|

|

|

|

|||||

|

|

|

Cardinal Health, Inc. CAH reported second-quarter fiscal 2026 adjusted earnings per share (EPS) of $2.63, which beat the Zacks Consensus Estimate of $2.39 by 10%. The bottom line also improved 36.3% year over year.

GAAP EPS in the quarter was $1.97 compared with $1.65 in the year-ago period.

Sales were up 18.6% on a year-over-year basis to $65.6 billion. The top line beat the Zacks Consensus Estimate by 0.9%.

Cardinal Health, Inc. price-consensus-eps-surprise-chart | Cardinal Health, Inc. Quote

Pharmaceutical and Specialty Solutions

Pharmaceutical revenues were up 19.3% to $60.67 billion on a year-over-year basis. This growth was driven by branded and specialty pharmaceutical sales growth from existing and new Pharmaceutical Distribution and Specialty Solutions customers.

Pharmaceutical profit totaled $687 million, up 29.4% from the year-ago period’s level. The upside was driven by growth in brand and specialty products and MSO platforms, and contributions from positive generics program performance.

Global Medical Products and Distribution

Revenues in this segment totaled $3.26 billion, up 3.3% year over year, driven by a rise in volume from existing customers.

The segment reported a profit of $37 million compared with $18 million in the year-ago quarter. The significant growth was driven by a rise in existing customers and benefits from cost optimization initiatives, partially offset by tariff headwinds.

Other

This segment includes three operating segments — at-Home Solutions, Nuclear and Precision Health Solutions, and OptiFreight Logistics. Sales totaled $1.72 billion, up 34.4% year over year.

The segment’s profit amounted to $179 million, up 51.7% from the year-ago level. The upside was driven by robust performance across the three operating segments.

Gross profit increased 23.5% year over year to $2.4 billion.

As a percentage of revenues, the gross margin in the reported quarter was 3.7%, up almost 15 basis points year over year.

Distribution, selling, general and administrative expenses totaled $1.5 billion, up 15.2% year over year.

Operating income amounted to $707 million, up 28.8% year over year. Adjusted operating income increased 38.1% year over year to $877 million.

The company exited the reported quarter with cash and cash equivalents of $2.78 billion compared with $4.59 billion in the fiscal first quarter.

Net cash provided by operating activities totaled $1.66 billion against $2.04 billion in net cash used in the year-ago period.

Cardinal Health raised its fiscal 2026 earnings guidance. The company anticipates adjusted EPS to be between $10.15 and $10.35 (23-26% growth), up from the previously outlook of at least $10.00 issued at the J.P. Morgan Health conference held last month. The Zacks Consensus Estimate for the same is pegged at $10.04.

The company continues to expect revenues from its Pharmaceutical segment to grow 11-13% year over year. Segmental profit is likely to increase 20-22%, up from the previous guidance of 16-19%.

Revenues from the Medical segment are estimated to grow 2-4%. Segmental profit is now expected to be approximately $150 million versus the earlier guidance of at least $140 million.

Revenues from the Other segment are likely to grow 26-28%. Segmental profit is now expected to increase 33-35% versus the previous guidance of 29-31%.

Cardinal Health reported robust second-quarter fiscal 2026 results, with earnings and sales beating estimates. Quarterly results were marked by broad-based profit growth across all operating segments. Pharmaceutical and Specialty Solutions benefited from robust brand and specialty drug sales, while Global Medical Products and Distribution posted double-digit profit gains on higher volumes. The Other segment also saw significant expansion, supported by acquisitions and growth in at-Home Solutions, Nuclear and Precision Health Solutions, and logistics services.

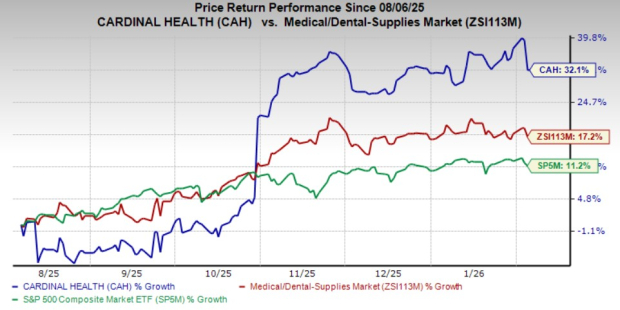

Following positive results, shares of CAH were up 1% in pre-market trading. The company’s shares have gained 32.1% so far this year compared with the industry’s 17.2% growth. The S&P 500 Index has gained 11.2% in the period.

The company’s recently closed Solaris acquisition should boost sales growth in the second half of 2026 with its strong presence in the United States as the leading Urology MSO. The BioPharma Solution platform looks promising on the back of Sonexus Access and Patient Support, which is gaining momentum as several leading pharma companies like Sanofi and Regeneron have selected it for their patient support hub programs.

As part of the continued integration of the Advanced Diabetes Supply Group with its at-Home Solutions business, CAH has launched ContinuCare Pathway program. The program will simplify diabetes supply management and enhance patient access. With Publix Super Markets enrolling its entire pharmacy network of nearly 1,400 pharmacies in the program, the ContinuCare Pathway program is now available to over 11,000 retail and grocery pharmacies.

The strong momentum in its MSO platforms, along with more than 30% anticipated in the BioPharma Solutions sales and strong demand across specialty distribution, is likely to support Specialty revenues to cross $50 billion in fiscal 2026. With solid momentum across all five segments and a raised full-year outlook, Cardinal Health enters the remainder of fiscal 2026 with confidence.

Cardinal Health carries a Zacks Rank #2 (Buy) at present.

Some other top-ranked stocks in the broader medical space are Boston Scientific Corporation BSX, Phibro Animal Health PAHC and AtriCure ATRC, each presently carrying a Zacks Rank #2. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Boston Scientific shares have lost 12% in the past six months. Estimates for the company’s fourth-quarter 2025 EPS have remained constant at 78 cents in the past 30 days. BSX’s earnings beat estimates in each of the trailing four quarters, delivering an average surprise of 7.36%. In the last reported quarter, it posted an earnings surprise of 5.63%.

Estimates for Phibro Animal Health’s second-quarter fiscal 2026 EPS have remained constant at 69 cents in the past 30 days. Shares of the company have risen 50.5% in the past six months compared with the industry’s 11.1% growth. PAHC’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 20.77%. In the last reported quarter, it delivered an earnings surprise of 23.73%.

AtriCure shares have risen 5.2% in the past six months. Estimates for the company’s fourth-quarter 2025 loss per share have remained stable at 4 cents in the past 30 days. ATRC’s earnings beat estimates in each of the trailing four quarters, delivering an average surprise of 67.06%. In the last reported quarter, it posted an earnings surprise of 90.91%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 57 min | |

| 2 hours | |

| Aug-10 | |

| Aug-10 | |

| Aug-05 | |

| Jul-31 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 |

Boston Scientific reports positive Q2 results yet opts to trim 2026 outlook

BSX

Medical Device Network

|

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite