|

|

|

|

|||||

|

|

|

Shares of 3M Company MMM have gained 8.9% since it reported first-quarter 2025 results on April 22. The company recorded year-over-year growth for both earnings and revenues (on an adjusted basis) in the quarter, with the latter falling short of the Zacks Consensus Estimate.

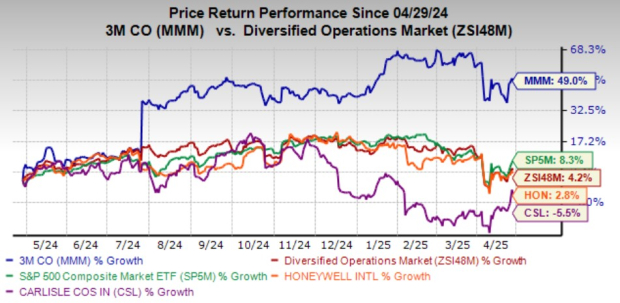

Nevertheless, 3M’s shares have surged 49% over the past year compared with the Zacks Diversified Operations industry and the S&P 500’s growth of 4.2% and 8.3%, respectively. The company has also outperformed other industry players like and Honeywell International Inc. HON and Carlisle Companies Incorporated CSL, which have gained 2.8% and declined 5.5%, respectively, over the same time frame.

Let us delve deeper into 3M’s first-quarter results and long-term prospects before assessing whether to buy, hold or sell the stock.

In the first quarter, adjusted revenues improved 1.5% year over year to $5.78 billion but narrowly missed the consensus estimate of $5.79 billion. However, its adjusted earnings of $1.88 per share surpassed the consensus estimate of $1.77 and increased 10% year over year. The year-over-year increase was primarily driven by strength across the electrical, aerospace, advanced materials and industrial adhesives & tapes markets.

In the quarter, revenues from the electrical, industrial adhesives and tapes markets grew in the high-single-digit range, while the same from roofing granules, industrial specialties and personal safety markets increased in the low-single-digit range. Also, revenues from the aerospace market increased in low-double-digit, and the same from the advanced materials market grew in high-single-digit.

3M has been witnessing strong momentum in the Safety and Industrial segment, driven by strength in the electrical, industrial adhesives and roofing granules markets. Significant orders for power cable accessories in the United States, driven by an increase in demand from data centers, augur well for the segment in the quarters ahead. However, soft demand in the auto aftermarket and abrasives markets remains a concern. The segment’s organic sales improved approximately 2.5% year over year in the first quarter of 2025.

The company’s Transportation and Electronics segment has been benefiting from strength in the transportation and aerospace end markets. Solid electronics demand, backed by an increase in production volume by electronics original equipment manufacturer (OEM) customers, is proving beneficial for the segment. However, weakness in the automotive electrification market, due to a decline in automotive OEM build rates, remains a concern.

The segment’s adjusted organic revenues grew 1.1% in the first quarter of 2025. Backed by strength across its businesses, the company provided a positive outlook. For 2025, it continues to expect total adjusted organic sales to grow 2-3% on a year-over-year basis.

The company also remains focused on increasing shareholders’ wealth through dividend payments and share buybacks. In the first quarter of 2025, it paid dividends worth $396 million and repurchased shares for $1.27 billion. In February 2025, MMM’s board also approved a share buyback program, authorizing it to repurchase up to $7.5 billion of common stock. In 2025, it anticipates a gross share repurchase of around $2 billion. Also, in February 2025, the company hiked its quarterly dividend by 4.3%.

Persistent weakness in the consumer retail end markets has been hurting the Consumer segment’s results, which declined 1.4% in the first quarter. There was a particular weakness in the command and packaging & expression businesses. The company expects consumer retail discretionary spending on hardline goods to remain muted for 2025, which is likely to hurt its overall performance.

Exiting the first quarter, 3M’s long-term debt was high at $12.3 billion, up 10.8% sequentially. Also, interest expenses in the quarter remained high at $255 million. Exiting the first quarter, its short-term borrowings and current portion of long-term debt totaled $1.2 billion. It’s worth noting that 3M’s long-term debt-to-capital ratio is currently 73.1%, much higher than the industry’s 55.1%. High debt levels, if not controlled, can increase financial obligations and prove detrimental to profitability in the quarters ahead.

The company has been subject to several litigations, including earplug lawsuits. It has committed substantial funds to resolve these disputes as ongoing litigation might lead to additional expenses.

MMM also operates in the highly competitive electronics, transportation, aerospace, defense and other markets, comprising well-recognised providers of highly engineered products. As one of its peers, Honeywell serves as a global diversified technology and manufacturing company, with a wide range of products and services. Carlisle, another peer, engages in the manufacture of a wide range of roofing and waterproofing products, engineered products and finishing equipment.

The Zacks Consensus Estimate for 3M’s 2025 earnings has decreased 1.8% to $7.66 per share over the past 30 days, indicating year-over-year growth of 4.9%. The consensus mark for second-quarter 2025 earnings decreased 1.5% to $2.01 per share, indicating a year-over-year increase of 4.2%. (Find the latest EPS estimates and surprises on Zacks Earnings Calendar.)

3M is trading at a forward 12-month price-to-earnings (P/E) ratio of 17.49X, higher than the industry average of 15.38X. This elevated valuation could make the stock vulnerable to further pullbacks if market sentiment sours. In comparison with MMM’s valuation, Honeywell and Carlisle are trading at 18.87X and 16.18X.

Despite its several upsides and solid share price returns, the near-term challenges, such as weakness in the retail market, high debt level and premium valuation, are limiting this Zacks Rank #3 (Hold) company’s prospects. While current shareholders should hold their positions, new investors should wait for the stock to retract some of its recent gains and provide a better entry point.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 5 hours | |

| 6 hours | |

| 6 hours | |

| 11 hours | |

| 12 hours | |

| 14 hours |

Johnson Matthey Lowers Price of Unit Being Sold to Honeywell to $1.8 Billion

HON

The Wall Street Journal

|

| 14 hours | |

| 15 hours | |

| Feb-21 | |

| Feb-20 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite