|

|

|

|

|||||

|

|

|

MercadoLibre’s MELI valuation may be a concern for some investors. The stock is trading at a premium compared to the broader Zacks Internet – Commerce industry. As of the latest data, MELI’s forward 12-month Price/Sales ratio hovers around 3.9, above the industry’s 2.08, reflecting investors' high growth expectations.

With MELI stock trading at a premium, investors may be wondering how to approach it. While the company faces short-term pressures, such as macroeconomic uncertainties and increased competition, it also experiences strong long-term growth drivers across all its segments. Let’s take a closer look at the key factors influencing the company to help determine the best course of action.

As e-commerce gains traction worldwide, the growing number of entrants into the space is intensifying competition for MELI. Currently, the company faces competition from e-commerce giants Amazon AMZN and Alibaba BABA, and from the retail behemoth Walmart WMT. Amazon is making strong efforts to expand its presence in Latin America, while Walmart has established itself as the biggest retailer in the region, with more than 3,000 stores just in Mexico. Alibaba’s AliExpress offers products at a low cost to consumers in the same region.

Although MercadoLibre has a very strong foothold in the online retail market of Latin America, competition from larger companies with a global presence poses a significant threat to its market share and growth trajectory. These entrants bring vast resources, advanced technology, and established supply chains. If MELI fails to implement effective counter strategies, it could face increasing pressure on both margins and user retention in the long term.

MercadoLibre operates across 18 Latin American countries, exposing it to significant foreign exchange risk. Revenues earned in local currencies must be converted into U.S. dollars for SEC reporting, making the company vulnerable to currency fluctuations. Appreciation of the dollar or instability in regional currencies could impact the company’s financial results.

Additionally, macroeconomic headwinds in key markets like Brazil and Argentina are forcing MELI to proceed with caution, particularly in its fintech segment. Rising interest rates in Brazil have led the company to scale back riskier credit products, while Argentina’s history of policy shifts and inflationary pressure has led the company to maintain shorter loan durations. MELI’s fintech expansion strategy remains highly sensitive to economic swings and currency volatility, making steady growth difficult to maintain in such unstable markets.

The Zacks Consensus Estimate for first-quarter 2025 earnings is pegged at $7.67 per share, which has been revised upward by 1.9% over the past seven days, indicating 13.13% year-over-year growth.

The consensus mark for first-quarter 2025 revenues is pegged at $5.53 billion, suggesting 27.54% year-over-year growth.

MercadoLibre’s earnings beat the Zacks Consensus Estimate in three of the trailing four quarters and missed once, with the average surprise being 16.37%.

See the Zacks Earnings Calendar to stay ahead of market-making news.

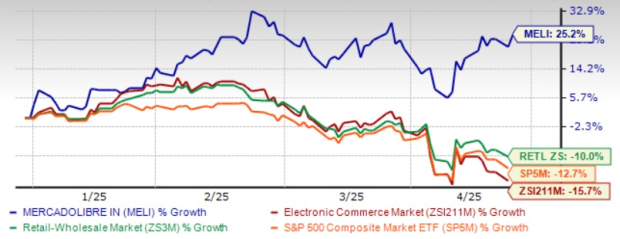

MercadoLibre shares have gained 25.2% in the year-to-date period, outperforming the Zacks Retail-Wholesale sector and the S&P 500 index’s decline of 10% and 12.7%, respectively. The stock has also outperformed the Zacks Internet – Commerce industry’s decline of 15.7% in the same time frame. Shares of its competitors Alibaba and Walmart have gained 36.9% and 5%, respectively, while Amazon has lost 21.1%.

MELI shares have been riding on its dominant presence in Latin America and a diversified business model across e-commerce, logistics and fintech. Operating in 18 countries, it continues to invest heavily in expansion. The company has plans to increase its investments in Mexico this year by 38%, and in Brazil by 48%. As of Dec. 31, 2024, cash and cash equivalents were $2.63 billion. Short-term investments were $1.05 billion as of Dec. 31, 2024. The strong liquidity position helps the company expand and pursue strategic initiatives.

MercadoLibre’s e-commerce platform grew strongly in 2024, reaching more than 100 million unique buyers. The company improved user experience with features like virtual try-ons and tire installation scheduling. It also launched Full Super, a new grocery section designed to make shopping easier, help users reorder quickly, and show progress toward free shipping to boost basket sizes.

Logistics upgrades supported this growth. New fulfillment centers and better delivery routes increased productivity, while keeping costs low even as shipments rose 29% year over year. Advertising also improved, which led to revenues as a share of gross market value to rise by 50 basis points. MELI’s move toward more display and video ads is expected to increase ad revenues over time.

MercadoLibre’s fintech arm, Mercado Pago, surpassed 60 million monthly active users in 2024, supported by the launch of 5.9 million new credit cards. Instant access to pre-approved credit and flexible 18-month instalment plans helped drive adoption and boosted engagement during high-value purchases.

The company expanded its offerings with the MELI Dollar stablecoin and localized investment options like LCI and LCA. Attractive deposit returns in Brazil, Mexico, Argentina and Chile further increased user engagement. MELI also grew its merchant lending through open finance tools, strengthening loyalty and positioning Mercado Pago as a leading digital financial platform in the region.

Current valuations of MELI suggest that investors should hold the stock for now. While the company’s dominant market position in Latin America remains a key strength, rising competition and macroeconomic uncertainties pose risks to its long-term prospects.

The company’s margins are under pressure from increased investments in free shipping, loyalty programs and fraud prevention efforts. Additionally, seasonal fluctuations, especially a typically weaker first quarter following a strong fourth quarter, may temporarily impact performance. Despite these pressures, MELI’s growing user ecosystem presents a strong foundation for sustained growth. MELI currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 5 min | |

| 20 min | |

| 21 min | |

| 34 min | |

| 42 min |

MercadoLibre Stock Climbs After Posting Mixed Q4 Results, Strong E-Commerce Growth

MELI

Investor's Business Daily

|

| 43 min |

MercadoLibre Stock Climbs After Posting Mixed Q4 Results, Strong E-Commerce Growth

AMZN

Investor's Business Daily

|

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 4 hours |

Anthropic Shows Olive Branch At Enterprise Event. Software Stocks Gain.

AMZN

Investor's Business Daily

|

| 4 hours | |

| 4 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite