|

|

|

|

|||||

|

|

|

What a brutal six months it’s been for C3.ai. The stock has dropped 41% and now trades at $9.21, rattling many shareholders. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Is there a buying opportunity in C3.ai, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.

Despite the more favorable entry price, we're swiping left on C3.ai for now. Here are three reasons you should be careful with AI and a stock we'd rather own.

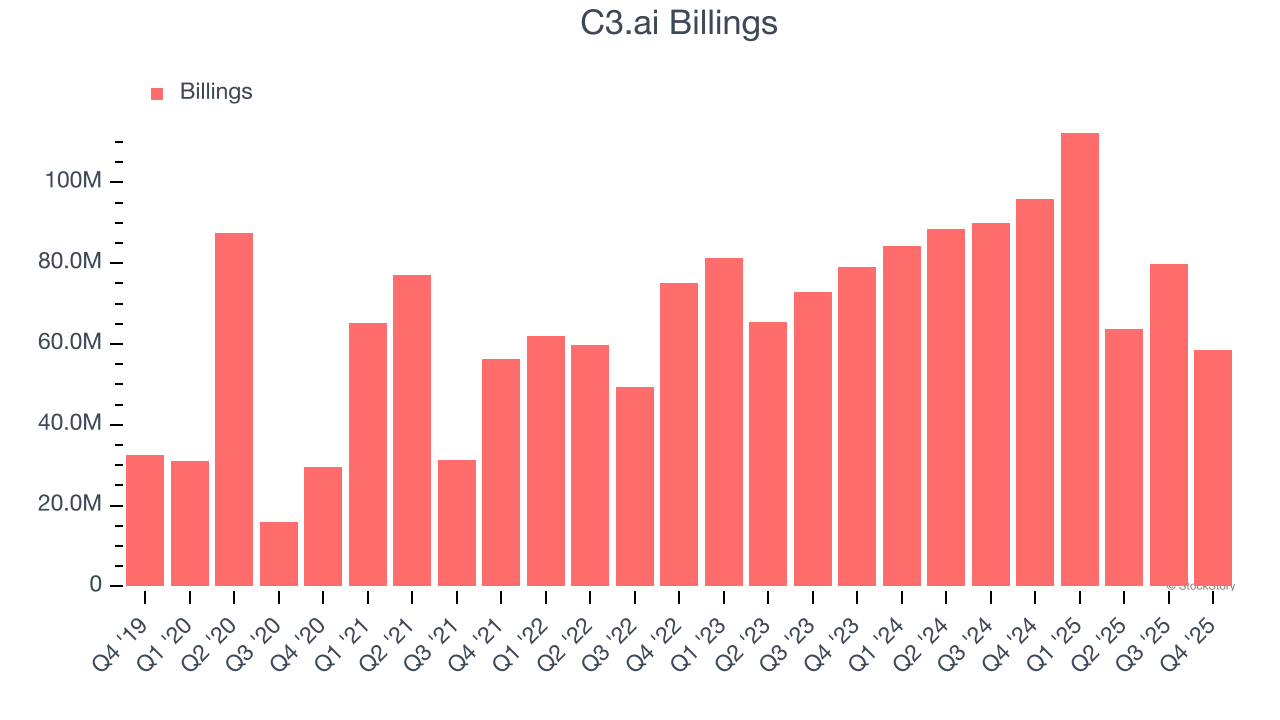

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

C3.ai’s billings came in at $58.57 million in Q4, and it averaged 11.2% year-on-year declines over the last four quarters. This performance was underwhelming and shows the company faced challenges in acquiring and retaining customers. It also suggests there may be increasing competition or market saturation.

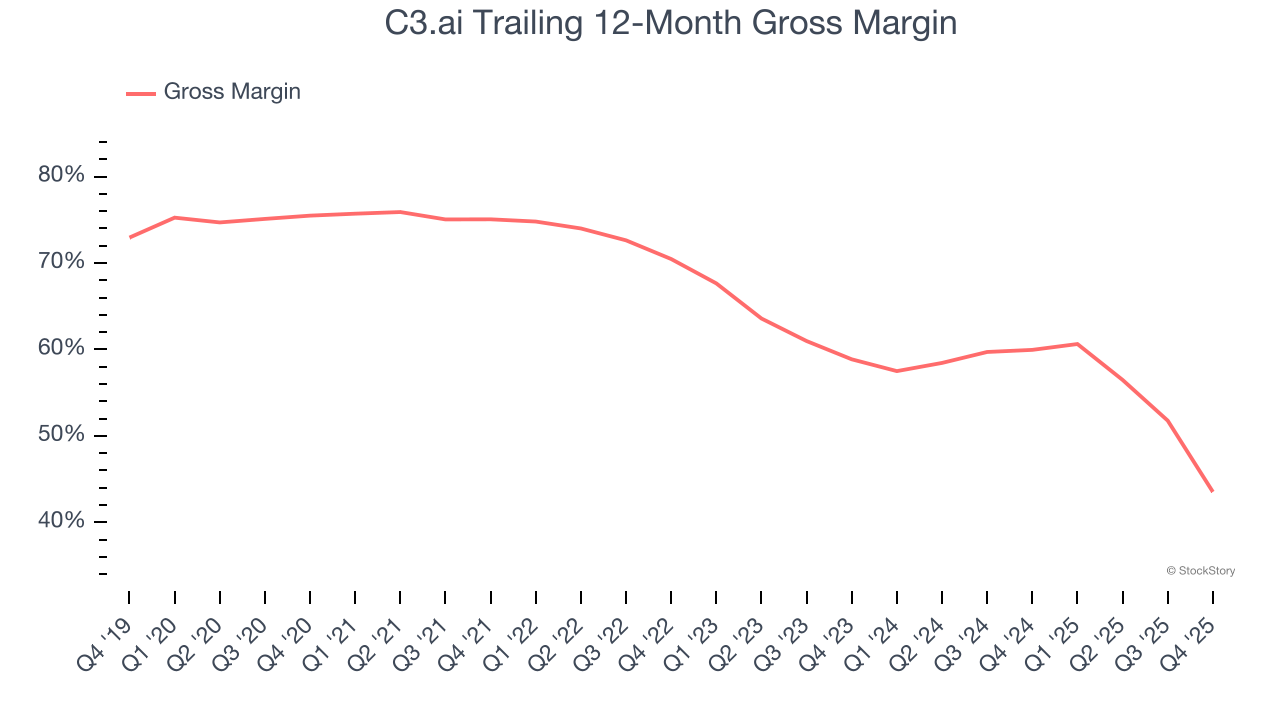

For software companies like C3.ai, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

C3.ai’s gross margin is substantially worse than most software businesses, signaling it has relatively high infrastructure costs compared to asset-lite businesses like ServiceNow. As you can see below, it averaged a 43.5% gross margin over the last year. Said differently, C3.ai had to pay a chunky $56.48 to its service providers for every $100 in revenue.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. C3.ai has seen gross margins decline by 15.3 percentage points over the last 2 year, which is among the worst in the software space.

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Over the next year, analysts predict C3.ai’s cash burn will increase. Their consensus estimates imply its free cash flow margin of negative 41.3% for the last 12 months will fall to negative 50.2%.

C3.ai doesn’t pass our quality test. Following the recent decline, the stock trades at 6.2× forward price-to-sales (or $9.21 per share). At this valuation, there’s a lot of good news priced in - we think there are better opportunities elsewhere. Let us point you toward a fast-growing restaurant franchise with an A+ ranch dressing sauce.

ONE MORE THING: Top 6 Stocks for This Week. This market is separating quality stocks from expensive ones fast. AI taking down whole sectors with no warning. In a rotation this fast, you need more than a list of good companies.

Our AI system flagged Palantir before it ran 1,662%. AppLovin before it ran 753%. Nvidia before it ran 1,178%. Each week it produces 6 new names that pass the same tests. Get Our Top 6 Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

| Aug-04 | |

| Jun-23 | |

| Jun-22 | |

| Jun-08 | |

| Jun-08 | |

| Jun-04 | |

| Jun-04 | |

| Jun-04 | |

| Jun-04 | |

| Jun-04 | |

| Jun-03 | |

| Jun-03 | |

| Jun-03 | |

| Jun-03 | |

| Jun-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite