|

|

|

|

|||||

|

|

|

The Coca-Cola Company KO reached a new 52-week high of $80.41 yesterday before dropping to close trading at $79.0, underscoring renewed investor confidence in the stock. This surge was largely driven by the company’s strong fourth-quarter 2025 performance reported on Tuesday, which reinforced Coca-Cola’s solid earnings momentum, disciplined pricing execution and enduring appeal as a defensive, all-weather investment amid an uncertain macroeconomic backdrop.

In fourth-quarter 2025, Coca-Cola continued to deliver resilient performance, supported by steady organic revenue growth, disciplined pricing and ongoing margin expansion despite persistent currency headwinds. Management emphasized broad-based execution across markets, with innovation and brand strength playing a central role. Core franchises such as Trademark Coca-Cola and Coca-Cola Zero Sugar maintained strong momentum, while brands like fairlife, Powerade, BODYARMOR and premium hydration offerings contributed meaningfully to growth.

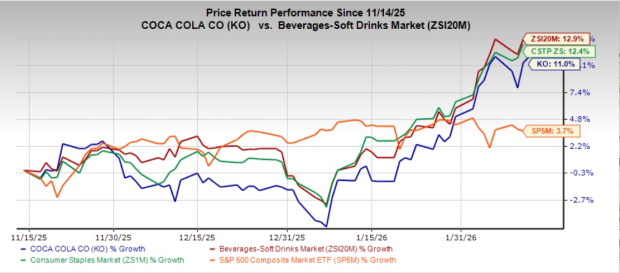

KO shares have advanced steadily in the past six months, supported by consistent revenue growth across operating segments, disciplined cost management and sustained investments behind its powerful brand portfolio. In the past six months, KO shares have rallied 11% compared with the broader industry’s 12.9% rise, the Zacks Consumer Staples sector’s 12.4% growth and the S&P 500 index’s 3.7% jump.

Following the recent momentum, KO has also outpaced several key peers, including PepsiCo Inc. PEP, Primo Brands Corporation PRMB and Keurig Dr Pepper Inc. KDP. Coca-Cola's performance is notably stronger than that of its closest competitor, PepsiCo, which recorded growth of 12.5% in the past six months. During the same time period, KO also outperformed Keurig Dr Pepper and Monster Beverage’s decline of 13.6% and 23%, respectively.

Coca-Cola is trading above its 50-day and 200-day moving averages, indicating a bullish sentiment. SMA is an essential tool in technical analysis that helps investors evaluate price trends by smoothing out short-term fluctuations. This approach also provides a clearer perspective on a stock's long-term direction.

Coca-Cola’s fourth-quarter 2025 performance was underpinned by solid organic revenue growth, driven by a healthy balance of pricing actions and improving volume trends. Strategic price increases, coupled with effective revenue growth management, enabled the company to offset inflationary pressures without materially dampening demand. Notably, volume trends improved sequentially in the quarter, signaling strengthening consumer traction across key markets.

Margin expansion was another critical contributor to fourth-quarter earnings strength. Comparable gross and operating margins improved year over year, supported by ongoing productivity initiatives, supply-chain efficiencies and disciplined marketing investments. These gains helped drive a 6% increase in comparable earnings per share despite persistent currency headwinds and a higher effective tax rate, highlighting Coca-Cola’s operational resilience.

Coca-Cola’s diversified geographic footprint and broad beverage portfolio also played a pivotal role. Strength in North America and Latin America helped offset softer conditions in parts of Asia-Pacific, while continued value-share gains across regions reinforced the effectiveness of Coca-Cola’s all-weather strategy. Innovation and brand activation, including zero-sugar offerings and localized product launches, further supported revenue momentum.

The company’s strong cash flow generation and balance sheet flexibility enhanced investor confidence. Robust free cash flow conversion enabled Coca-Cola to continue investing in growth, sustain its long-standing dividend growth streak and maintain prudent leverage. Together, these factors position Coca-Cola to navigate near-term macro uncertainty while sustaining long-term earnings and shareholder value growth.

Coca-Cola’s 2026 outlook reflects confidence in its all-weather strategy and disciplined execution across markets. Management expects 4-5% organic revenue growth in 2026, supported by resilient demand, pricing and revenue management. Comparable net revenues should see a 1% currency tailwind, partially offset by a 4% impact from acquisitions and divestitures.

Profitability is set to rise, with comparable currency-neutral EPS up 5-6% and reported EPS up 7-8%, aided by a 3% currency tailwind. Adjusted free cash flow is projected at $12.2 billion, supported by $14.4 billion in cash from operations and $2.2 billion in capital expenditures.

The Zacks Consensus Estimate for Coca-Cola’s 2026 and 2027 EPS has increased by a penny each in the past 30 days. For 2026, the Zacks Consensus Estimate for KO’s revenues and EPS implies 5.4% and 7.7% year-over-year growth, respectively. The consensus mark for 2027 revenues and earnings suggests 4.7% and 7.3% year-over-year growth, respectively.

KO’s current forward 12-month price-to-earnings (P/E) multiple of 24.24X is higher than the Zacks Beverages – Soft Drinks industry average of 20.15X, making the stock appear relatively expensive. Also, the company’s P/E is significantly higher than the S&P 500’s multiple of 22.90X.

At 24.24X P/E, Coca-Cola trades at a significant premium to its industry peers like PepsiCo, Keurig Dr Pepper and Primo Brands, which trade at more reasonable multiples. PepsiCo, Keurig Dr Pepper and Primo Brands have forward 12-month P/E ratios of 19.29X, 13.67X and 14.49X — all significantly lower than that of KO.

Despite its strong global footprint and brand power, Coca-Cola faces several near-term challenges that could temper its momentum. One key concern is slowing volume growth in mature markets, particularly North America and Western Europe, where consumer demand remains pressured by inflation and ongoing shifts toward healthier beverages. While Coca-Cola has relied heavily on pricing to drive revenue growth, sustained price increases risk elasticity pressures over time, potentially weighing on volumes as consumers become more value-conscious.

Coca-Cola remains exposed to volatile input costs, including sweeteners, aluminum and PET resin, as well as higher marketing and distribution expenses needed to defend market share. Additionally, currency fluctuations continue to be a swing factor given the company’s significant international exposure, which can dilute reported results even when underlying performance is solid.

Coca-Cola has hit a significant milestone, with its stock reaching new highs, driven by its robust market position, diverse product lineup and focus on innovation and digital initiatives. These strengths support the company’s potential for steady, long-term growth. However, KO faces near-term risks, including inflationary pressures, economic uncertainty in key markets, tariff-related challenges and currency fluctuations.

Even with these challenges, Coca-Cola remains an attractive option for long-term investors, supported by strong profitability and a growing global presence. Its proactive approach to managing economic volatility will be key to sustaining momentum.

For new investors, evaluating the stock’s current valuation is important given its recent rally. Existing shareholders may find it sensible to retain this Zacks Rank #3 (Hold) stock, considering its resilience and long-term growth prospects. You can see the complete list of today's Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-20 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite