|

|

|

|

|||||

|

|

|

With the rise of artificial intelligence (AI), NVIDIA Corporation NVDA has delivered impressive returns, soaring more than 1,000% over the past five years. Yet, in the past year, Micron Technology, Inc.’s MU shares outpaced NVIDIA’s (+307% vs +43.1%). Let’s see why Micron is emerging as the new go-to AI investment, even amid NVIDIA’s strong bullish momentum.

NVIDIA remains the center of attraction among investors, and for good reasons. Consistently, NVIDIA delivered encouraging quarterly results that exceeded Wall Street expectations even in the face of several geopolitical hurdles. This is because demand for its next-generation Blackwell chips and cloud graphics processing units (GPUs) remains strong.

Somewhat easing of the U.S.-China trade tensions and incessant increase in data center spending, in all likelihood, could boost NVIDIA’s sales. NVIDIA remains optimistic about its future growth and expects revenues for the fiscal fourth quarter of 2026 to hit nearly $65 billion, plus or minus 2%, according to investor.nvidia.com. This would be more than the company’s fiscal third-quarter 2026 revenues of $57 billion, and if achieved, it will surely raise the stock further (read more: NVIDIA vs. Palantir: One AI Stock is a Clear Buy Right Now).

While NVIDIA continues to command the spotlight, another chipmaker, Micron, has steadily gained investors’ attention, driven by strong demand for its high-bandwidth memory (HBM) chips amid the rapid expansion of AI.

The demand for Micron’s HBM chips has surged as data center operators and hyperscalers ramp up AI infrastructure investments. At the same time, constrained HBM supply amid high demand is likely to enhance Micron’s profit margin and support its growth trajectory. Micron CEO Sanjay Mehrotra also added that tight HBM supply is expected to persist as demand remains strong, creating a demand-supply imbalance that could push prices higher and benefit Micron in the near future.

Against this backdrop, Micron is quite optimistic about its financial performance, with management expecting fiscal second-quarter 2026 revenues to come between $18.3 billion and $19.1 billion, more than the $13.64 billion reported in first-quarter fiscal 2026, according to investors.micron.com. The company also expects net income to increase further.

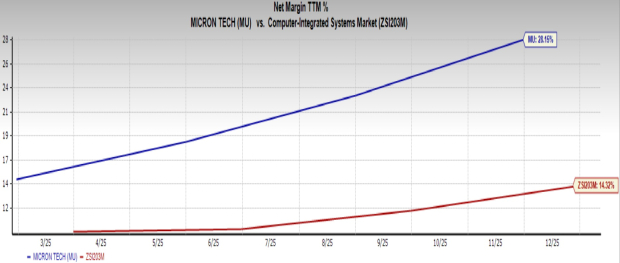

Micron is gaining investors’ attention as AI-driven HBM demand and tight supply bolster its growth outlook. Micron’s net profit margin of 28.2%, more than the Computer - Integrated Systems industry's 14.3%, also clearly suggests strong growth potential.

Image Source: Zacks Investment Research

Moreover, Micron offers an attractive buying opportunity at a reasonable valuation. Micron’s forward price-to-earnings (P/E) ratio of 11.66 is well below the industry’s average of 18.18.

Image Source: Zacks Investment Research

Therefore, from an investment standpoint, Micron is too promising to ignore right now. Its Zacks Consensus Estimate of $32.9 for earnings per share (EPS) implies growth of 204.3% year over year.

Image Source: Zacks Investment Research

Currently, Micron sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 52 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 5 hours | |

| Aug-09 | |

| Aug-09 | |

| Aug-09 | |

| Aug-09 | |

| Aug-09 | |

| Aug-09 | |

| Aug-09 | |

| Aug-09 | |

| Aug-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite