|

|

|

|

|||||

|

|

|

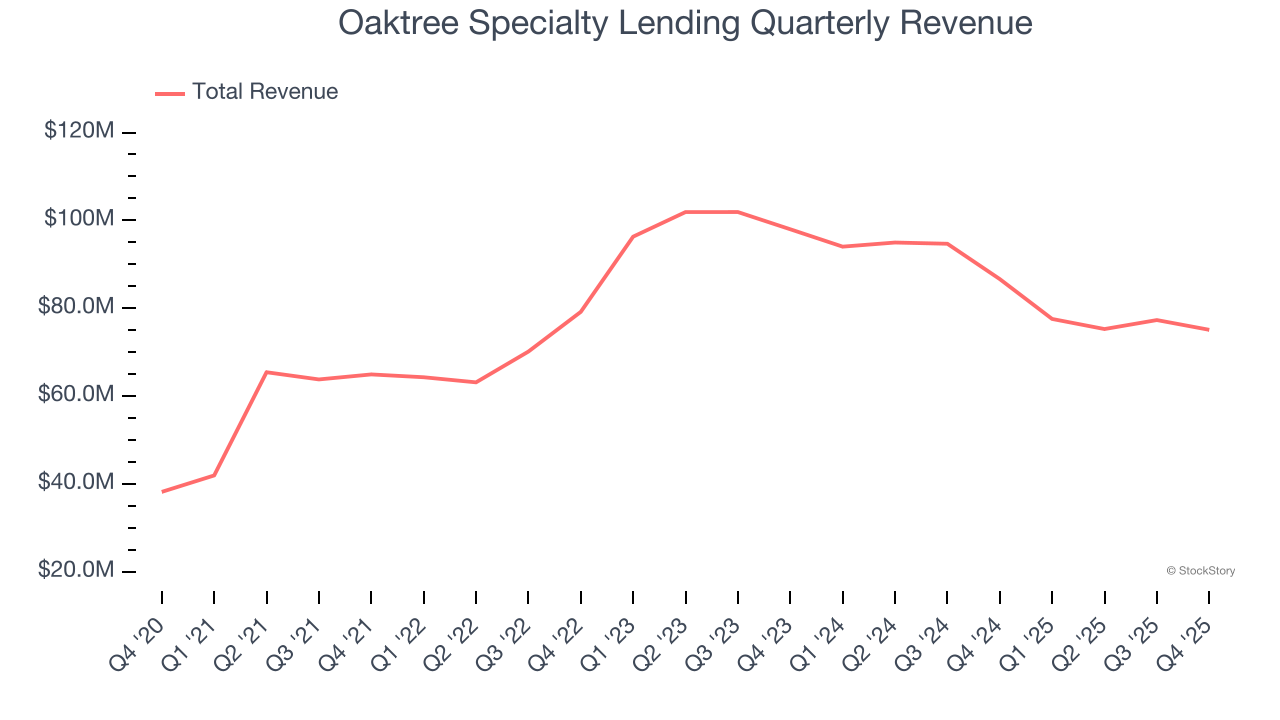

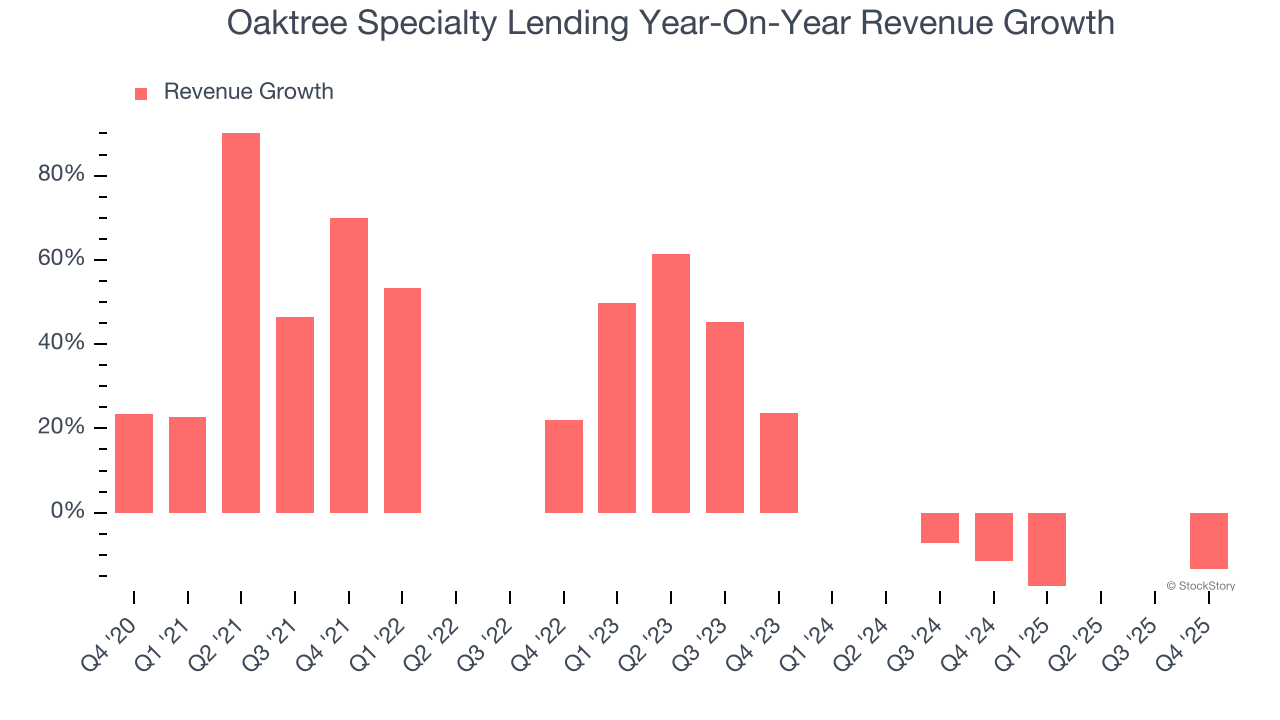

Business development company Oaktree Specialty Lending (NASDAQ:OCSL) met Wall Streets revenue expectations in Q4 CY2025, but sales fell by 13.3% year on year to $75.1 million. Its non-GAAP profit of $0.06 per share was 84.1% below analysts’ consensus estimates.

Is now the time to buy Oaktree Specialty Lending? Find out by accessing our full research report, it’s free.

“We delivered solid results in the first fiscal quarter of 2026 including adjusted net investment income of $36.7 million, or $0.41 per share, and fully covered our dividend,” said Armen Panossian, Chief Executive Officer and Chief Investment Officer of Oaktree Specialty Lending.

Managed by Oaktree Capital Management, one of the world's premier alternative investment firms, Oaktree Specialty Lending (NASDAQ:OCSL) is a business development company that provides customized financing solutions to mid-market companies across various industries.

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Oaktree Specialty Lending grew its revenue at an impressive 15.2% compounded annual growth rate. Its growth beat the average financials company and shows its offerings resonate with customers.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Oaktree Specialty Lending’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 12.4% over the last two years.

This quarter, Oaktree Specialty Lending reported a rather uninspiring 13.3% year-on-year revenue decline to $75.1 million of revenue, in line with Wall Street’s estimates.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

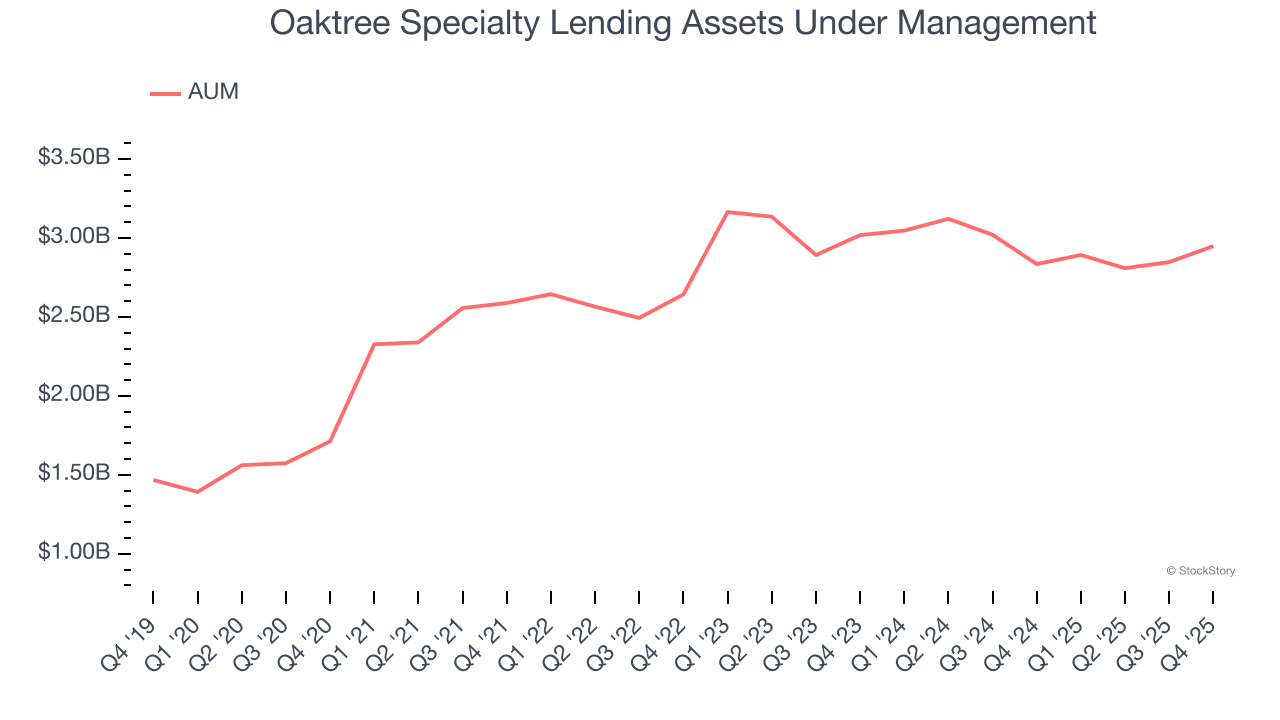

Assets Under Management (AUM) encompasses all client funds under a firm's investment management umbrella. The recurring fee structure on these assets provides consistent revenue generation, offering financial stability even during periods of poor investment returns, though sustained underperformance can impact future asset flows.

Oaktree Specialty Lending’s AUM has grown at an annual rate of 13% over the last five years, a step above the broader financials industry but slower than its total revenue. When analyzing Oaktree Specialty Lending’s AUM over the last two years, we can see its assets dropped by 3% annually. Other parts of the business were even bigger detractors of growth than fundraising or short-term investment performance over this shorter period since assets outperformed total revenue. But again, we put less weight on asset growth given how lumpy and cyclical it can be.

In Q4, Oaktree Specialty Lending’s AUM was $2.95 billion, beating analysts’ expectations by 1.7%. This print was 4% higher than the same quarter last year.

It was encouraging to see Oaktree Specialty Lending beat analysts’ AUM expectations this quarter. On the other hand, its EPS missed. Overall, this quarter could have been better. The stock remained flat at $12.12 immediately after reporting.

The latest quarter from Oaktree Specialty Lending’s wasn’t that good. One earnings report doesn’t define a company’s quality, though, so let’s explore whether the stock is a buy at the current price. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).

| 10 hours | |

| 10 hours | |

| Jul-09 | |

| May-06 | |

| May-06 | |

| May-06 | |

| May-05 | |

| May-05 | |

| Apr-17 | |

| Apr-02 | |

| Feb-11 | |

| Feb-06 | |

| Feb-05 | |

| Feb-04 | |

| Feb-04 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite