|

|

|

|

|||||

|

|

|

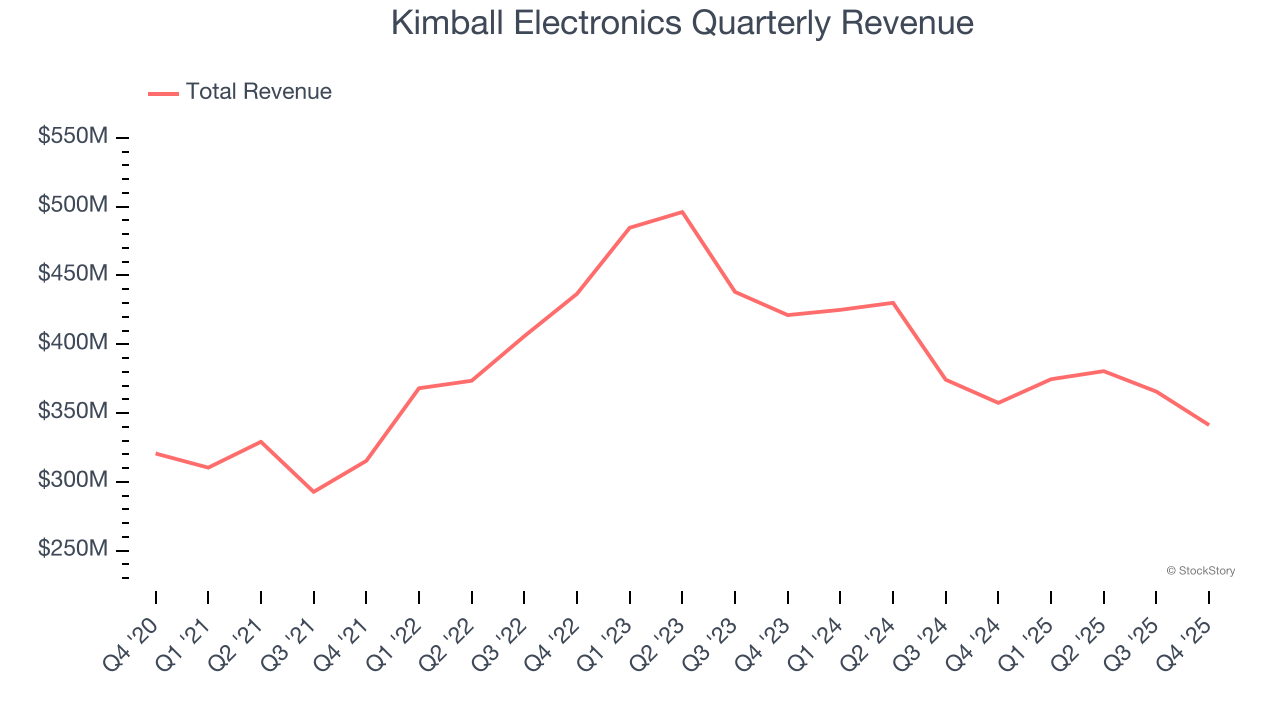

Global electronics contract manufacturer Kimball Electronics (NYSE:KE) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, but sales fell by 4.5% year on year to $341.3 million. The company’s full-year revenue guidance of $1.43 billion at the midpoint came in 1.9% above analysts’ estimates. Its non-GAAP profit of $0.28 per share was 9.8% above analysts’ consensus estimates.

Is now the time to buy Kimball Electronics? Find out by accessing our full research report, it’s free.

Commenting on today’s announcement, Richard D. Phillips, Chief Executive Officer, stated, “I’m pleased with the results for the second quarter and our updated guidance for fiscal 2026. Sales in Q2 were in line with expectations, highlighted by another quarter of strong double-digit year-over-year growth in the medical vertical, margins improved compared to the same period last year, and cash from operations was positive for the eighth consecutive quarter.”

Founded in 1961, Kimball Electronics (NYSE:KE) is a global contract manufacturer specializing in electronics and manufacturing solutions for automotive, medical, and industrial markets.

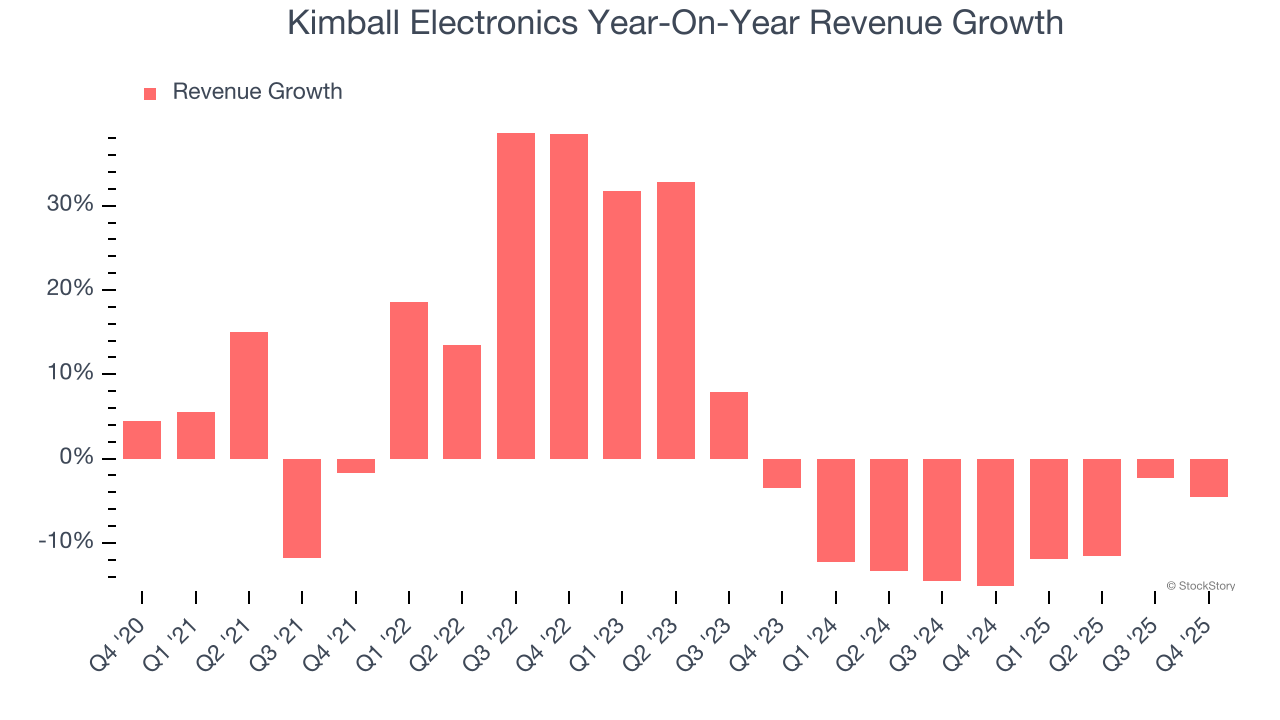

A company’s long-term sales performance is one signal of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Unfortunately, Kimball Electronics’s 3.5% annualized revenue growth over the last five years was sluggish. This was below our standard for the industrials sector and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Kimball Electronics’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 10.9% annually.

This quarter, Kimball Electronics’s revenue fell by 4.5% year on year to $341.3 million but beat Wall Street’s estimates by 0.6%.

Looking ahead, sell-side analysts expect revenue to decline by 1.3% over the next 12 months. Although this projection is better than its two-year trend, it’s tough to feel optimistic about a company facing demand difficulties.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

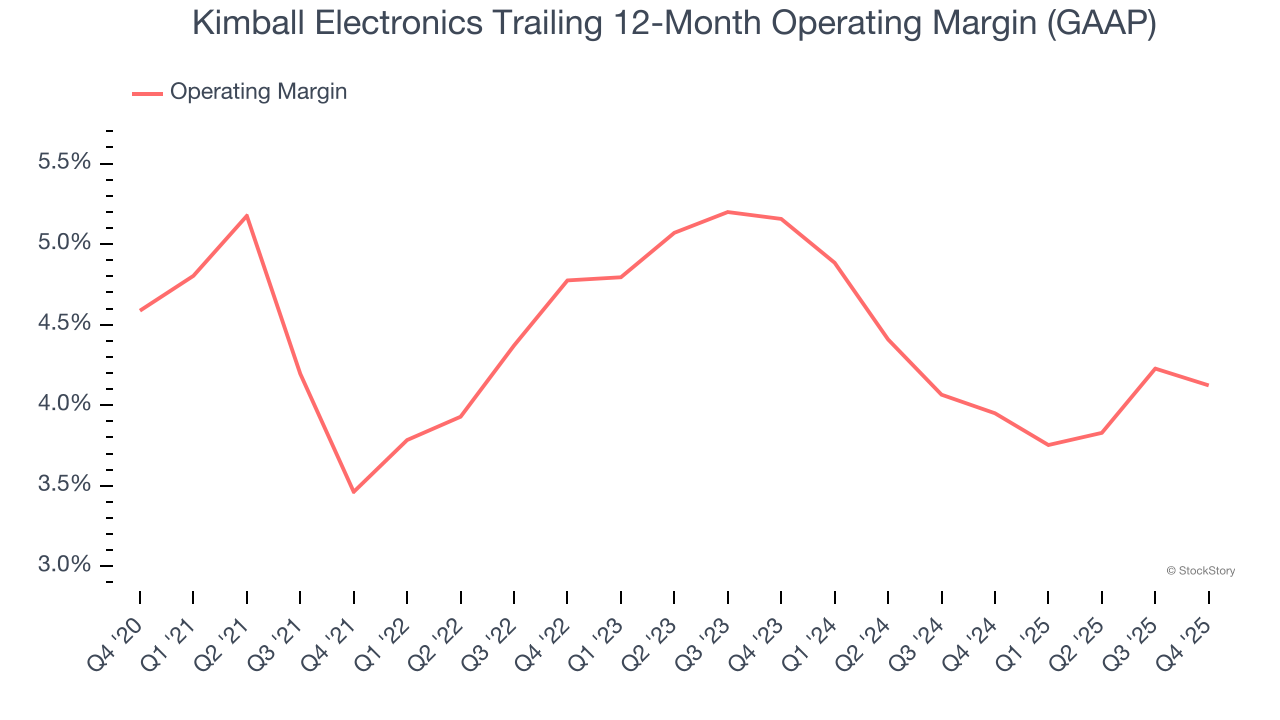

Kimball Electronics’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 4.4% over the last five years. This profitability was lousy for an industrials business and caused by its suboptimal cost structureand low gross margin.

Analyzing the trend in its profitability, Kimball Electronics’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Kimball Electronics generated an operating margin profit margin of 3.2%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

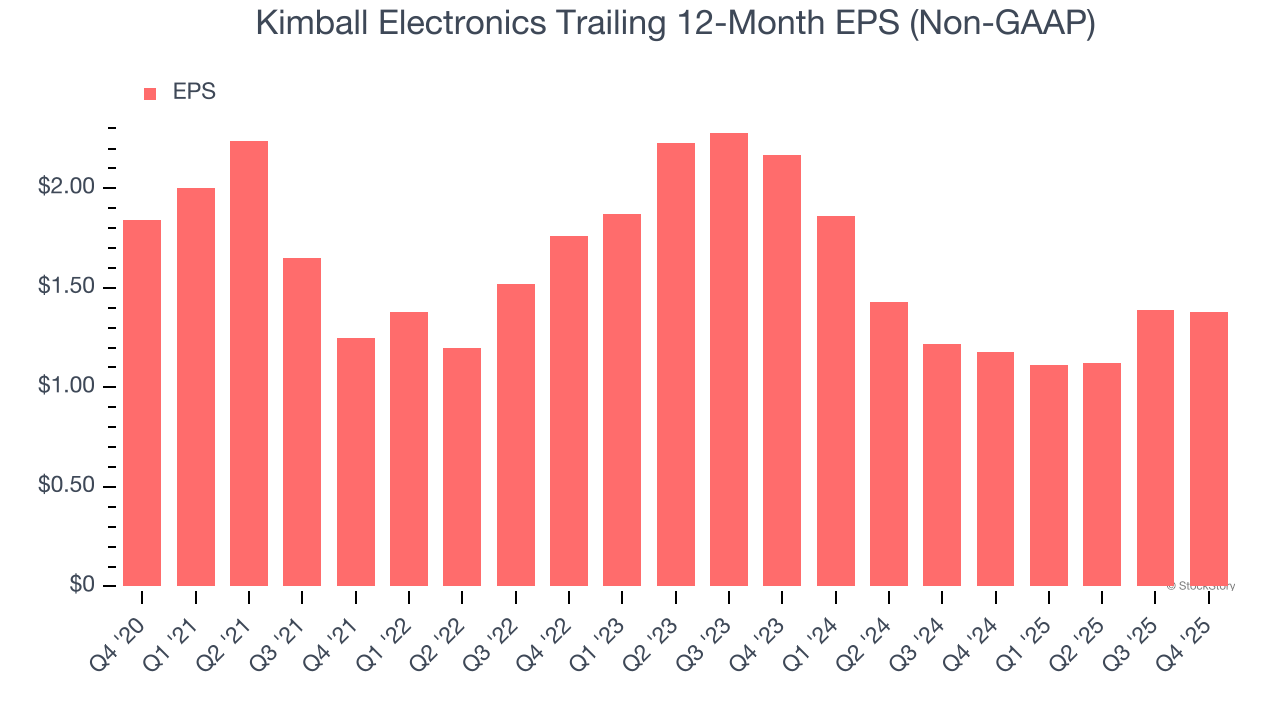

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Kimball Electronics, its EPS declined by 5.6% annually over the last five years while its revenue grew by 3.5%. However, its operating margin didn’t change during this time, telling us that non-fundamental factors such as interest and taxes affected its ultimate earnings.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Kimball Electronics, its two-year annual EPS declines of 20.3% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q4, Kimball Electronics reported adjusted EPS of $0.28, in line with the same quarter last year. This print beat analysts’ estimates by 9.8%. Over the next 12 months, Wall Street expects Kimball Electronics’s full-year EPS of $1.38 to shrink by 1.8%.

It was great to see Kimball Electronics’s full-year revenue guidance top analysts’ expectations. We were also glad its EPS outperformed Wall Street’s estimates. Overall, we think this was a decent quarter with some key metrics above expectations. The stock remained flat at $30.70 immediately following the results.

Sure, Kimball Electronics had a solid quarter, but if we look at the bigger picture, is this stock a buy? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).

| Jul-29 | |

| Jul-15 | |

| Jul-01 | |

| May-19 | |

| May-06 | |

| May-05 | |

| May-05 | |

| Apr-22 | |

| Mar-19 | |

| Mar-10 | |

| Mar-05 | |

| Feb-11 | |

| Feb-05 | |

| Feb-05 | |

| Feb-04 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite