|

|

|

|

|||||

|

|

|

Jabil, Inc. JBL has gained 26% in the past three months compared with the Electronic Manufacturing Services industry’s growth of 4.4%. It has outperformed the Zacks Computer & Technology sector and the S&P 500’s growth during this period.

Among its competitors, the company has outperformed Flex Ltd. FLEX and Celestica, Inc. CLS. Celestica has declined 3.7%, while Flex has gained 7.4%.

AI is driving a structural shift across the sector. This is not a short-term spike. Enterprises across industries are rushing to integrate AI capabilities across operations to streamline workflow, enhance productivity and boost competitive edge. This is pushing hyperscalers like Amazon, Microsoft and Google to rapidly expand the AI data center market infrastructure. Per a report from Grand View Research, the AI data center market was valued at $147.28 billion in 2025. It is projected to reach $810.61 billion with a compound annual growth rate of 23.9% from 2026 to 2033. Jabil is placing strong emphasis to expand its AI native portfolio to capitalize on this emerging market trend.

Jabil has strengthened its capabilities in liquid cooling and thermal management with strategic acquisitions. Jabil boasts strong capability in chip-level cooling, rack-level cooling and network cooling that can support increasing AI power density in data centers. Its fully integrated systems that combine compute, networking, power distribution and advanced cooling reduce the deployment time and reduce total cost of ownership for hyperscalers.

Owing to these factors, the company is witnessing healthy traction among hyperscaler customers. Its second hyperscaler customer revenue is now nearing $1 billion. It is also steadily investing in increasing its manufacturing capacity in the United States. This will likely strengthen Jabil’s position in the AI hardware supply chain and boost its competitive edge against other players in the AI data center vertical, such as Flex and Celestica.

Jabil’s diversified portfolio reduces its vulnerability to business cycles and macro headwinds. The company is witnessing healthy traction in the healthcare market. Demand for drug delivery platforms, including GLP-1, continuous glucose monitors, diagnostics & minimally invasive devices, remained strong. The healthcare portfolio is expected to be a multiyear growth engine for the company. Jabil’s automation, robotics, and warehouse solutions portfolio is also witnessing solid demand.

Over the past few years, Jabil has built a strong supply chain network. The company has a strong presence in more than 25 countries worldwide. Its worldwide connected factory network allows it scale up production as per evolving market dynamics. This improves factory resource utilization, enhances working capital efficiency and also helps in inventory management. Amid growing geopolitical unrest, trade and tariff-related uncertainty, Jabil’s multi-region presence has boosted its reliability to its customers. Jabil is focusing on localizing its manufacturing units to cater to regional demands.

As per the first quarter of fiscal 2026, Jabil’s free cash flow stands at $272 million compared to $226 million a year ago. This highlights efficient financial management practices and optimum utilization of assets. The company remains committed to generating more than $1.3 billion in free cash flow in fiscal 2026.

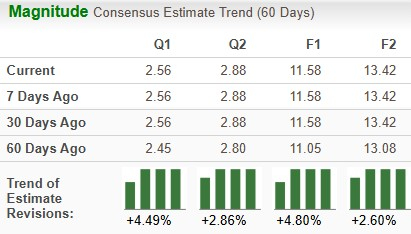

Earnings estimates for Jabil for 2025 have moved up 4.8% to $11.58 over the past 60 days, while the same for 2026 has increased 2.6% to $13.42.

From a valuation standpoint, JBL appears to be relatively cheaper than the industry but above its mean. Going by the price/earnings ratio, the company shares currently trade at 21.44 forward earnings, lower than 24.31 for the industry but above its mean of 20.14.

The AI data center market will likely remain a major growth driver for the company in the upcoming quarters. However, Jabil’s diverse market presence significantly enhances its resilience and reduces exposure to downtrend in any single end market. Healthcare, robotics and warehouse automation will likely drive growth. Capital discipline and strong cash flow will allow investment in growth initiatives, drive innovation and ensure greater value for investors. The upward estimate revision depicts bullish sentiments for the stock. With a Zacks Rank #2 (Buy) and attractive valuation, Jabil appears to be a good investment option right now. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-28 | |

| Jul-28 | |

| Jul-28 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite