|

|

|

|

|||||

|

|

|

Microsoft MSFT shares have experienced significant turbulence following the company's second-quarter fiscal 2026 earnings release on Jan. 28, losing approximately 14% from their pre-earnings levels. Despite beating both revenue and earnings estimates, with non-GAAP earnings per share of $4.14 surpassing expectations and revenue reaching $81.3 billion, representing 17% year-over-year growth, the stock faced immediate selling pressure.

The disconnect between strong operational performance and negative market reaction reflects growing investor scrutiny over capital expenditure intensity and the timeline for artificial intelligence infrastructure investments to generate meaningful returns.

The cloud infrastructure segment remains Microsoft's primary growth engine, though mixed signals emerged from the quarterly results. Azure and other cloud services grew 39% in constant currency during the quarter, a modest deceleration from the 40% growth achieved in the fiscal first quarter. Microsoft Cloud revenues crossed the $50 billion quarterly threshold for the first time, reaching $51.5 billion with 26% year-over-year growth. However, the company's gross margin compressed to just over 68%, marking the narrowest level in three years as substantial investments in AI infrastructure weighed on profitability. Management acknowledged continuing capacity constraints through at least the fiscal year-end, with demand significantly exceeding current infrastructure buildout, resulting in lost revenue opportunities.

The commercial bookings picture painted a more encouraging narrative. Commercial bookings growth surged to 230% from 112% in the previous quarter, while commercial remaining performance obligation reached $625 billion, representing 110% year-over-year growth. This massive backlog demonstrates robust enterprise demand for Microsoft's cloud and AI offerings, suggesting sustained revenue visibility extending well into future quarters. The Productivity and Business Processes segment generated $34.1 billion in revenues with 16% growth, reflecting steady adoption of Microsoft 365 services across the company's installed base of more than 450 million paid commercial seats. LinkedIn and Dynamics business applications contributed to this segment's consistent performance trajectory.

Challenges emerged within the More Personal Computing division, which declined approximately 3% to $14.25 billion in revenues. Gaming revenues fell 9.5% as the company took an unspecified impairment charge during the quarter, while Windows OEM revenues faced headwinds despite the October end of support for Windows 10, driving some upgrade activity. These declines partially offset the strength in cloud services and underscore the portfolio's uneven performance across different business lines.

Looking ahead, Microsoft's fiscal third-quarter guidance projects revenues between $80.65 billion and $81.75 billion, implying growth of approximately 15% to 17%. The Zacks Consensus Estimate for MSFT’s third-quarter fiscal 2026 earnings is projected at $4.04 per share, up 4.1% over the past 30 days. The estimate indicates 16.76% year-over-year growth.

The company expects Azure revenue growth of 37% to 38% in constant currency, though this guidance incorporates continued capacity constraints limiting growth potential. Operating margins are anticipated to decline slightly year over year for the quarter, though management raised full fiscal year 2026 operating margin expectations to slight growth, aided by first-half investment prioritization and favorable revenue mix shifts. Rising memory prices present an additional headwind, with management noting potential impacts on both Windows OEM markets and capital expenditure requirements, though effects on Microsoft Cloud gross margins will build gradually as assets depreciate over their six-year useful lives.

Microsoft Corporation price-consensus-chart | Microsoft Corporation Quote

Recent company developments in early 2026 have focused on expanding AI capabilities across the product portfolio. In January, Microsoft rolled out agent mode features in Excel, enabling users to work alongside AI assistants that actively edit spreadsheets while reasoning through changes. The company has also enhanced Copilot in Outlook mobile with interactive voice experiences for email summarization and triage actions. Windows updates introduced cross-device resume functionality, expanding from Android phones to PCs, alongside improvements to narrator controls and voice access setup experiences. These incremental enhancements demonstrate ongoing efforts to embed AI throughout the Microsoft ecosystem, though monetization of these features remains in early stages.

Microsoft currently trades at a forward price-to-sales ratio of 8.67 times, representing a significant premium to the Zacks Computer-Software industry average of 7.03 times. This elevated valuation reflects the market's recognition of Microsoft's dominant cloud position but leaves limited room for execution missteps.

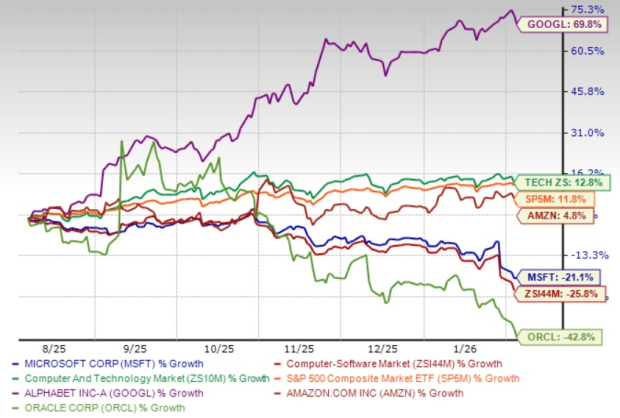

Microsoft shares have lost 21.1% over the past six months, underperforming the broader Zacks Computer and Technology sector. Cloud competitors Alphabet GOOGL and Amazon AMZN have returned 69.8% and 4.8%, respectively, while shares of Oracle ORCL have lost 42.8% in the same time frame.

Alphabet benefits from lower capital intensity in its AI infrastructure approach, with Google Cloud revenues growing 48% year over year while maintaining improved profitability in the fourth quarter of 2025. Alphabet's diversified revenue streams and custom TPU development provide competitive differentiation against Microsoft's NVIDIA-dependent infrastructure. Amazon Web Services remains the largest cloud provider with superior scale economics, recently signing a $38 billion contract with OpenAI and committing over $100 billion in capital expenditures for 2025.

Amazon's established customer base and pricing power position AWS favorably against Microsoft Azure's growth trajectory. Oracle represents an emerging threat with its AI-optimized Oracle Cloud Infrastructure, having accumulated a $523 billion remaining performance obligation and targeting aggressive expansion. Oracle's multicloud partnerships and purpose-built AI infrastructure have attracted significant enterprise commitments, intensifying competition for high-performance computing workloads that Microsoft and Amazon also pursue aggressively in this rapidly evolving market landscape.

For investors considering Microsoft at current levels, the investment case presents competing considerations requiring careful evaluation. The company's strong competitive positioning in enterprise cloud, massive backlog of contracted future revenues and leadership in generative AI applications through partnerships and internal development provide substantial long-term growth foundations. However, the combination of elevated capital expenditure requirements, compressed margins during the infrastructure buildout phase, and capacity constraints limiting near-term growth creates uncertainty around the pace of financial performance improvement. Investors might consider holding existing positions while monitoring quarterly execution, or waiting for more attractive entry points if market volatility creates opportunities later in 2026 as infrastructure investments begin translating into accelerated revenue growth and margin expansion. Microsoft currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-25 | |

| Jul-25 | |

| Jul-25 | |

| Jul-25 | |

| Jul-25 |

Dow Jones Futures: Market Triggers Sell Signal; Apple Earnings, Iran News, Fed Meeting In Focus

AMZN MSFT

Investor's Business Daily

|

| Jul-25 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

What to watch next week: Big Tech earnings, the Fed, and Consumer Confidence

GOOGL MSFT

Yahoo Finance Video

|

| Jul-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite