|

|

|

|

|||||

|

|

|

Energy Transfer LP ET units appear to be relatively undervalued compared to the Zacks Oil and Gas Production Pipeline – MLB industry. The company's current trailing 12-month Enterprise Value to EBITDA (EV/EBITDA) ratio stands at 10.25X, which is below the industry average of 11.67X. This suggests that ET is currently trading at a discount relative to its peers.

Energy Transfer owns a wide network of pipelines across the United States and is pursuing opportunities to serve growing power loads from new demand centers across its network.

Another firm operating in this space, Plains All American Pipeline PAA, is also trading at an EV/EBITDA of 9.2X, at a discount compared to its industry.

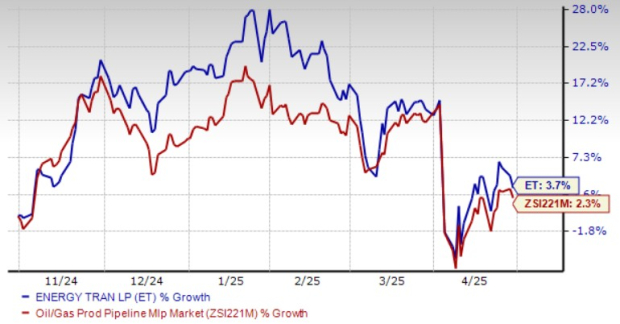

The ET stock has underperformed its industry in the past six-month period.

Should you consider adding ET to your portfolio only based on discounted valuation and current softness in prices? Let’s delve deeper and find out the factors that can help investors decide whether it is a good entry point to add ET stock to their portfolio.

Energy Transfer LP operates an extensive pipeline network exceeding 130,000 miles across the United States, with operations spanning 44 states. The company continues to expand its footprint through a combination of organic growth initiatives and strategic acquisitions. Since 2021, ET has consistently executed one major accretive acquisition annually, including the purchase of WTG last year, which enhanced its natural gas pipeline and processing infrastructure in the Permian Basin.

Nearly 90% of Energy Transfer’s revenues are generated through fee-based contracts related to transportation and storage services. These long-term agreements with a strong and reliable customer base ensure stable cash flows and significantly mitigate the company’s exposure to fluctuations in commodity prices. As oil and gas production continues to rise across the United States, ET is well-positioned to benefit from the growing demand for pipeline transportation infrastructure.

Energy Transfer also possesses significant export capabilities, with natural gas liquids (NGL) and crude oil export capacities surpassing 1.1 million and 1.9 million barrels per day, respectively. The company is actively enhancing its export infrastructure through ongoing expansion projects at its Marcus Hook and Nederland terminals. Notably, ET commands an estimated 20% share of the global NGL export market, underscoring its strong position in international energy trade.

Energy Transfer’s asset base is strategically distributed across key U.S. production basins and high-demand regions, providing strong earnings support. This diversified portfolio includes a balanced mix of oil and gas pipelines, gathering and processing facilities, and storage assets, enabling the company to efficiently serve a broad range of markets.

Energy Transfer’s current quarterly cash distribution rate is 32.75 cents per Energy Transfer common unit. ET’s management has raised distribution rates 14 times in the past five years, and the current payout ratio is 101%.

ET’s management and insiders own a sizeable chunk of its units. Management members and independent board members continue to purchase units of the firm. Energy Transfer insiders bought more than 44 million units worth $468 million from January 2021 to February 2025. The increasing ownership of insiders indicates bright prospects and sustainable growth amid rising demand in the midstream space.

Insider ownership in the ET stock is nearly 10%, which is more than its peers in the same industry. The increasing ownership of insiders indicates bright prospects and sustainable growth amid the rising demand in the midstream space.

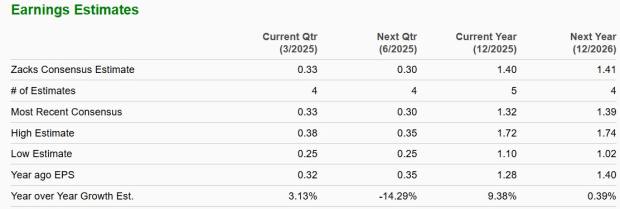

The Zacks Consensus Estimate for Energy Transfer’s 2025 and 2026 earnings per unit indicates year-over-year growth of 9.38% and 0.39%, respectively.

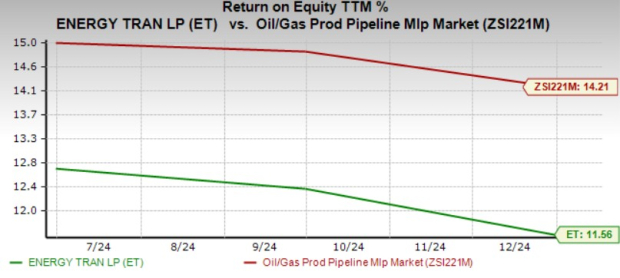

Energy Transfer’s trailing 12-month return on equity is 11.56%, lower than the industry average of 14.21%. Return on equity, a profitability measure, reflects how effectively a company utilizes its shareholders’ funds to generate income.

With a vast network of over 130,000 miles of pipelines and related infrastructure spanning 44 states, Energy Transfer is well-positioned to capitalize on the rising production of oil, natural gas, and natural gas liquids across the United States.

Energy Transfer’s ROE is lower than the industry average. Those who have this Zacks Rank #3 (Hold) stock in their portfolio can stay invested and enjoy the regular cash distribution. It will be better for new investors to wait a little longer and find a better entry point.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-24 | |

| Feb-24 | |

| Feb-24 | |

| Feb-23 | |

| Feb-23 | |

| Feb-23 | |

| Feb-21 | |

| Feb-20 | |

| Feb-20 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 |

This Pipeline Operator Blips Up On Takeover Reports As AI Could Make 'Electricity The New Oil'

ET

Investor's Business Daily

|

| Feb-19 | |

| Feb-18 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite