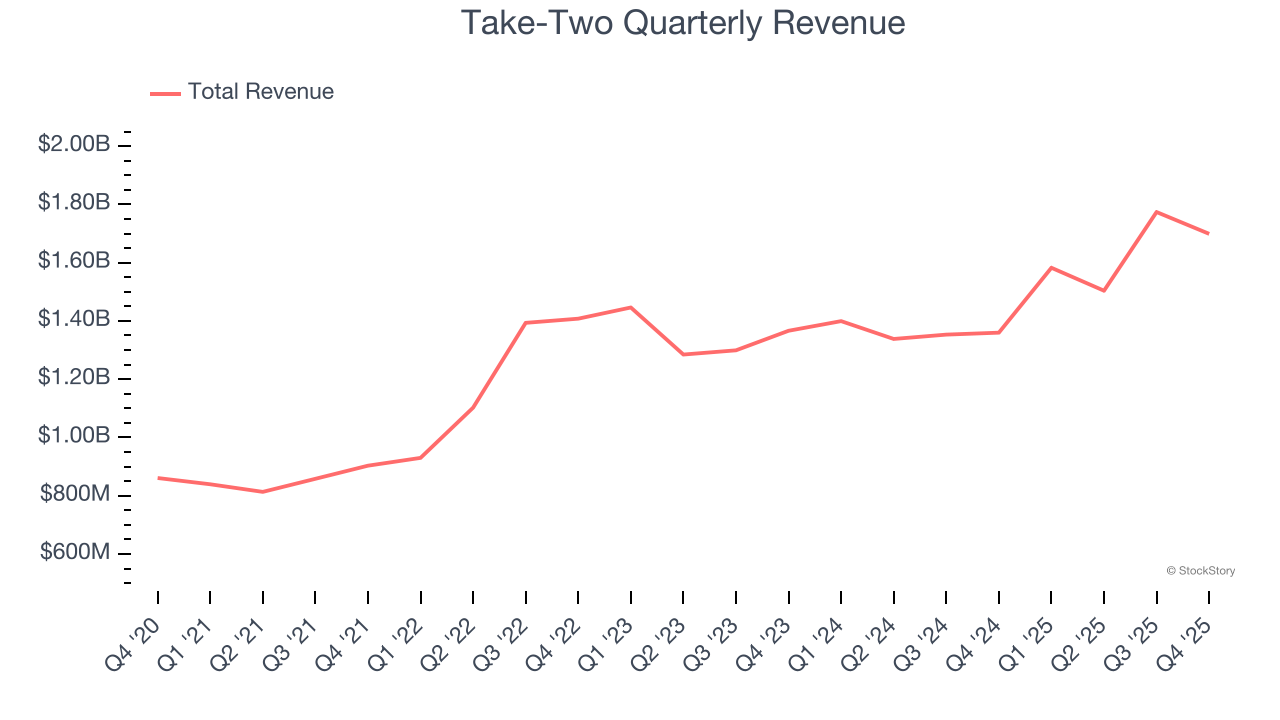

Video game publisher Take Two (NASDAQ:TTWO) reported Q4 CY2025 results topping the market’s revenue expectations, with sales up 24.9% year on year to $1.70 billion. On top of that, next quarter’s revenue guidance ($1.60 billion at the midpoint) was surprisingly good and 5.2% above what analysts were expecting. Its GAAP loss of $0.50 per share was 28.6% below analysts’ consensus estimates.

Is now the time to buy Take-Two? Find out by accessing our full research report, it’s free.

Strauss Zelnick, Chairman and CEO of Take-Two Interactive, stated: “Our outstanding third quarter results reflect outperformance from all of our labels, and we are once again raising our Net Bookings outlook for Fiscal 2026. With ongoing momentum across many of our businesses, and the highly anticipated launch of Grand Theft Auto VI on November 19th, we continue to project record levels of Net Bookings in Fiscal 2027, which we believe will establish a new financial baseline for our business, set us on a path to enhanced profitability, and provide further balance sheet strength and flexibility.”

Best known for its Grand Theft Auto and NBA 2K franchises, Take Two (NASDAQ:TTWO) is one of the world’s largest video game publishers.

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Thankfully, Take-Two’s 10.7% annualized revenue growth over the last three years was decent. Its growth was slightly above the average consumer internet company and shows its offerings resonate with customers.

This quarter, Take-Two reported robust year-on-year revenue growth of 24.9%, and its $1.70 billion of revenue topped Wall Street estimates by 7.5%. Company management is currently guiding for flat sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 27.9% over the next 12 months, an acceleration versus the last three years. This projection is eye-popping and suggests its newer products and services will spur better top-line performance.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

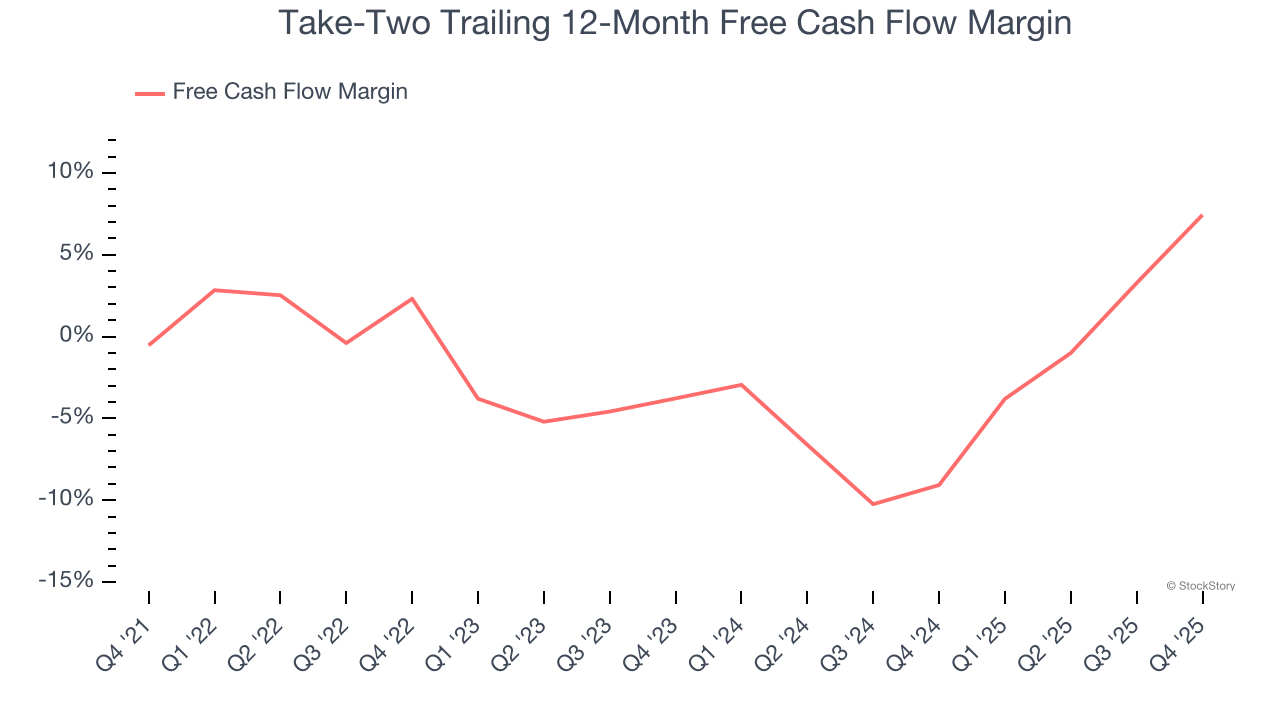

Take-Two broke even from a free cash flow perspective over the last two years, giving the company limited opportunities to return capital to shareholders. The divergence from its good EBITDA margin stems from its capital-intensive business model, which requires Take-Two to make large cash investments in working capital (i.e., stocking inventories) and capital expenditures (i.e., building new facilities).

Taking a step back, an encouraging sign is that Take-Two’s margin expanded by 5.1 percentage points over the last few years. The company’s improvement shows it’s heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability fell.

Take-Two’s free cash flow clocked in at $236.2 million in Q4, equivalent to a 13.9% margin. Its cash flow turned positive after being negative in the same quarter last year, building on its favorable historical trend.

It was great to see Take-Two’s revenue guidance for next quarter top analysts’ expectations. We were also glad its revenue outperformed Wall Street’s estimates. On the other hand, its full-year EBITDA guidance missed and its EBITDA fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded up 3.9% to $220.45 immediately following the results.

Big picture, is Take-Two a buy here and now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).

| Jun-02 | |

| Jun-02 | |

| May-22 | |

| May-22 | |

| May-22 | |

| May-22 | |

| May-22 | |

| May-22 | |

| May-22 | |

| May-22 | |

| May-22 | |

| May-22 | |

| May-22 | |

| May-22 | |

| May-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite