|

|

|

|

|||||

|

|

|

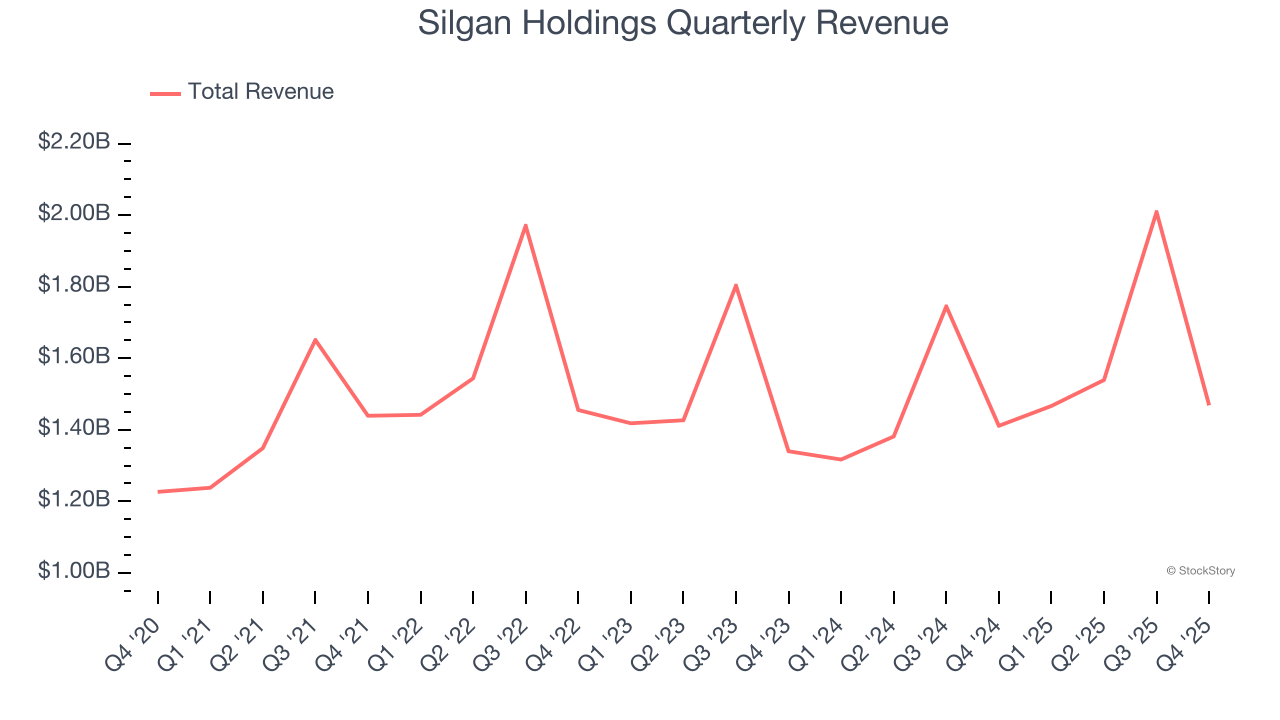

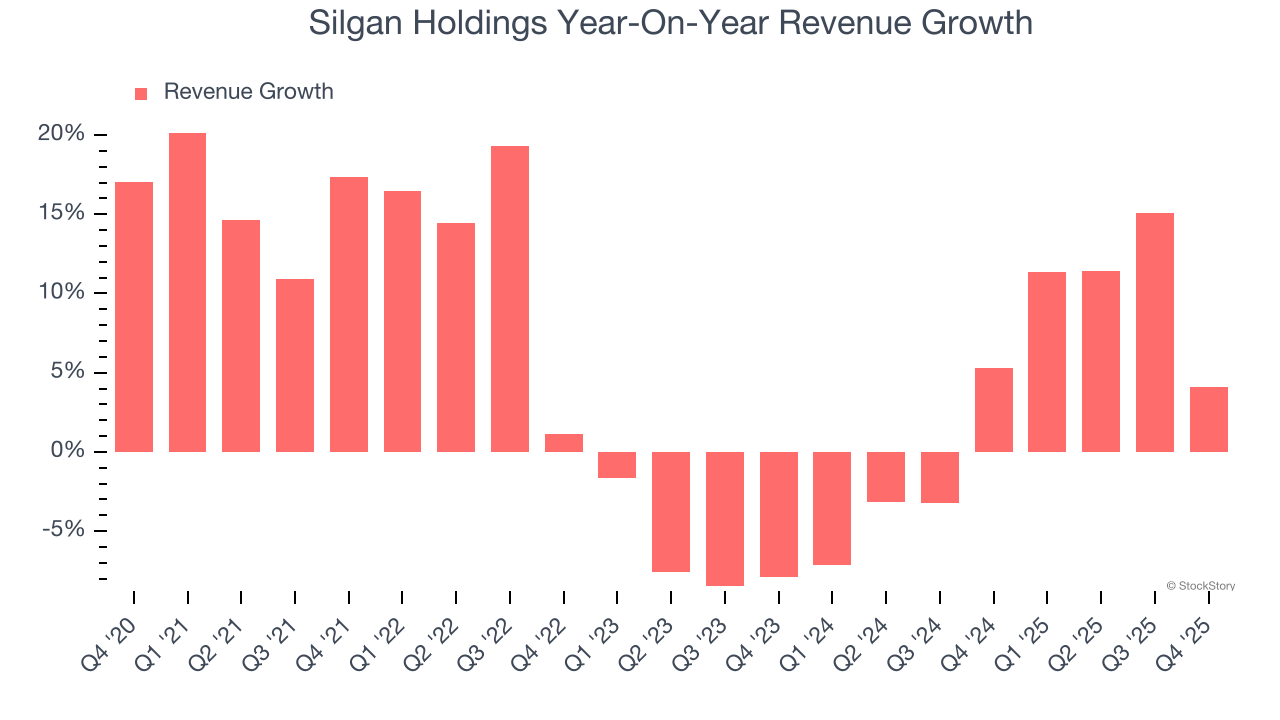

Rigid packaging solutions manufacturer Silgan Holdings (NYSE:SLGN) announced better-than-expected revenue in Q4 CY2025, with sales up 4.1% year on year to $1.47 billion. Its non-GAAP profit of $0.67 per share was 4.3% above analysts’ consensus estimates.

Is now the time to buy Silgan Holdings? Find out by accessing our full research report, it’s free.

"Our 2025 results continued to highlight the meaningful progress from our key strategic initiatives, as we successfully integrated the Weener acquisition, continued to outpace market growth in our high value dispensing and pet food products, and completed our multi-year cost savings program. The Silgan team showed exceptional strength, drive and commitment in 2025 while adapting to a dynamic operating environment and continuing to compete and win in the marketplace by meeting the unique needs of our customers and being the best at what we do. The power of our diverse portfolio of consumer staple products, the effectiveness of the Silgan business model, and the discipline of our capital deployment strategy has positioned the Company to continue to outperform our peers and our end markets to create meaningful value for our shareholders," said Adam Greenlee, President and CEO.

Established in 1987, Silgan Holdings (NYSE:SLGN) is a supplier of rigid packaging for consumer goods products, specializing in metal containers, closures, and plastic packaging.

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Silgan Holdings grew its sales at a tepid 5.7% compounded annual growth rate. This fell short of our benchmark for the industrials sector and is a tough starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Silgan Holdings’s recent performance shows its demand has slowed as its annualized revenue growth of 4.1% over the last two years was below its five-year trend.

This quarter, Silgan Holdings reported modest year-on-year revenue growth of 4.1% but beat Wall Street’s estimates by 0.6%.

Looking ahead, sell-side analysts expect revenue to grow 1.9% over the next 12 months, a slight deceleration versus the last two years. This projection doesn't excite us and implies its products and services will face some demand challenges.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

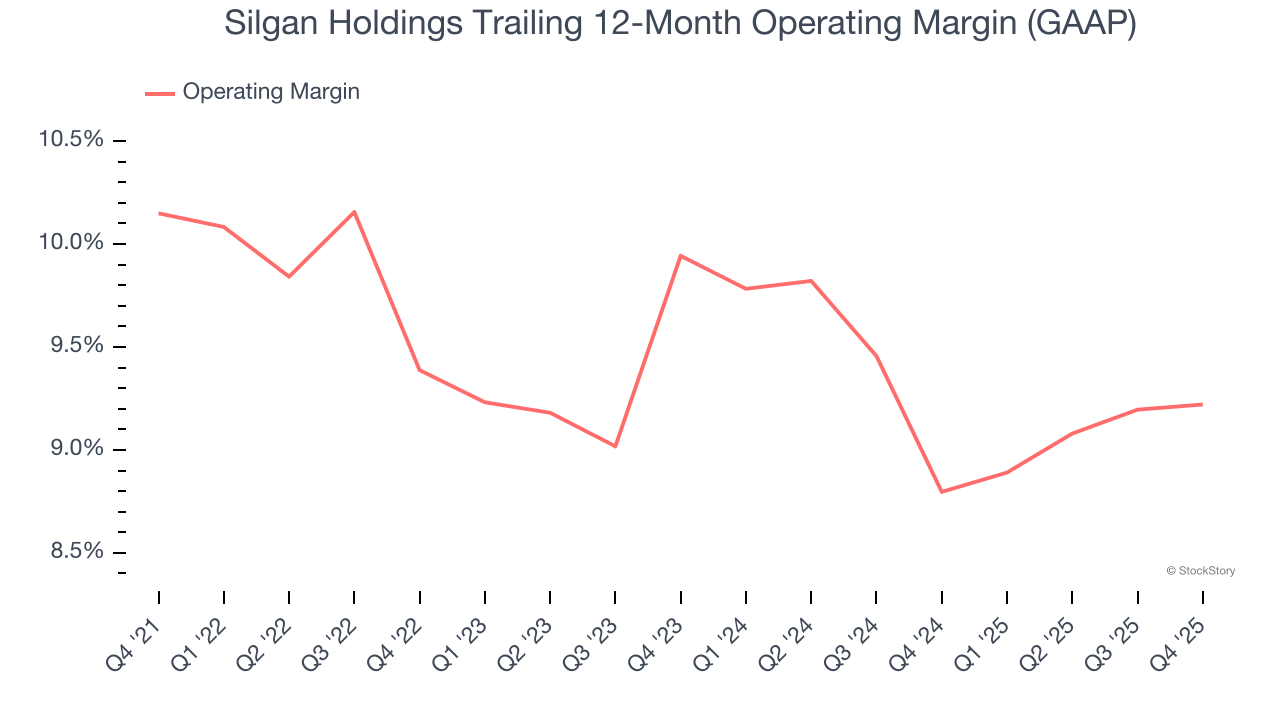

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Silgan Holdings’s operating margin might fluctuated slightly over the last 12 months but has generally stayed the same, averaging 9.5% over the last five years. This profitability was higher than the broader industrials sector, showing it did a decent job managing its expenses.

Looking at the trend in its profitability, Silgan Holdings’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. We like to see margin expansion, but we’re still happy with Silgan Holdings’s performance considering most Industrial Packaging companies saw their margins plummet.

In Q4, Silgan Holdings generated an operating margin profit margin of 6.9%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

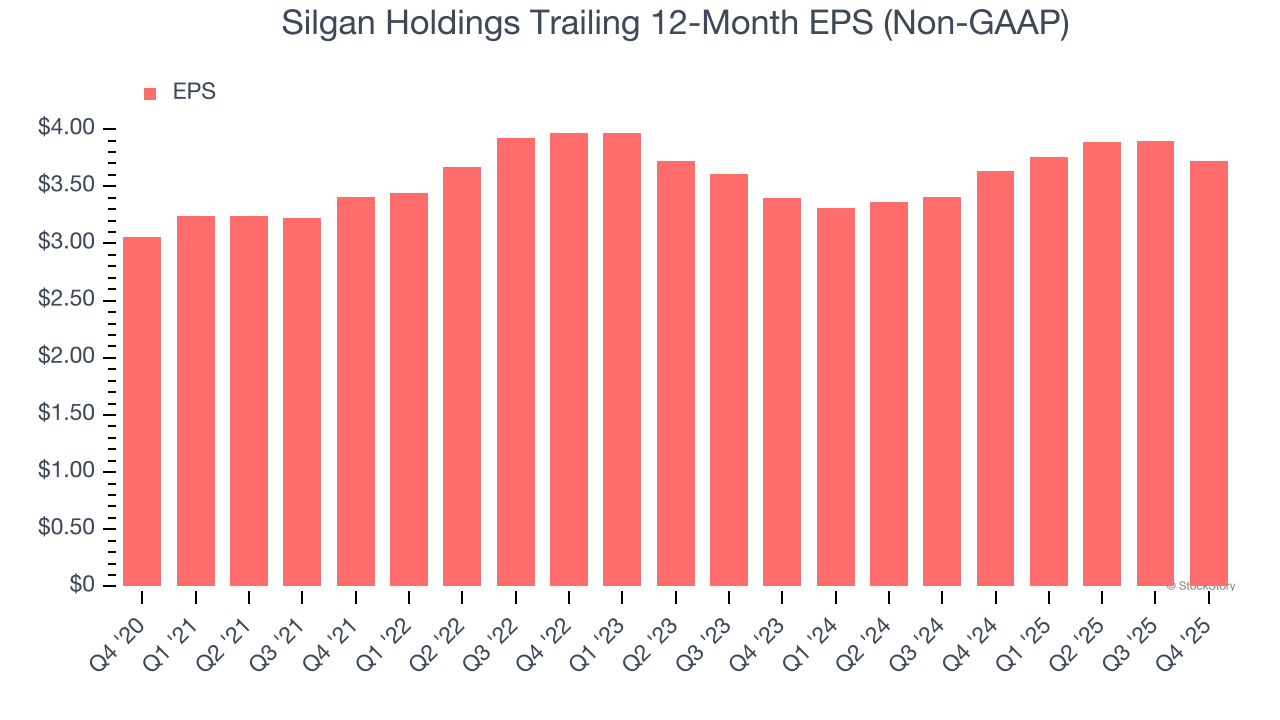

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Silgan Holdings’s weak 4% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Silgan Holdings, its two-year annual EPS growth of 4.6% is similar to its five-year trend, implying stable earnings.

In Q4, Silgan Holdings reported adjusted EPS of $0.67, down from $0.85 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 4.3%. Over the next 12 months, Wall Street expects Silgan Holdings’s full-year EPS of $3.72 to grow 2.1%.

It was good to see Silgan Holdings beat analysts’ EPS expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. On the other hand, its EBITDA missed and its EPS guidance for next quarter fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock remained flat at $43.76 immediately after reporting.

So do we think Silgan Holdings is an attractive buy at the current price? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).

| Jul-10 | |

| May-12 | |

| Apr-29 | |

| Apr-29 | |

| Apr-29 | |

| Apr-10 | |

| Mar-23 | |

| Mar-06 | |

| Feb-24 | |

| Feb-18 | |

| Feb-11 | |

| Feb-05 | |

| Feb-05 | |

| Feb-04 | |

| Feb-04 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite