|

|

|

|

|||||

|

|

|

AT&T Inc. T and Verizon Communications Inc. VZ are major players in the telecommunications industry. Operating as one the largest wireless service provider in North America, AT&T offers a vast array of communication and business solutions that include wireless, local exchange, long-distance, data/broadband and Internet, video, managed networking, wholesale and cloud-based services.

Verizon, the leading wireless carrier in the United States, delivers communication services to a vast customer base across the public sector, small, medium businesses and global enterprises as well. With the acquisition of Alltel Wireless Corp. the company has surpassed AT&T Inc. as the largest wireless carrier in the North America.

With deep industry expertise, both AT&T and Verizon are strategically positioned in the highly competitive U.S. telecommunications landscape. Let us analyze in depth the competitive strength and weaknesses of the companies to understand who is in better position to maximize gain from the emerging market trends.

Verizon is benefiting from significant 5G adoption and fixed wireless broadband momentum. The company is steadily expanding the availability of its 5G Ultra-Wideband network across the country. To drive growth in a highly competitive and saturated U.S. wireless market, Verizon is focusing on changing its revenue mix toward new growth areas like cloud, security, and professional services. The company formed a strategic partnership with Accenture to develop cutting-edge cybersecurity solutions for businesses across industries. It is collaborating with NVIDIA to power real-time Generative AI (artificial intelligence) applications over its 5G private network. The company recently launched Verizon Business Assistant to support small businesses in their customer interaction process.

The company is also initiating a customer-oriented strategy to gain a competitive edge. It recently introduced a three-year price lock guarantee for all its myPlan and myHome network plans. This ensures that the core monthly plan price for calling, data, and texting will not change in the next three-year period, excluding taxes, fees and perks. Verizon is aggressively forging ahead to expand its fiber network footprint with strategic acquisitions and innovation. With the buyout of Frontier Communication, Verizon is expected to gain a significant broadband customer base by 2026. Its dividend payout rate stands at 58%. A solid free cash flow growth combined with consistently high dividend payout rate underscores strong operational efficiency and a commitment to driving shareholders’ value. Its debt-to-capital ratio is 58.9% in 2024, down from 61.6% in 2023.

However, Verizon is facing intensifying competition from AT&T and T-Mobile US, Inc. TMUS. Growing spending on promotion and lucrative discount offers to beat the competition is weighing on margins. Its wireline business is also struggling owing to competitive pressure from voice-over-Internet protocol (VoIP) service providers and aggressive triple-play (voice, data and video) offerings by cable companies.

With a customer-centric business model, AT&T is witnessing healthy momentum in its postpaid wireless business with a lower churn rate and increased adoption of higher-tier unlimited plans. The company remains focused on improving mobile 5G, fixed wireless, and edge computing services to drive growth. AT&T is leveraging Ericsson technology to deploy a commercial-scale open radio access network (Open RAN) across the country to help build a more robust ecosystem of network infrastructure providers and suppliers. It is also collaborating with Nokia to streamline network services, improve automation, speed up deployment times, and improve operational efficiency.

AT&T has been taking several customer-oriented strategies to gain a competitive edge in the industry. It is working with TransUnion to improve customer experiences with branded calling services. AT&T is also collaborating with Microsoft to move its 5G mobile network to the latter’s cloud. The move will enable AT&T to enhance productivity and deliver large-scale network services to meet customers’ needs. The company recently introduced AT&T Guarantee, a first-of-its-kind industry initiative that promises to pay bill credits for any network outage across its wireless and fiber networks for consumers and small businesses. The company’s dividend payout rate stands at 50.1%. In 2024, its debt-to-capital ratio is 51.1%, which has declined steadily since 2022. The company’s strong emphasis on debt management and improving liquidity is an added advantage.

However, despite its effort to reinforce focus on the customer-centric business model with an aim to maintain its customer base, the nationwide wireless service outage that occurred last year has dented customer trust. Moreover, its effort to woo customers with healthy discounts, freebies and cash credits further escalates margin pressures. Stiff competition from Verizon and T-Mobile is a headwind. T-Mobile’s strong cash flow position and continuous deployment of mid-band 2.5 GHz spectrum are further intensifying the competition. Declining trends in the wireline business remain a concern.

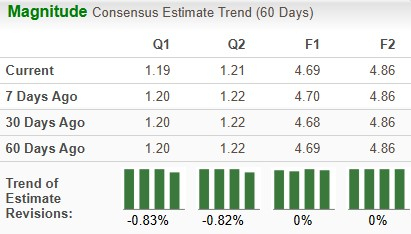

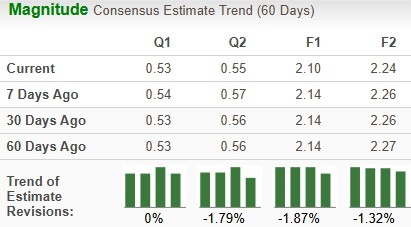

The Zacks Consensus Estimate for Verizon’s 2025 sales and EPS implies year-over-year growth of 1.68% and 2.18%, respectively. The EPS estimates have remained unchanged over the past 60 days.

The Zacks Consensus Estimate for AT&T’s 2025 sales indicates growth of 1.5% year over year, while EPS is projected to decline 7.08%. The EPS estimates have been trending southward over the past 60 days.

Over the past year, Verizon has gained 5% compared with the industry’s growth of 30.7%. T has gained 58.6% over the same period.

Verizon looks more attractive than AT&T from a valuation standpoint. Going by the price/earnings ratio, Verizon’s shares currently trade at 8.83 forward earnings, lower than 12.52 for AT&T.

Verizon and AT&T carry a Zacks Rank #3 (Hold) each. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Both companies expect modest revenue growth with improved cash flow in 2025. Verizon’s bigger customer base, strategic collaborations to expand its portfolio offerings, core network upgrades, fiber expansion and AI initiatives are major growth drivers. Solid subscriber momentum over the past few months, strong emphasis on debt management, and network modernizations are positives for AT&T. However, with an attractive valuation, greater dividend payout rate, stronger free cash flow growth and resilient business model, Verizon appears to be a better investment option at the moment.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite