|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

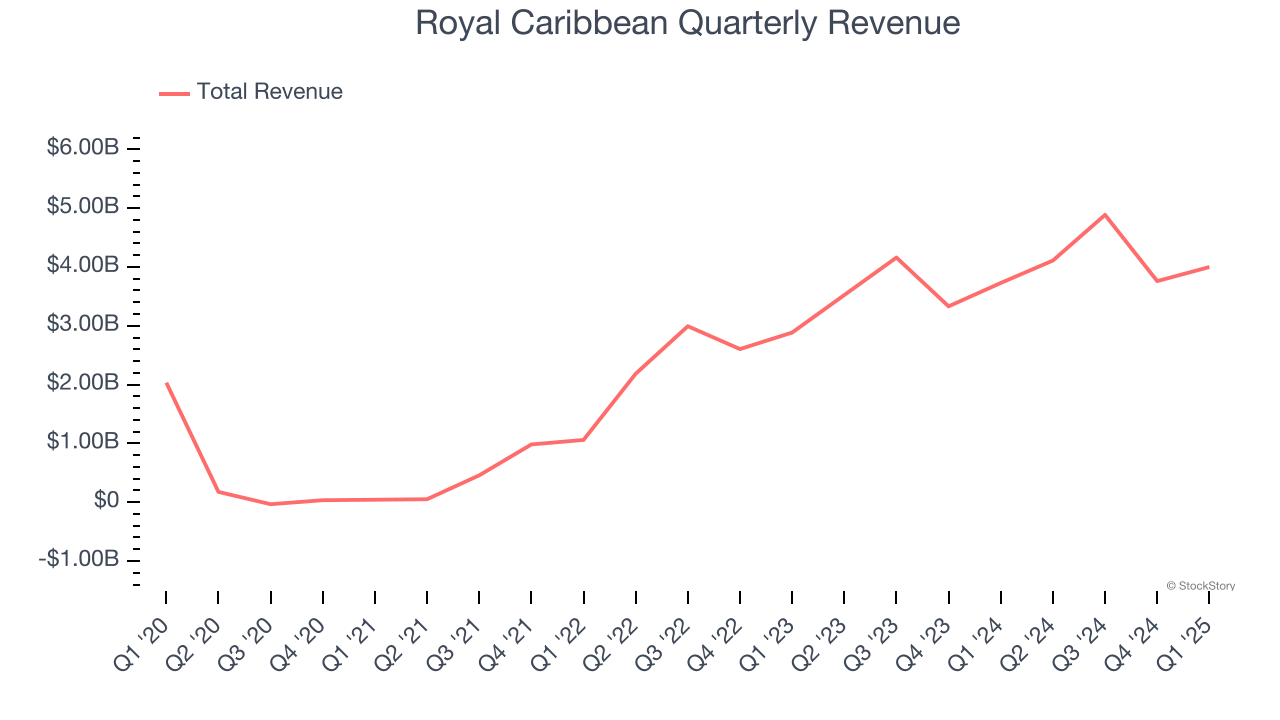

Cruise vacation company Royal Caribbean (NYSE:RCL) met Wall Street’s revenue expectations in Q1 CY2025, with sales up 7.3% year on year to $4.00 billion. Its non-GAAP profit of $2.71 per share was 7% above analysts’ consensus estimates.

Is now the time to buy Royal Caribbean? Find out by accessing our full research report, it’s free.

"Our strong first quarter results are a testament to the enduring appeal and attractive value proposition of our leading brands and the incredible vacations they deliver," said Jason Liberty, president and CEO, Royal Caribbean Group.

Established in 1968, Royal Caribbean Cruises (NYSE:RCL) is a global cruise vacation company renowned for its innovative and exciting cruise experiences.

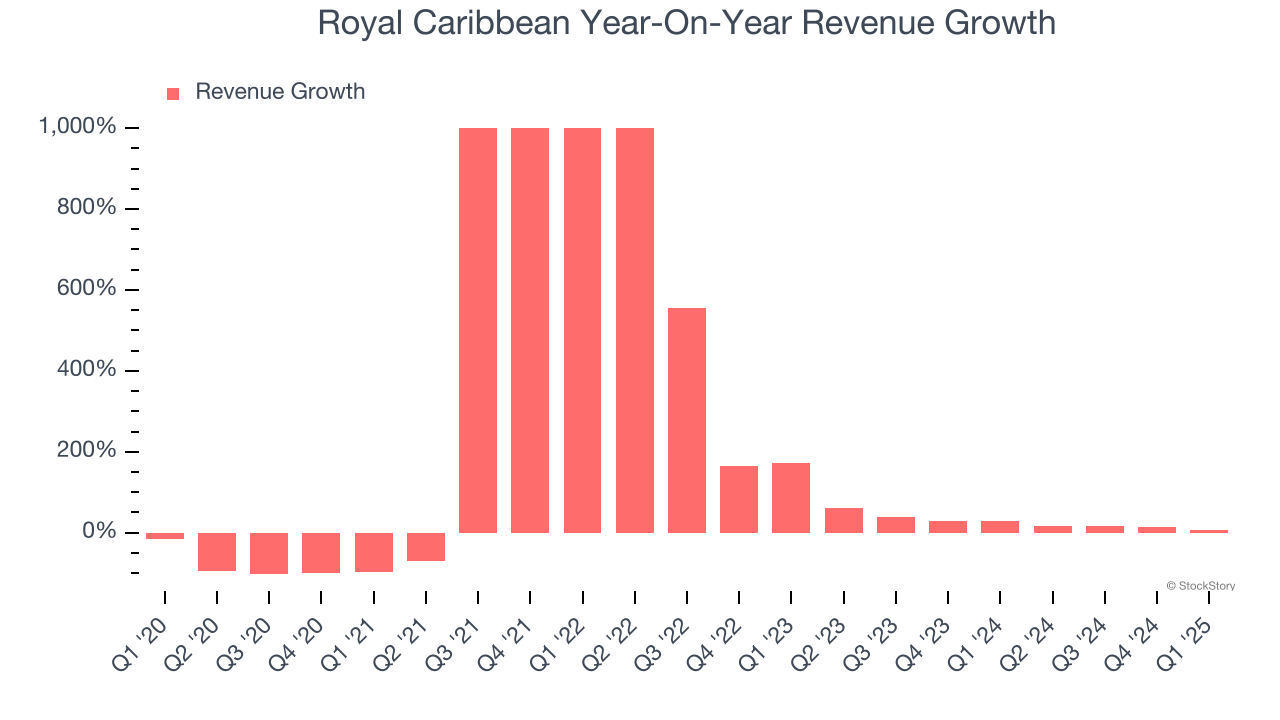

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Royal Caribbean grew its sales at a tepid 9.7% compounded annual growth rate. This was below our standard for the consumer discretionary sector and is a poor baseline for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new property or trend. Royal Caribbean’s annualized revenue growth of 25.3% over the last two years is above its five-year trend, suggesting its demand recently accelerated. Note that COVID hurt Royal Caribbean’s business in 2020 and part of 2021, and it bounced back in a big way thereafter.

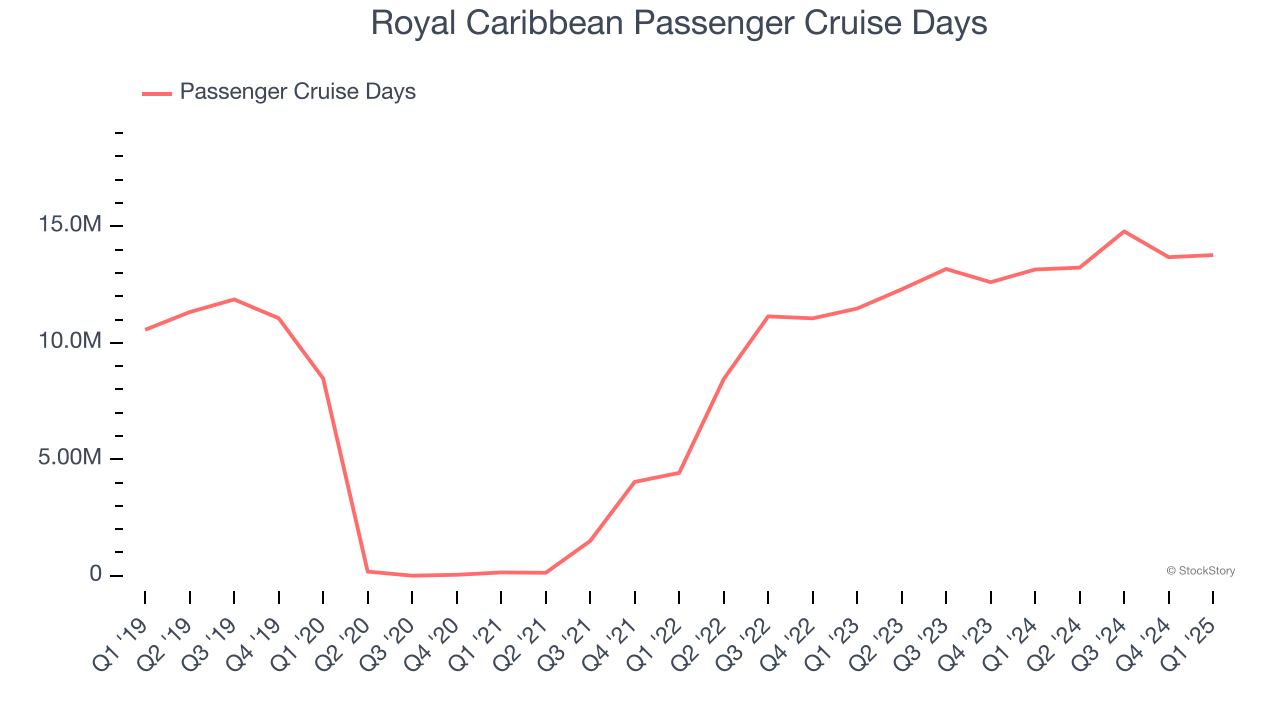

We can dig further into the company’s revenue dynamics by analyzing its number of passenger cruise days, which reached 13.77 million in the latest quarter. Over the last two years, Royal Caribbean’s passenger cruise days averaged 15.7% year-on-year growth. Because this number is lower than its revenue growth during the same period, we can see the company’s monetization has risen.

This quarter, Royal Caribbean grew its revenue by 7.3% year on year, and its $4.00 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 9.7% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and implies its products and services will face some demand challenges.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

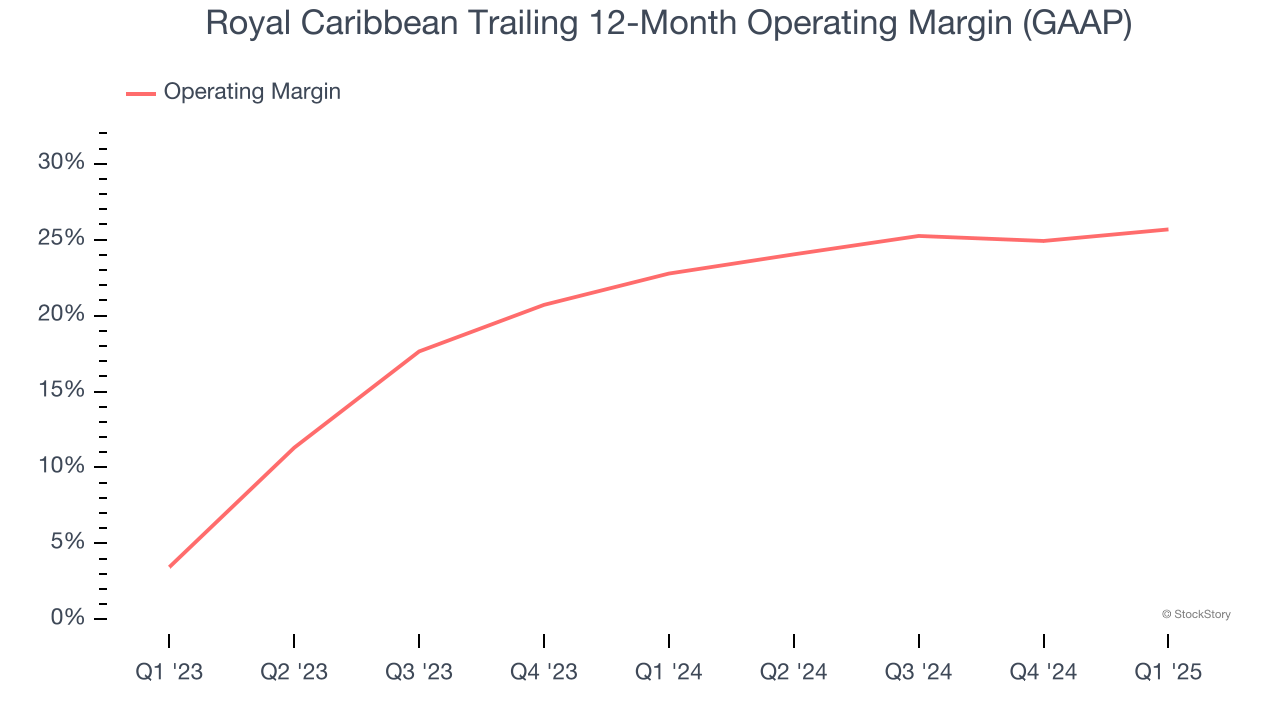

Royal Caribbean’s operating margin has been trending up over the last 12 months and averaged 24.3% over the last two years. On top of that, its profitability was elite for a consumer discretionary business thanks to its efficient cost structure and economies of scale.

This quarter, Royal Caribbean generated an operating profit margin of 23.6%, up 3.5 percentage points year on year. This increase was a welcome development and shows it was more efficient.

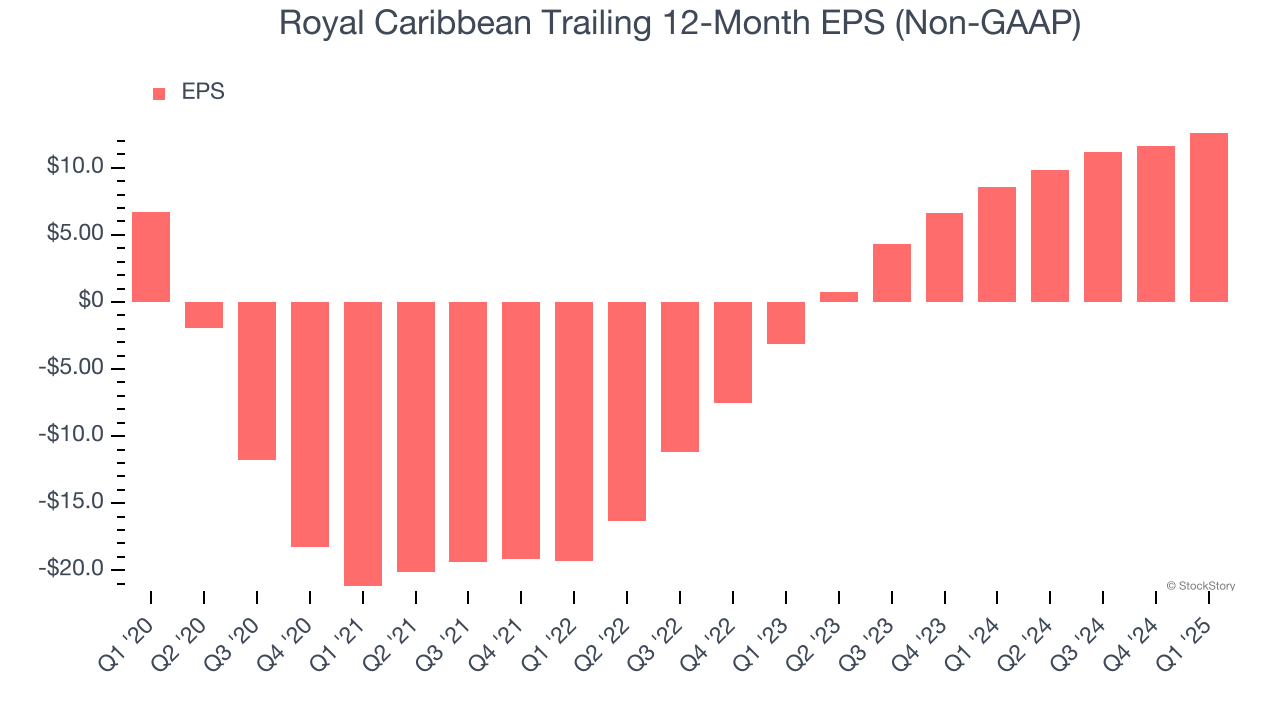

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Royal Caribbean’s EPS grew at a solid 13.4% compounded annual growth rate over the last five years, higher than its 9.7% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

In Q1, Royal Caribbean reported EPS at $2.71, up from $1.70 in the same quarter last year. This print beat analysts’ estimates by 7%. Over the next 12 months, Wall Street expects Royal Caribbean’s full-year EPS of $12.63 to grow 21.4%.

It was encouraging to see Royal Caribbean beat analysts’ EPS expectations this quarter. We were also happy its EBITDA outperformed Wall Street’s estimates. On the other hand, its revenue was in line. Overall, this quarter had some key positives, and this is important given the choppy macro backdrop and news of lower and middle-income consumer pulling back discretionary spend. The stock traded up 1.4% to $220.18 immediately after reporting.

Big picture, is Royal Caribbean a buy here and now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free.

| Feb-22 | |

| Feb-21 | |

| Feb-20 | |

| Feb-20 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite