|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

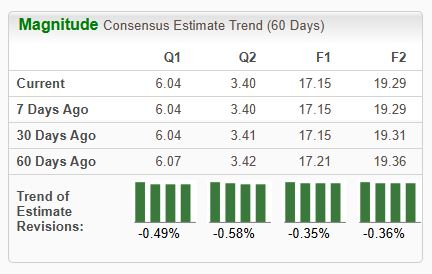

Leading insurer Aon PLC AON is set to report its first-quarter 2025 results on April 25, before the opening bell. The Zacks Consensus Estimate for the to-be-reported quarter’s earnings is currently pegged at $6.04 per share on revenues of $4.86 billion. (See the Zacks Earnings Calendar to stay ahead of market-making news.)

The first-quarter earnings estimate has been constant over the past week. The bottom-line projection indicates a year-over-year increase of 6.7%. Moreover, the Zacks Consensus Estimate for quarterly revenues suggestsyear-over-year growth of 19.3%.

For the current year, the Zacks Consensus Estimate for Aon’s revenues is pegged at $17.29 billion, implyinggrowth of 10.2% year over year. Also, the consensus mark for current-year EPS is pegged at $17.15, calling for a jump of around 9.9% on a year-over-year basis.

AON beat the consensus estimate for earnings in two of the last four quarters and missed twice, with the average surprise being 1.7%.

Aon plc price-eps-surprise | Aon plc Quote

Our proven model does not conclusively predictanearnings beat for the company this time. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat, which is not the case here. You can see the complete list of today’s Zacks #1 Rank stocks here.

AON has an Earnings ESP of -1.24% and a Zacks Rank #3. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Aon's revenue growth in the first quarter is expected to have been supported by Health Solutions and Reinsurance Solutions. The Zacks Consensus Estimate forHealth Solutions stands at $1.04 billion, suggestinga 42.4% year-over-year increase, while our estimate is pegged at $1 billion.

The Zacks Consensus Estimate for Reinsurance Solutions is pegged at $1.23billion, marking a 5.7% year-over-year increase, while our estimate stands at around $1.24 billion. The consensus mark for Commercial Risk Solutions’ revenues is pegged at $2.1 billion, up from $1.8 billion a year ago.

Also, the consensus estimate for Wealth Solutions’ revenues is pegged at $500 million, up from $370 million a year ago.

The factors mentioned above are expected to have contributed to the company's year-over-year growth. However, the upsides are likely to have been partially offset by higher costs.

Our model suggests that the total operating expensesin the first quarter may rise 24.8%, attributed to increased costs related to higher compensation and benefits and information technology.

Here are some companies worth considering from the broader Finance space, as our model shows that these have the right combination of elements to beat on earnings this time:

Palomar Holdings Inc. PLMR has an Earnings ESP of +1.57% and is a Zacks #2 Ranked player.

The Zacks Consensus Estimate for Palomar Holdings’ bottom line for the to-be-reported quarter is pegged at $1.59 per share, indicating 45.9% year-over-year growth. It has remained stable over the past week. The consensus estimate for Palomar Holdings’ revenues is pegged at $171.76 million.

Arthur J. Gallagher & Co. AJG has an Earnings ESP of +0.53% and is a Zacks #3 Ranked player.

The Zacks Consensus Estimate forArthur J. Gallagher & Co.’s bottom line for the to-be-reported quarter is pegged at $3.57 per share, indicating 2.3% year-over-year growth. Arthur J. Gallagher & Co.beat earnings estimates in each of the past four quarters, with the average surprise being 2.3%. The consensus estimate for AJG’s revenues is pegged at $3.75 billion.

Brown & Brown, Inc. BRO has an Earnings ESP of +0.77% and is a Zacks #3 Ranked player.

The Zacks Consensus Estimate for Brown & Brown’s bottom line for the to-be-reported quarter is pegged at $1.30 per share, indicating 14% year-over-year growth. It has remained stable over the past week. The consensus estimate for Brown & Brown’s revenues is pegged at $1.4 billion.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-20 | |

| Feb-19 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 |

Aon appoints Nick Fraccalvieri to lead global facultative reinsurance unit

AON

Life Insurance International

|

| Feb-16 | |

| Feb-16 | |

| Feb-14 | |

| Feb-13 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite