|

|

|

|

|||||

|

|

|

Bank of America BAC is widening the funnel on relationship-based rewards with BofA Rewards, a no-fee loyalty program set to launch on May 27, for any client with a personal checking account. Hence, more than 30 million existing customers who were previously outside the bank’s Preferred Rewards umbrella will become newly eligible, an expansion that effectively turns basic checking into a gateway for deeper, higher-value engagement.

By tying membership to checking, BAC encourages customers to centralize bill pay, debit spending and direct deposit, behaviors that typically translate into stickier, lower-cost deposits. Over time, that funding stability can support net interest income (NII) by improving deposit retention and mix. Hence, loyalty benefits are likely to shift customers from “single-product” users to “primary bank” households.

The program also aims to drive fee-based revenue. Clients can earn 10% to 75% credit card rewards bonuses on eligible cards, a lever that can increase card adoption and everyday spend, driving interchange income and, for revolvers, higher NII. As tiering is based on a three-month average balance across qualifying Bank of America and Merrill accounts, this is expected to nudge customers to consolidate assets, an important tailwind for Merrill net new assets and long-term wealth fees.

Further, BAC Rewards includes discounts on home and auto loans and access to cash-back deals from more than 15,000 brands, incentives designed to pull more borrowing and purchase activity onto the bank’s rails. If successful, the expanded loyalty base will compound relationship value through higher product-per-household, better retention and a broader pool for cross-sell. This will support revenue growth across interest, fee and payments lines.

The two closest peers of BAC are JPMorgan JPM and Citigroup C.

JPMorgan is widening cross-sell by pairing scale with tighter “relationship” hooks. The bank is adding 160 Chase branches this year to capture more primary deposits, then using omnichannel bankers and data-driven offers to steer customers into cards, mortgages and wealth. JPMorgan’s relationship-pricing mortgage discounts reward balances and are expected to lift fee income and NII.

Citigroup is widening cross-sell by combining its U.S. retail bank with wealth, aligning Citigold and mass-market clients in one pipeline. Citigroup is also uplifting U.S. consumer cards as a core unit, helping bankers bundle deposits, cards, lending and advice through a centralized client organization across digital channels.

Shares of Bank of America have risen 10.3% over the past six months.

From a valuation standpoint, Bank of America trades at a 12-month trailing price-to-tangible book (P/TB) of 1.93X, below the industry.

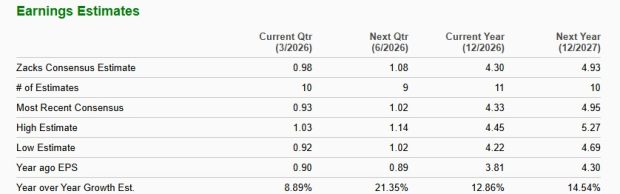

The Zacks Consensus Estimate for Bank of America’s 2026 and 2027 earnings suggests year-over-year growth of 12.9% and 14.5%, respectively. In the past week, earnings estimates for 2026 and 2027 have been revised lower.

Bank of America currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 3 hours | |

| 10 hours | |

| Jul-04 | |

| Jul-04 | |

| Jul-04 | |

| Jul-04 | |

| Jul-04 | |

| Jul-03 | |

| Jul-03 | |

| Jul-03 | |

| Jul-03 | |

| Jul-03 | |

| Jul-03 | |

| Jul-03 | |

| Jul-02 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite