|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

Philip Morris International Inc.’s PM shares rallied almost 3.5% in the pre-market session today after reporting robust first-quarter 2025 results. Both top and bottom lines increased year over year and beat the respective Zacks Consensus Estimate. Results were fueled by robust momentum across regions and product categories, including continued momentum in IQOS and ZYN, along with a stable combustibles performance. The company raised its 2025 adjusted earnings per share (EPS) guidance.

First-quarter adjusted EPS came in at $1.69, which increased 12.7% year over year. Excluding currency effects, the adjusted EPS jumped 17.3%. The bottom line beat the Zacks Consensus Estimate of $1.61. (Find the latest EPS estimates and surprises on Zacks Earnings Calendar.)

Net revenues of $9,301 million increased 5.8% on a reported basis and 10.2% on an organic basis. Revenues came ahead of the Zacks Consensus Estimate of $8,946.3 million. The increase in organic revenues was backed by positive pricing variance (mainly driven by elevated combustible tobacco pricing) and favorable volume/mix (attributable to increased smoke-free product volumes), despite a less favorable cigarette mix.

Philip Morris International Inc. price-consensus-eps-surprise-chart | Philip Morris International Inc. Quote

During the first quarter, Philip Morris’ net revenues from combustible products remained flat year over year and increased 3.8% organically. Combustible products delivered volume growth and strong pricing gains, which were partially offset by an unfavorable geographic mix.

Revenues from the smoke-free business increased 15% (up 20.4% on an organic basis) and formed 42% of the company’s total revenues. Within the smoke-free business, inhalable smoke-free products (SFP) were driven by strength in IQOS, while oral SFP was fueled by increased shipment volumes of ZYN.

Total shipment volumes (including heated tobacco units, oral SFP and cigarettes) increased 3.9% to 187.8 billion units in the first quarter.

The adjusted operating income ascended 12.8% (up 16% on an organic basis) to $3,790 million, driven by improved pricing variance and a positive volume/mix, somewhat negated by increased marketing, administration and research costs.

Following the sale of Vectura Group Ltd. on Dec. 31, 2024, the company revised its segment reporting to integrate ongoing Wellness and Healthcare results into the Europe segment. Its first-quarter 2025 financial results reflect this updated segment structure.

Net revenues in the European region grew 3% (up 8.6%) on an organic basis to $3,560 million. This was a result of positive pricing variance and favorable volume/mix. Total HTU and cigarette shipment volumes in the region were almost flat at 48.4 billion units.

In the SSEA, CIS & MEA regions, net revenues increased 3.2% (up 6.5% organically) to $2,743 million on improved pricing variance and favorable volume. Total cigarette and HTU shipment volume in the region rose 4.6% to 90.2 billion units.

In the EA, AU & PMI GTR regions, net revenues grew 2.8% (up 6.5% organically) to $1,731 million on favorable volume/mix. Total shipment volumes in the region rose 5.9% to 28.8 billion units.

Revenues in the Americas rose 27.2% (up 32% on an organic basis) to $1,267 million. This was a result of the positive volume/mix and pricing. Total cigarette and HTU shipment volumes in the Americas remained unchanged at 14.4 billion units.

The company ended the quarter with cash and cash equivalents of $4,443 million, long-term debt of $38,781 million and a total shareholder deficit of $8,926 million.

Philip Morris announced its quarterly dividend of $1.35 per share ($5.40 per share on an annualized basis). However, the company stated that it would not make share repurchases in 2025.

Adjusted EPS for 2025 is now envisioned in the $7.36-$7.49 range, suggesting 12-14% growth. Earlier, the metric was expected in the $7.04-$7.17 range, suggesting 7.2-9.1% growth. Adjusted EPS, excluding currency, is likely to be in the $7.26-$7.39 band, indicating a year-over-year increase of 10.5-12.5%. For full-year 2025, PM expects reported EPS in the band of $7.01-$7.14 compared with the $4.52 reported in 2024.

The total international industry volume for cigarettes and HTUs (excluding China and the United States) is likely to decline nearly 1% in 2025. The total cigarette and smoke-free product shipment volume for Philip Morris is likely to rise up to 2%, driven by a smoke-free product volume increase of 12-14%.

Nicotine pouch shipment volumes in the United States are expected to be between 800 and 840 million cans for 2025, projecting 38-45% growth.

For 2025, PM expects net revenues to increase 6-8% on an organic basis. The operating income on an organic basis is likely to rise 10.5-12.5%.

Management expects an operating cash flow of more than $11 billion in 2025. Capital expenditures are likely to be nearly $1.5 billion, including additional investments in ZYN.

For the second quarter of 2025, Philip Morris envisions adjusted EPS in the range of $1.80-$1.85, including a projected favorable currency impact of 6 cents.

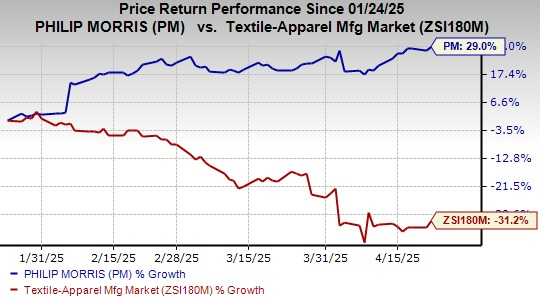

Shares of this Zacks Rank #2 (Buy) company have gained 29% in the past three months against the industry’s decline of 31.2%.

United Natural Foods, Inc. UNFI distributes natural, organic, specialty, produce and conventional grocery and non-food products in the United States and Canada. At present, United Natural carries a Zacks Rank of 2. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The consensus estimate for United Natural’s current financial-year sales and earnings implies growth of 1.9% and 485.7%, respectively, from the year-ago figures. UNFI delivered a trailing four-quarter earnings surprise of 408.7%, on average.

Utz Brands UTZ engages in the manufacture, marketing and distribution of snack foods in the United States and presently carries a Zacks Rank of 2. UTZ delivered a trailing four-quarter earnings surprise of 8.8%, on average.

The Zacks Consensus Estimate for Utz Brands’ current financial-year sales and earnings indicates growth of 1.4% and 10.4%, respectively, from the year-ago numbers.

BRF S.A. BRFS raises, produces and slaughters poultry and pork for the processing, production and sale of fresh meat, processed products, pasta, margarine, pet food and other products. It currently carries a Zacks Rank of 2. BRFS delivered a trailing four-quarter earnings surprise of 9.6%, on average.

The Zacks Consensus Estimate for BRF S.A.'s current fiscal-year sales indicates growth of 0.3% from the prior-year levels.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-20 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-16 | |

| Feb-16 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-13 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite