|

|

|

|

|||||

|

|

|

U.S. legacy automaker Ford F ended 2025 on a weak note, snapping its four-quarter earnings beat streak. The company posted sharply disappointing fourth-quarter 2025 results, incurring a net loss of $11.1 billion on a GAAP basis versus a profit of $1.8 billion in the corresponding quarter of 2024. On a non-GAAP basis, EPS came in at 13 cents, missing the Zacks Consensus Estimate of 17 cents and declining 26% year over year.

The weak performance was largely due to a combination of one-off disruptions and policy-related costs. Ford took roughly $2 billion in losses linked to fires at a Novelis aluminum supplier plant in New York. The company also faced a $2 billion net tariff headwind, including about $1 billion in unexpected costs after auto-parts tariff credits were delayed. Results were further weighed down by $15.5 billion in special charges, primarily tied to scaling back its all-electric vehicle (EV) plans announced in December.

While not all of these pressures are expected to fade quickly, the key question for investors is whether Ford’s outlook points to stabilization and recovery. Let’s assess whether the stock still makes sense to own at current levels.

Ford Motor Company price-consensus-eps-surprise-chart | Ford Motor Company Quote

Management acknowledged that the quarter was messy and that while some challenges will linger, the worst of the headwinds are already behind the company.

In December, Ford said it would take $19.5 billion in charges as it reset its EV strategy. Big, expensive projects that no longer made economic sense—such as a three-row electric SUV, an electric commercial van and a next-gen electric pickup—have been scrapped. Instead, Ford is narrowing its focus to more affordable EVs built on a new, shared platform. About $15.5 billion of these charges hit in the fourth quarter of 2025, with the rest spread over the coming periods. The company expects around $7 billion in special charges over the next two years tied to EV strategy changes and asset sales, with most of the cash impact likely in 2026.

And these charges related to EV reset aren’t unique to Ford. Several auto biggies, including General Motors GM and Stellantis STLA, are being forced to reassess their EV business as demand has slowed and costs have stayed high. Stellantis has taken the largest hit, writing down roughly $26 billion after scaling back its EV ambitions, including canceling plans for an all-electric Ram pickup. General Motors has also recorded sizable write-downs of about $7.6 billion as it delayed its EV rollout.

Operationally, Ford’s Model e segment remains in the red, though losses are narrowing. EBIT losses narrowed to $4.8 billion in 2025 from $5.07 billion in 2024. While the segment is expected to remain unprofitable through 2026 with a projected $4-$4.5 billion loss, Ford targets breakeven by 2029.

Management does expect some cost relief. Tariff headwinds are projected to ease to about $1 billion in 2026 as credits fully take effect. Additional savings from material and warranty cost reductions are also expected to help offset higher commodity prices and incremental investments.

The Novelis disruption will continue to weigh on results in 2026. While the company expects about $1 billion of year-over-year improvement, it will still absorb $1.5-$2 billion in temporary aluminum sourcing costs, which will fade next year. Ford expects EBIT to normalize progressively through 2026, with a more stable run rate in the second half as volumes and portfolio mix improve.

Ford expects adjusted EBIT of $8-$10 billion, up from $6.8 billion last year, with adjusted free cash flow improving to $5-$6 billion from $3.5 billion. Strength in Ford Pro and the traditional ICE/hybrid business is anticipated to offset ongoing Model e losses. Ford Pro pre-tax earnings are seen at $6.5-$7.5 billion, compared with $6.8 billion in 2025. EBIT from Ford Blue unit is projected to be $4-$4.5 billion (up from $3 billion in 2025), helped by Novelis recovery and a favorable pickup-led product mix.

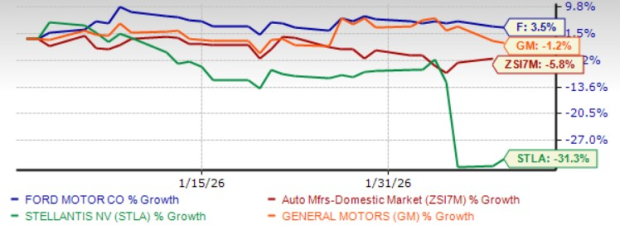

Year to date, shares of Ford have gained 3%, outperforming the industry as well as peers like General Motors and Stellantis.

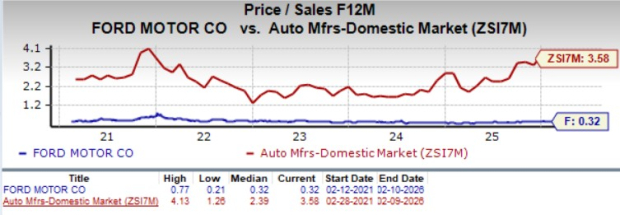

Valuation-wise, F appears undervalued now. The company is trading at a forward sales multiple of 0.32, way lower than the industry.

Despite the ugly fourth-quarter and near-term noise, Ford’s long-term case remains intact. The company generated $187 billion in revenues for the full year, marking its fifth straight year of top-line growth. U.S. market share climbed to 13.2%, its best showing in six years, helped by a strong dealer network and a smarter product mix. Hybrids and off-road models posted record sales.

Ford Pro remains the crown jewel. The commercial and fleet business continues to deliver double-digit EBIT margins, supported by strong global demand for the Super Duty and Transit franchises. Management acknowledged that Pro’s 2026 results will face temporary pressure from the Novelis impact, the Oakville plant ramp to expand Super Duty capacity in Canada, and tougher European regulations. Still, these are short-term hurdles rather than structural issues.

On EVs, Ford is clearly shifting gears. Instead of chasing volume at any cost, the company is focusing on affordable EVs built on a cost-efficient, universal platform, targeting lower-price models where EV demand in the United States has held up better and profitability is more achievable.

Beyond vehicles, Ford is building higher-margin growth engines. Paid software subscriptions rose 30% in 2025, with software and physical services profits expected to grow around 6.5%. Ford Energy is another strategic lever, with a $1.5 billion planned investment in 2026 and a goal of reaching 20 GWh of battery storage capacity by 2027. Partnerships with CATL and Renault further strengthen scale and cost advantages.

Finally, Ford’s balance sheet provides comfort. With nearly $50 billion in total liquidity, including $29 billion in cash, the company has the financial flexibility to navigate near-term bumps while investing for long-term returns.

Ford currently sports a Zacks Rank #1 (Strong Buy). The Zacks Consensus Estimate implies a 35% growth in Ford’s 2026 EPS.You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 26 min | |

| 36 min |

Trump imposes 50% tariffs on Canada: Markets are accustomed to 'heavy hand' tactic

GM

Yahoo Finance Video

|

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 4 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite