|

|

|

|

|||||

|

|

|

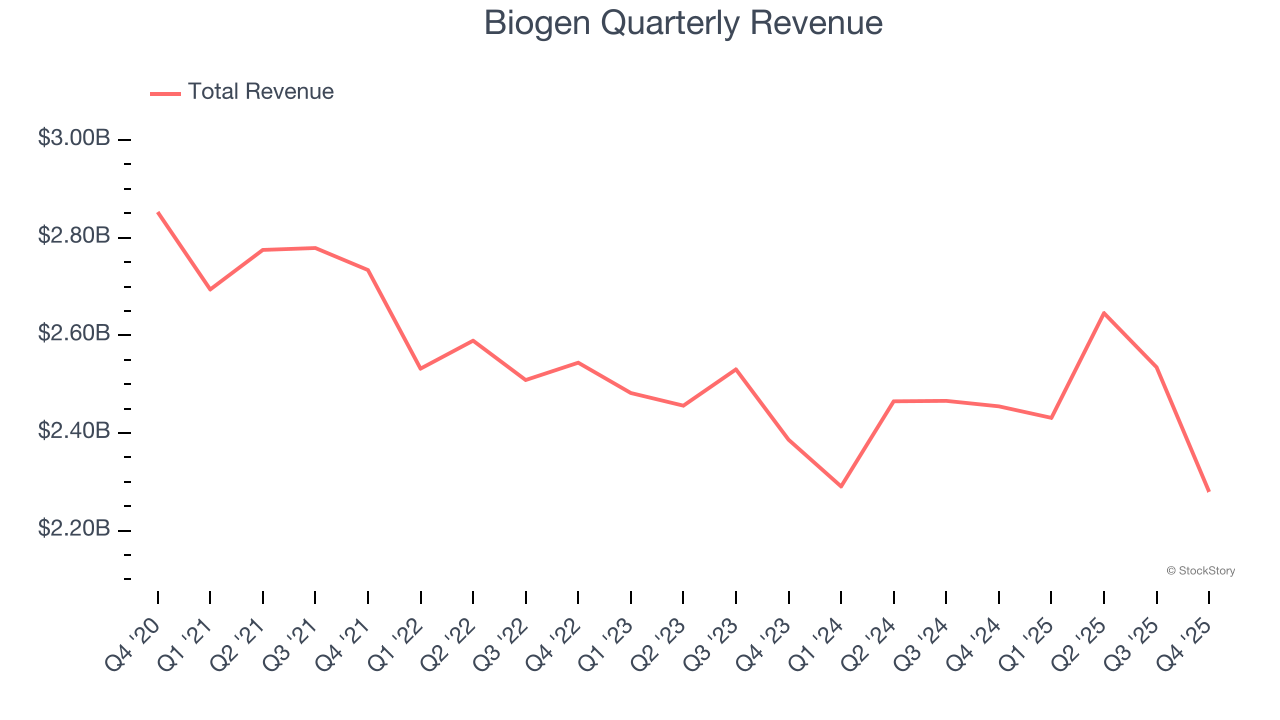

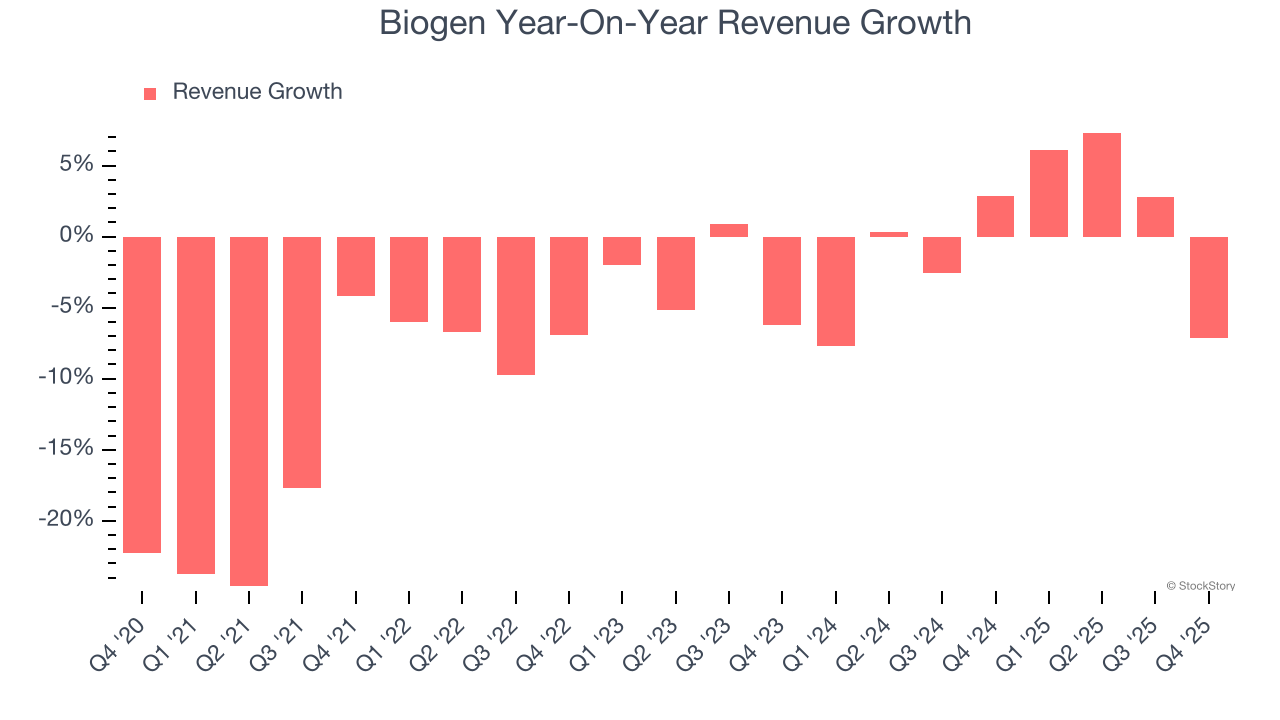

Biotech company Biogen (NASDAQ:BIIB) reported Q4 CY2025 results topping the market’s revenue expectations, but sales fell by 7.1% year on year to $2.28 billion. Its non-GAAP profit of $1.99 per share was 22.1% above analysts’ consensus estimates.

Is now the time to buy Biogen? Find out by accessing our full research report, it’s free.

Founded in 1978 and pioneering treatments for some of medicine's most complex challenges, Biogen (NASDAQ:BIIB) develops and markets therapies for neurological conditions, including multiple sclerosis, Alzheimer's disease, spinal muscular atrophy, and rare diseases.

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Biogen’s demand was weak over the last five years as its sales fell at a 6% annual rate. This wasn’t a great result and suggests it’s a low quality business.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Biogen’s revenue over the last two years was flat, sugggesting its demand was weak but stabilized after its initial drop.

This quarter, Biogen’s revenue fell by 7.1% year on year to $2.28 billion but beat Wall Street’s estimates by 3.6%.

Looking ahead, sell-side analysts expect revenue to decline by 6.6% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and suggests its products and services will face some demand challenges.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

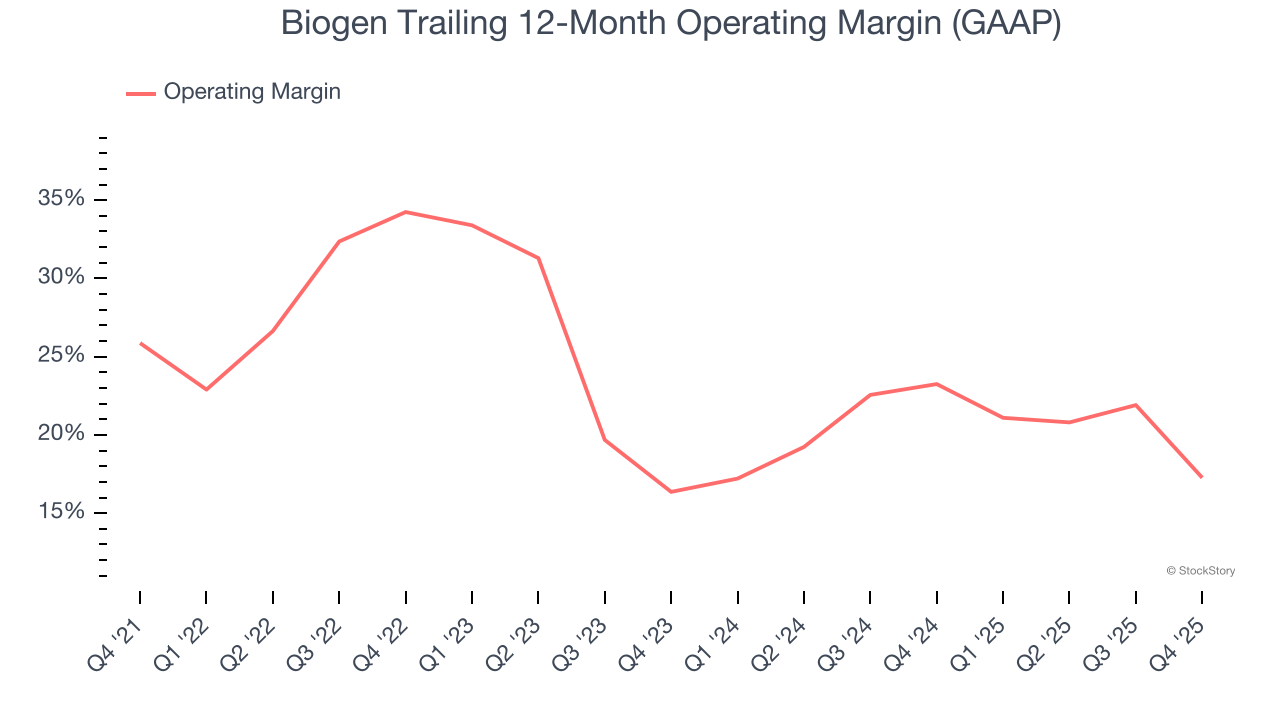

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Biogen has been an efficient company over the last five years. It was one of the more profitable businesses in the healthcare sector, boasting an average operating margin of 23.5%.

Analyzing the trend in its profitability, Biogen’s operating margin decreased by 8.6 percentage points over the last five years. Even though its historical margin was healthy, shareholders will want to see Biogen become more profitable in the future.

In Q4, Biogen generated an operating margin profit margin of negative 2.5%, down 20.4 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

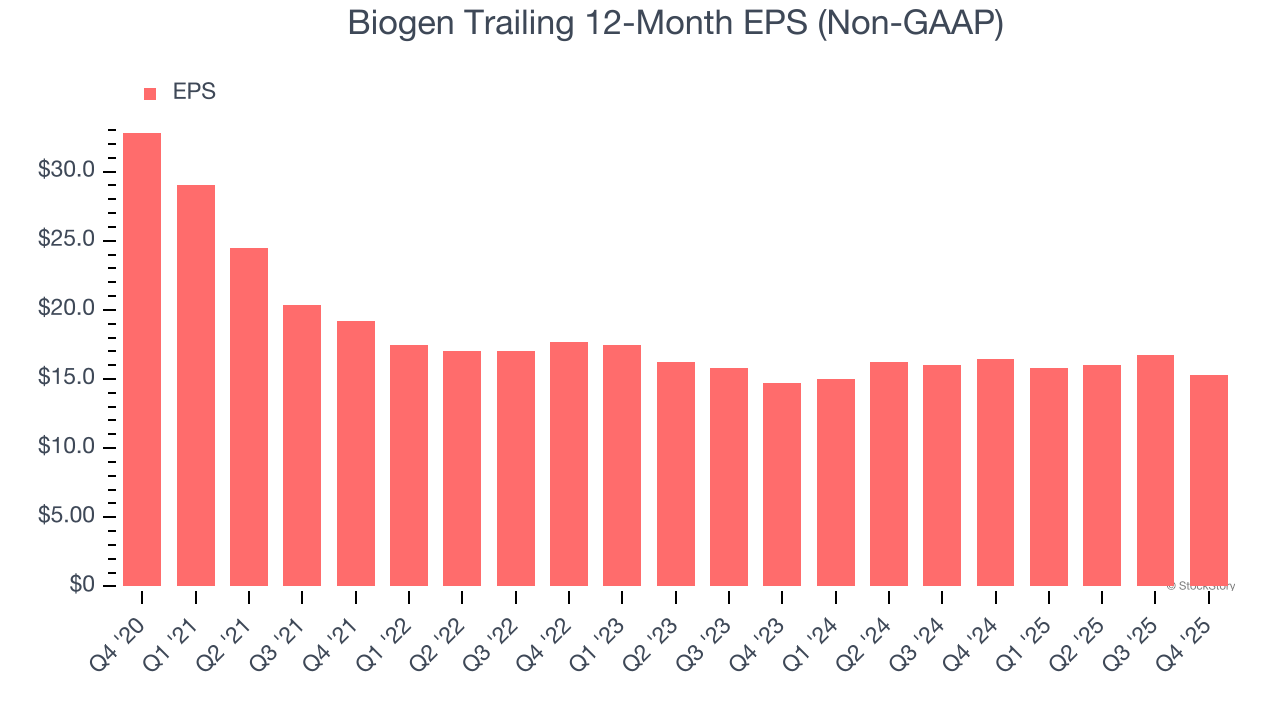

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Biogen, its EPS declined by 14.2% annually over the last five years, more than its revenue. We can see the difference stemmed from higher interest expenses or taxes as the company actually improved its operating margin and repurchased its shares during this time.

We can take a deeper look into Biogen’s earnings to better understand the drivers of its performance. As we mentioned earlier, Biogen’s operating margin declined by 8.6 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, Biogen reported adjusted EPS of $1.99, down from $3.44 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Biogen’s full-year EPS of $15.29 to shrink by 5.6%.

We were impressed by how significantly Biogen blew past analysts’ full-year EPS guidance expectations this quarter. We were also glad its revenue and EPS in the reported quarter outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock remained flat at $185.89 immediately following the results.

Biogen may have had a good quarter, but does that mean you should invest right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).

| Apr-27 | |

| Apr-24 |

Biogen seeks Darzalex rivalry in China for multiple myeloma with felzartamab deal

BIIB

Pharmaceutical Technology

|

| Apr-22 | |

| Apr-22 | |

| Apr-22 | |

| Apr-20 | |

| Apr-20 | |

| Apr-18 | |

| Apr-16 | |

| Apr-14 | |

| Apr-08 | |

| Apr-08 | |

| Apr-07 | |

| Apr-07 | |

| Apr-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite