|

|

|

|

|||||

|

|

|

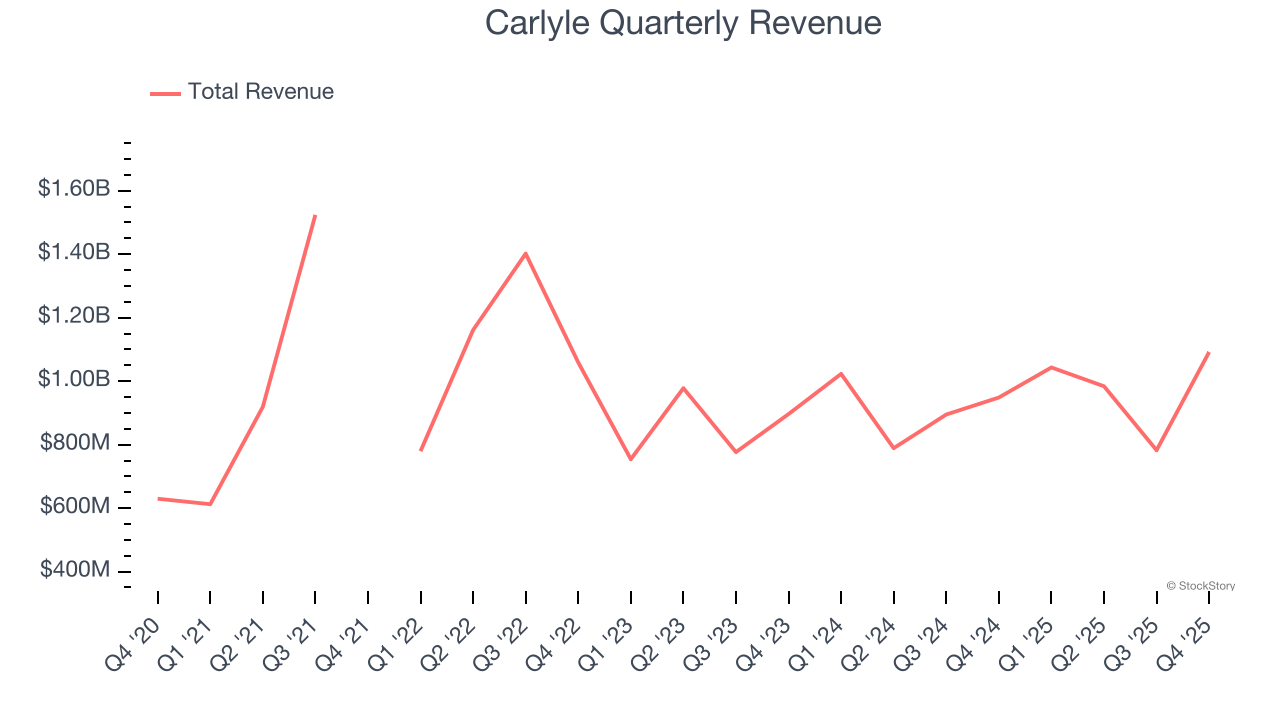

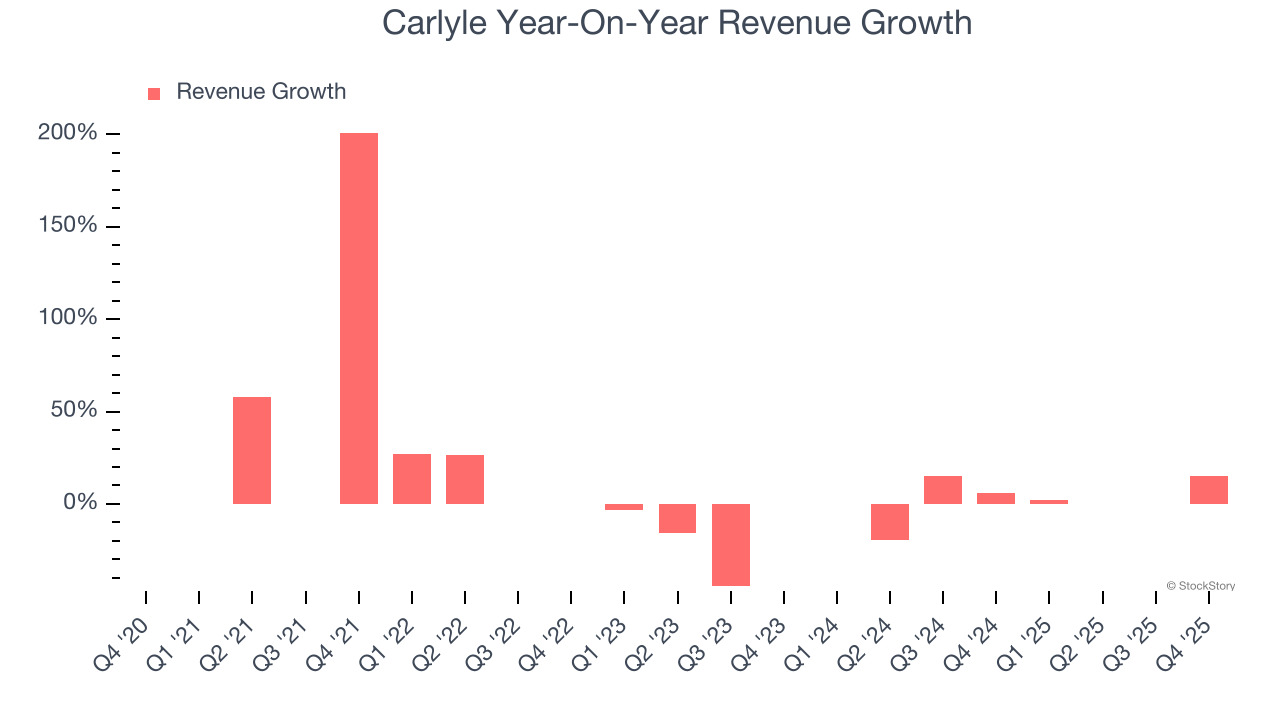

Private equity firm Carlyle Group (NASDAQ:CG) reported Q4 CY2025 results topping the market’s revenue expectations, with sales up 15.1% year on year to $1.09 billion. Its non-GAAP profit of $1.01 per share was 1.7% above analysts’ consensus estimates.

Is now the time to buy Carlyle? Find out by accessing our full research report, it’s free.

Founded in 1987 with just $5 million in capital and named after the iconic New York hotel where the founders first met, The Carlyle Group (NASDAQ:CG) is a global investment firm that raises, manages, and deploys capital across private equity, credit, and investment solutions.

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Luckily, Carlyle’s revenue grew at a solid 11.2% compounded annual growth rate over the last five years. Its growth surpassed the average financials company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Carlyle’s recent performance shows its demand has slowed as its annualized revenue growth of 7% over the last two years was below its five-year trend.

This quarter, Carlyle reported year-on-year revenue growth of 15.1%, and its $1.09 billion of revenue exceeded Wall Street’s estimates by 3.7%.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

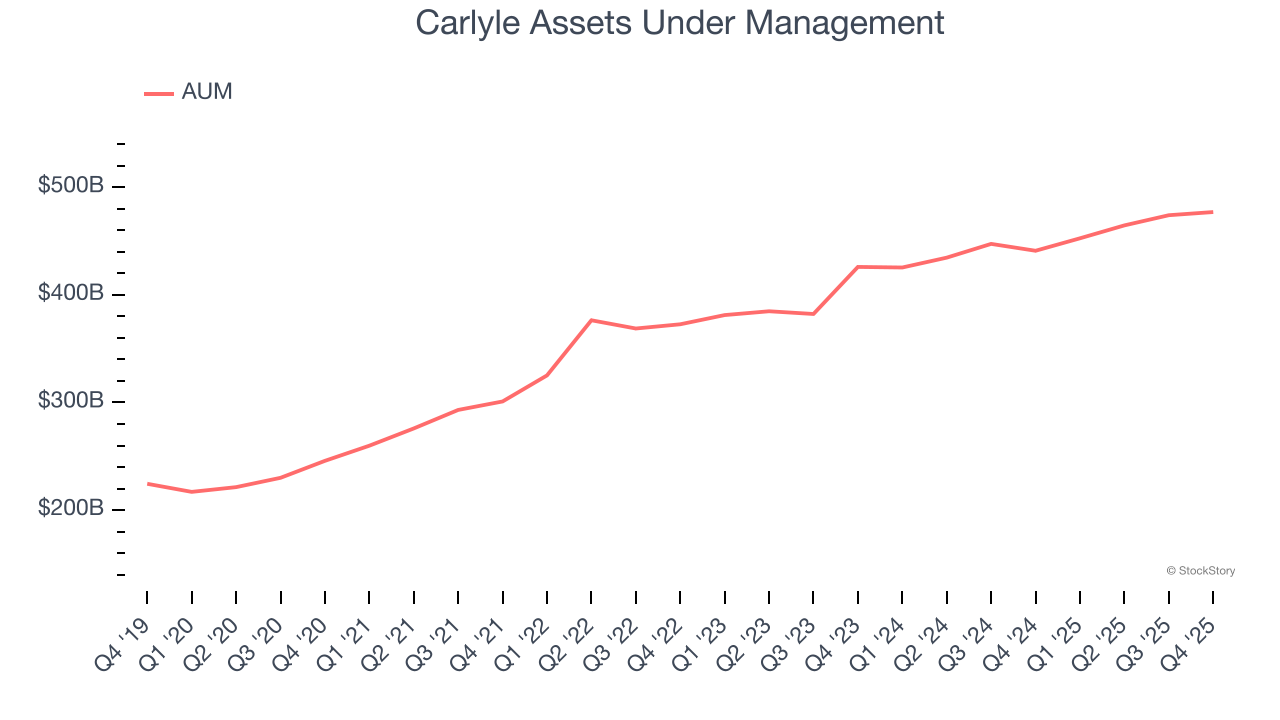

Assets Under Management (AUM) is the total capital a firm oversees or manages on behalf of clients. Fees on this AUM, typically a small percentage, are contractually recurring and provide a high level of stability to revenue even if investment performance lags (although too much poor investment performance eventually hurts fundraising ability).

Carlyle’s AUM has grown at an annual rate of 15.4% over the last five years, better than the broader financials industry and faster than its total revenue. When analyzing Carlyle’s AUM over the last two years, we can see that growth decelerated to 8.9% annually. Fundraising or short-term investment performance were net contributors for the company over this shorter period since assets grew faster than total revenue. But again, we put less weight on asset growth given how lumpy and cyclical it can be.

Carlyle’s AUM punched in at $477 billion this quarter, meeting analysts’ expectations. This print was 8.2% higher than the same quarter last year.

It was encouraging to see Carlyle beat analysts’ revenue expectations this quarter. We were also happy its fee-related earnings outperformed Wall Street’s estimates. Overall, this print had some key positives. The stock traded up 1.5% to $56.25 immediately following the results.

Carlyle put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).

| Jul-21 | |

| Jul-13 | |

| Jul-07 | |

| Jun-24 | |

| Jun-24 | |

| Jun-23 | |

| Jun-16 | |

| Jun-09 |

Carlyle finalises $2.8bn acquisition of majority stake in MAI Capital

CG

Private Banker International

|

| Jun-08 | |

| Jun-08 | |

| Jun-08 | |

| Jun-05 | |

| Jun-04 | |

| Jun-02 | |

| Jun-02 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite