|

|

|

|

|||||

|

|

|

Beauty products company Estée Lauder (NYSE:EL) met Wall Street’s revenue expectations in Q4 CY2025, with sales up 5.6% year on year to $4.23 billion. Its non-GAAP profit of $0.89 per share was 6.6% above analysts’ consensus estimates.

Is now the time to buy Estée Lauder? Find out by accessing our full research report, it’s free.

“We delivered excellent second quarter results to solidify a strong first half of fiscal 2026,” said Stéphane de La Faverie, President and CEO.

Named after its founder, who was an entrepreneurial woman from New York with a passion for skincare, Estée Lauder (NYSE:EL) is a one-stop beauty shop with products in skincare, fragrance, makeup, sun protection, and men’s grooming.

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

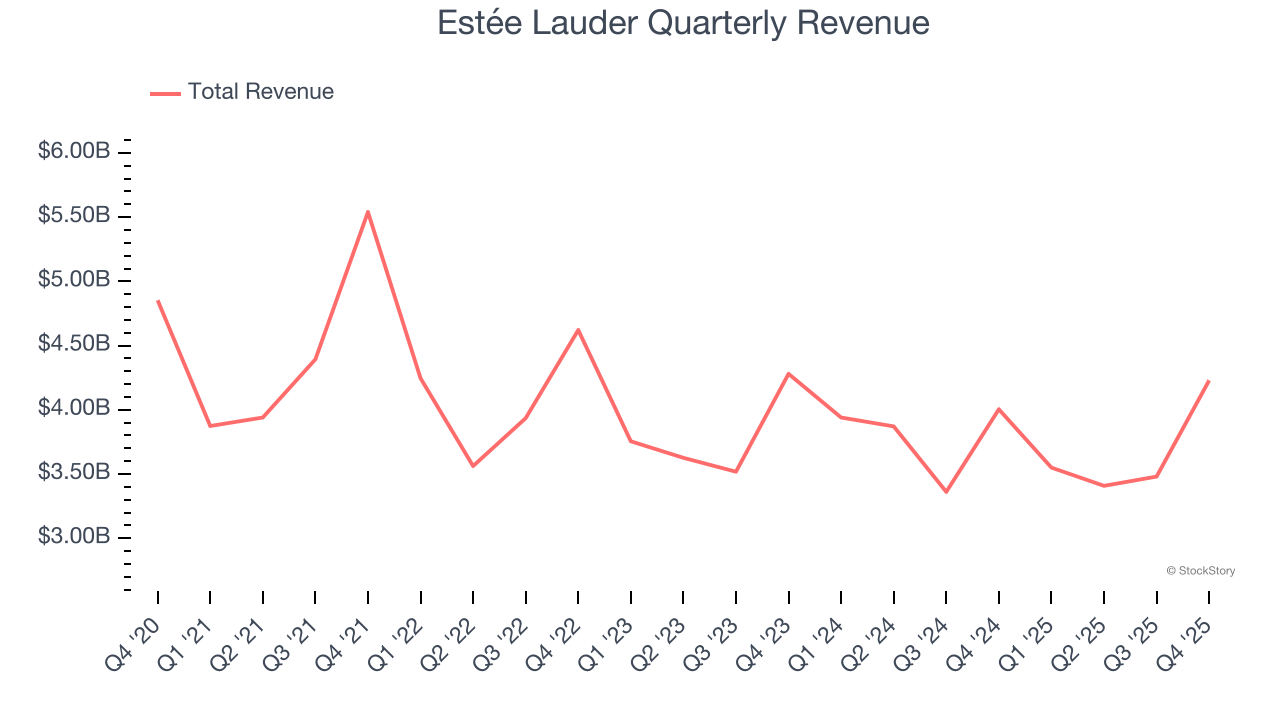

With $14.67 billion in revenue over the past 12 months, Estée Lauder is one of the larger consumer staples companies and benefits from a well-known brand that influences purchasing decisions. However, its scale is a double-edged sword because it’s harder to find incremental growth when your existing brands have penetrated most of the market. To accelerate sales, Estée Lauder likely needs to optimize its pricing or lean into new products and international expansion.

As you can see below, Estée Lauder’s demand was weak over the last three years. Its sales fell by 3.6% annually, a tough starting point for our analysis.

This quarter, Estée Lauder grew its revenue by 5.6% year on year, and its $4.23 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 4.2% over the next 12 months. While this projection indicates its newer products will spur better top-line performance, it is still below the sector average.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

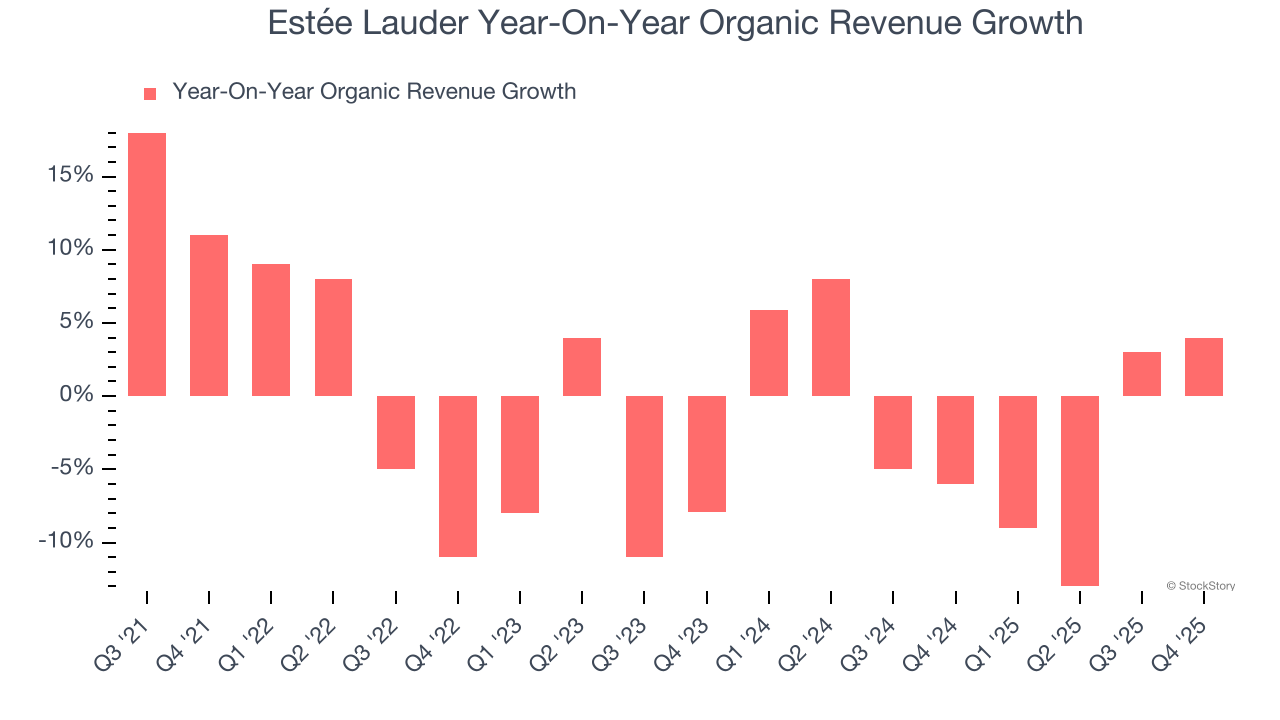

When analyzing revenue growth, we care most about organic revenue growth. This metric captures a business’s performance excluding one-time events such as mergers, acquisitions, and divestitures as well as foreign currency fluctuations.

Estée Lauder’s demand has been falling over the last eight quarters, and on average, its organic sales have declined by 1.5% year on year.

In the latest quarter, Estée Lauder’s organic sales rose by 4% year on year. This growth was a well-appreciated turnaround from its historical levels, showing the business is regaining momentum.

It was good to see Estée Lauder narrowly top analysts’ organic revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its full-year EPS guidance fell slightly short of Wall Street’s estimates. This guide is weighing on shares. The stock traded down 7.9% to $110.18 immediately after reporting.

Estée Lauder underperformed this quarter, but does that create an opportunity to invest right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).

| Jun-22 | |

| Jun-22 | |

| Jun-17 | |

| Jun-16 | |

| Jun-12 | |

| Jun-08 | |

| Jun-08 | |

| Jun-08 | |

| Jun-05 | |

| Jun-03 | |

| May-29 | |

| May-27 | |

| May-26 | |

| May-22 | |

| May-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite