|

|

|

|

|||||

|

|

|

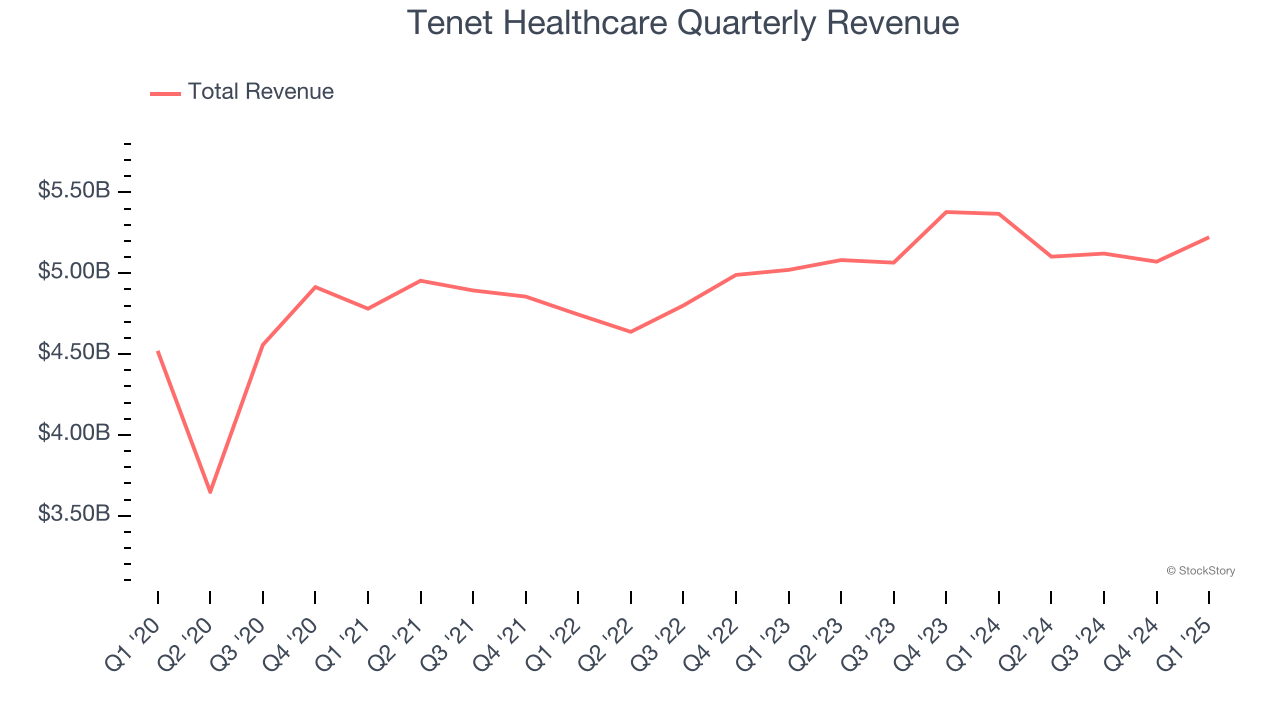

Hospital operator Tenet Healthcare (NYSE:THC) reported revenue ahead of Wall Street’s expectations in Q1 CY2025, but sales fell by 2.7% year on year to $5.22 billion. The company expects the full year’s revenue to be around $20.8 billion, close to analysts’ estimates. Its non-GAAP profit of $4.36 per share was 39.2% above analysts’ consensus estimates.

Is now the time to buy Tenet Healthcare? Find out by accessing our full research report, it’s free.

With a network spanning nine states and serving primarily urban and suburban communities, Tenet Healthcare (NYSE:THC) operates a nationwide network of hospitals, ambulatory surgery centers, and outpatient facilities providing acute care and specialty healthcare services.

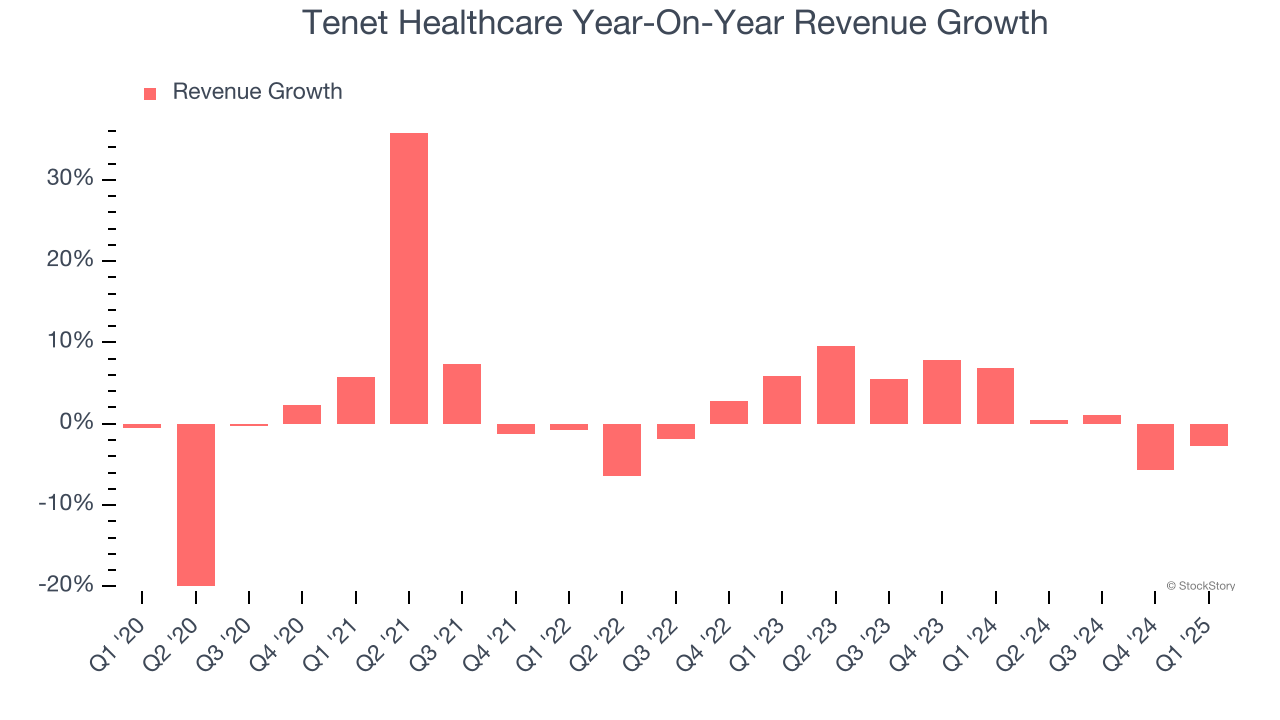

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Tenet Healthcare grew its sales at a tepid 2.1% compounded annual growth rate. This wasn’t a great result, but there are still things to like about Tenet Healthcare.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Tenet Healthcare’s annualized revenue growth of 2.7% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

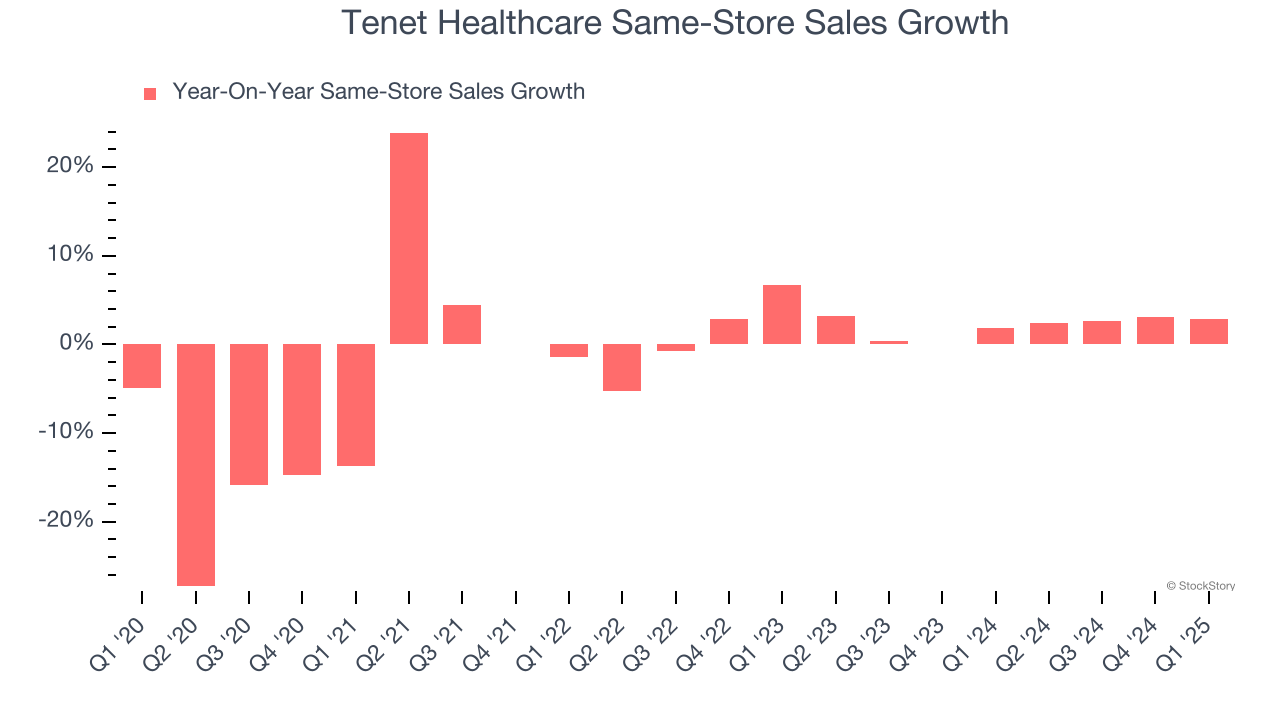

We can dig further into the company’s revenue dynamics by analyzing its same-store sales, which show how much revenue its established locations generate. Over the last two years, Tenet Healthcare’s same-store sales averaged 2.1% year-on-year growth. This number doesn’t surprise us as it’s in line with its revenue growth.

This quarter, Tenet Healthcare’s revenue fell by 2.7% year on year to $5.22 billion but beat Wall Street’s estimates by 1.3%.

Looking ahead, sell-side analysts expect revenue to grow 2.7% over the next 12 months, similar to its two-year rate. This projection is underwhelming and suggests its newer products and services will not lead to better top-line performance yet. At least the company is tracking well in other measures of financial health.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

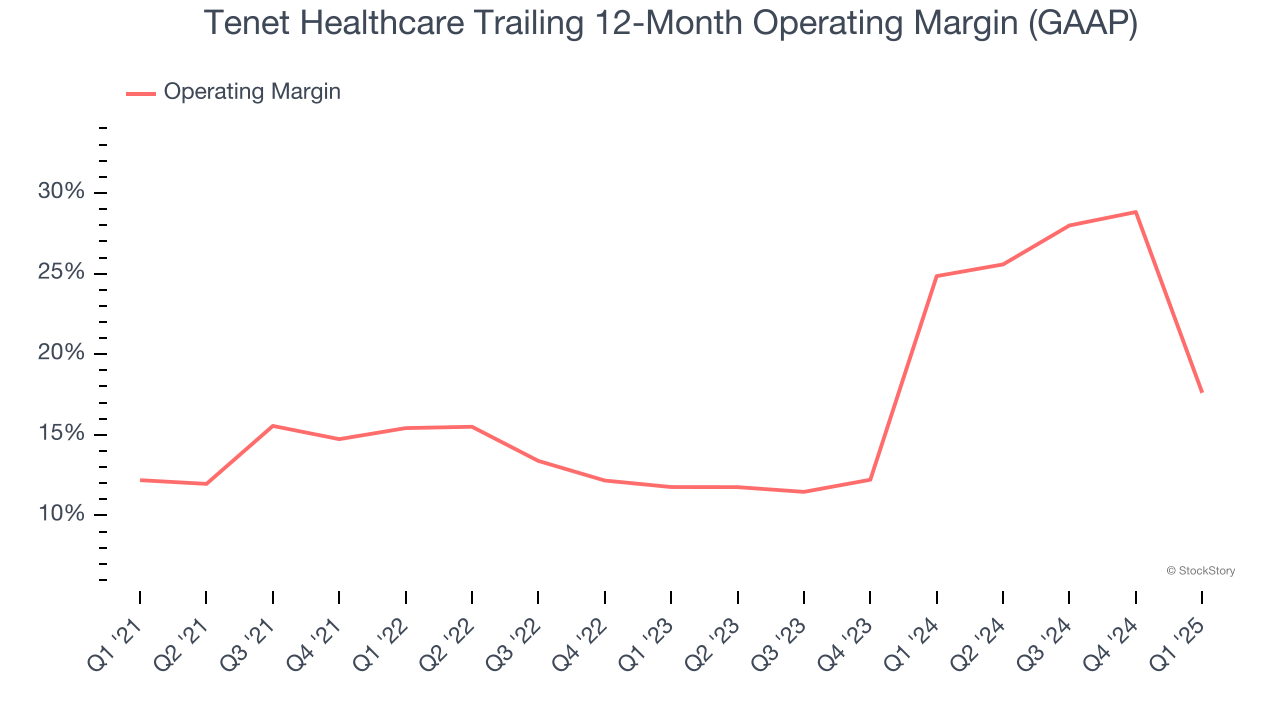

Tenet Healthcare has managed its cost base well over the last five years. It demonstrated solid profitability for a healthcare business, producing an average operating margin of 16.6%.

Analyzing the trend in its profitability, Tenet Healthcare’s operating margin rose by 5.4 percentage points over the last five years, as its sales growth gave it operating leverage. The company’s two-year trajectory shows its performance was mostly driven by its recent improvements.

This quarter, Tenet Healthcare generated an operating profit margin of 18.1%, down 43.1 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

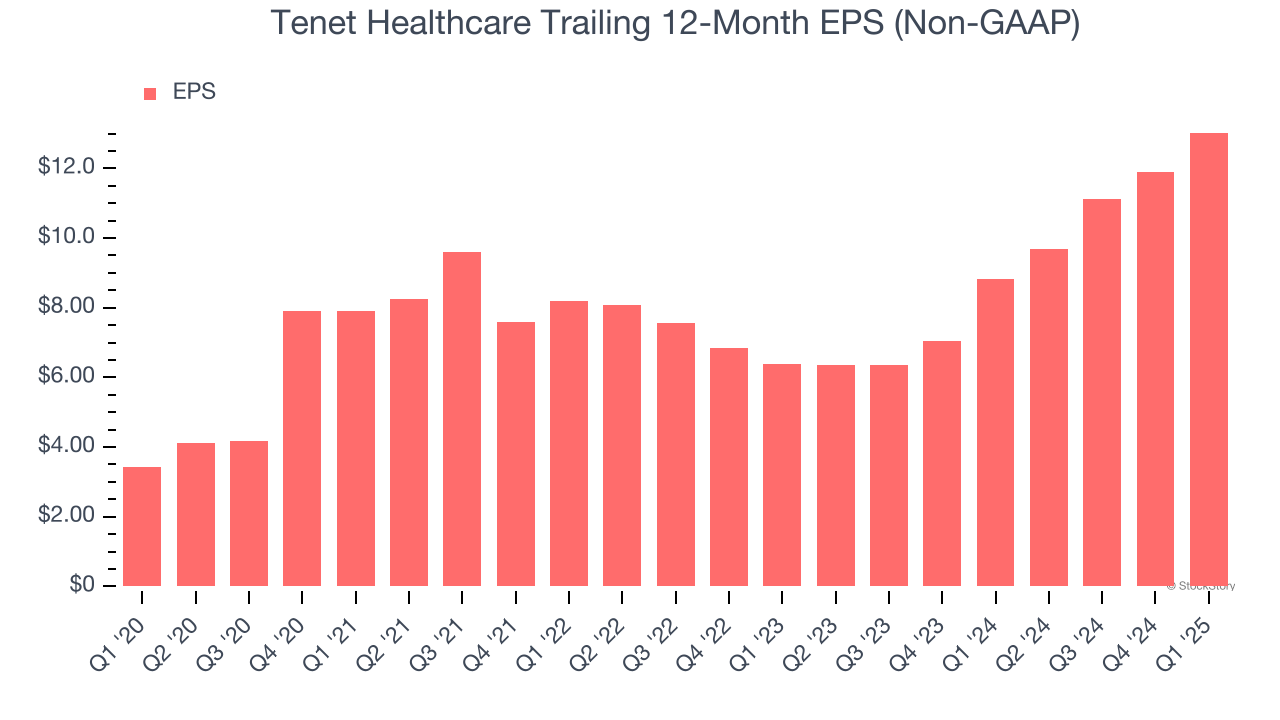

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Tenet Healthcare’s EPS grew at an astounding 30.7% compounded annual growth rate over the last five years, higher than its 2.1% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

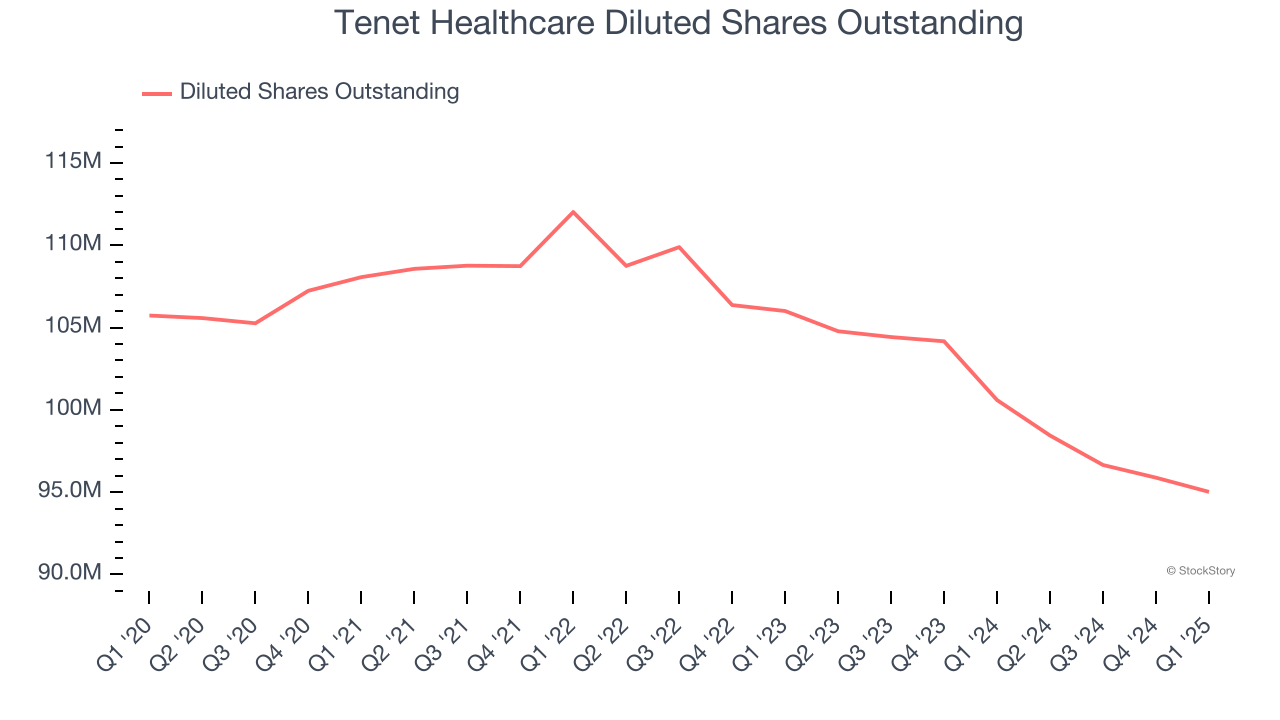

We can take a deeper look into Tenet Healthcare’s earnings quality to better understand the drivers of its performance. As we mentioned earlier, Tenet Healthcare’s operating margin declined this quarter but expanded by 5.4 percentage points over the last five years. Its share count also shrank by 10.1%, and these factors together are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

In Q1, Tenet Healthcare reported EPS at $4.36, up from $3.22 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Tenet Healthcare’s full-year EPS of $13.03 to shrink by 5.4%.

We were impressed by how significantly Tenet Healthcare blew past analysts’ EPS expectations this quarter on a solid revenue beat. We were also glad its full-year EPS guidance outperformed Wall Street’s estimates. On the other hand, its full-year revenue guidance was just in line. Overall, this quarter was still solid. The stock traded up 1.8% to $126.01 immediately after reporting.

Tenet Healthcare had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.

| Feb-26 | |

| Feb-26 | |

| Feb-25 | |

| Feb-24 | |

| Feb-24 | |

| Feb-20 | |

| Feb-20 | |

| Feb-19 | |

| Feb-19 | |

| Feb-18 | |

| Feb-13 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite