|

|

|

|

|||||

|

|

|

Novo Nordisk NVO announced better-than-expected fourth-quarter and full-year results last week. The company is a dominant player in the cardiometabolic space, marketing its blockbuster semaglutide-based (GLP-1) drugs — Ozempic (for type II diabetes [T2D]) and Wegovy (for obesity). These therapies are NVO’s key growth drivers, generating DKK 206.2 billion in 2025, including DKK 53.7 billion in the fourth quarter. Despite 15% growth over the combined sales figure of these two drugs in 2024, sales momentum for both drugs has slowed in the past year.

The declining growth trajectory of Novo Nordisk in 2025 was mostly fueled by intensifying competition from Eli Lilly LLY, widespread compounded semaglutide use in the United States, along with other macroeconomic factors such as pricing pressure in the country and foreign exchange headwinds.

Novo Nordisk secured the long-awaited FDA approval for its oral Wegovy pill to treat obesity and reduce cardiovascular risk in late December, followed by its commercial launch in early January. This marked a major milestone, making Wegovy the first GLP-1 RA available in an oral form for weight management. Compared to injectable formulations, the pill offers a far more convenient administration option.

Investors had viewed this development as the beginning of a potential turnaround for Novo Nordisk, with prospects of stronger Wegovy sales, regained share from Lilly and easing pressure from compounded semaglutide alternatives in the United States amid intensified legal action by NVO and an FDA crackdown. However, the company’s weaker-than-expected 2026 guidance has tempered those expectations and eroded investor optimism, prompting a sharp sell-off in the stock.

Although headline sales and operating profit will benefit from a one-off $4.2 billion reversal of U.S. 340B rebate provisions, management excluded this gain from its new non-IFRS adjusted metrics, exposing a much weaker underlying outlook. On an adjusted basis, the company expects sales and operating profit to decline 5-13% at CER in 2026, with further FX headwinds in DKK terms. Even on a reported basis, guidance implies roughly flat sales and only modest operating profit growth, highlighting the limited core momentum once non-recurring benefits are stripped out.

Growth in International Operations, driven by broader GLP-1 adoption and Wegovy roll-outs, is expected to be offset by rising competition, pricing pressure and semaglutide exclusivity losses. In the United States, slowing prescriptions, reduced Medicaid obesity coverage and lower realized prices under access initiatives and the MFN agreement weigh on expectations. At the same time, stepped-up R&D and commercial spending — including pipeline investments and acquisition-related costs — are set to pressure margins, with no repeat of favorable gross-to-net adjustments from 2025, underscoring the challenging earnings outlook.

Taken together, the near-term setup for Novo Nordisk remains catastrophic, warranting caution until clearer evidence of a re-acceleration emerges.

Eli Lilly is Novo Nordisk’s fierce competitor in the diabetes/obesity space, which markets its tirzepatide-based drugs, Mounjaro (T2D) and Zepbound (obesity). Despite being on the market for just over three years, Mounjaro and Zepbound have become LLY’s key top-line drivers. Last week, LLY reported fourth-quarter and full-year results, beating earnings and revenue estimates. In 2025, Mounjaro and Zepbound generated combined sales of $36.5 billion, comprising around 56% of the company’s total revenues. Along with its earnings results, Lilly also announced a bullish outlook for 2026. Lilly is also preparing to enter the oral obesity treatment market with its oral GLP-1 candidate, orforglipron. The company’s regulatory application seeking its approval is currently under FDA review, with a potential launch anticipated later this year.

The obesity space has garnered much of the spotlight over the past year due to the sizeable and still underpenetrated market opportunity. Smaller biotech firms, like Viking Therapeutics VKTX, are also advancing GLP-1-based therapies to challenge the incumbents. Viking Therapeutics is developing VK2735, both as oral and subcutaneous formulations, for the treatment of obesity. Last year, VKTX started two late-stage studies evaluating the subcutaneous formulation of VK2735. While one of these studies completed enrolment in November 2025 at a rapid pace, Viking Therapeutics expects to complete enrolment in the other study later in 2026.

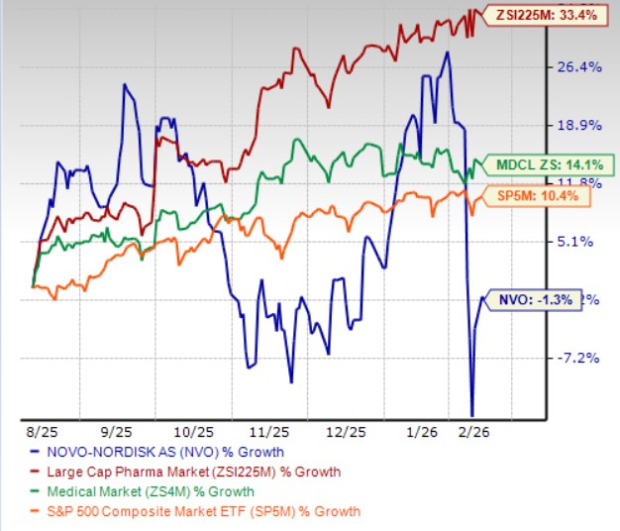

In the past six months, Novo Nordisk shares have lost 1.3% against the industry’s 33.4% growth. The company has also underperformed the sector and the S&P 500 during the same time frame, as seen in the chart below.

Novo Nordisk is trading at a discount to the industry, as seen in the chart below. Going by the price/earnings ratio, the company’s shares currently trade at 14.75 forward earnings, which is lower than 18.65 for the industry. The stock is trading much below its five-year mean of 29.25.

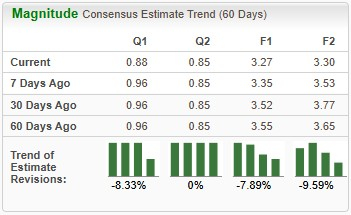

Earnings estimates for 2026 have declined from $3.55 to $3.27 per share over the past 60 days. During the same time frame, Novo Nordisk’s 2027 earnings estimates have declined from $3.65 to $3.30.

Novo Nordisk currently carries a Zacks Rank #5 (Strong Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 7 hours | |

| 12 hours | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite