|

|

|

|

|||||

|

|

|

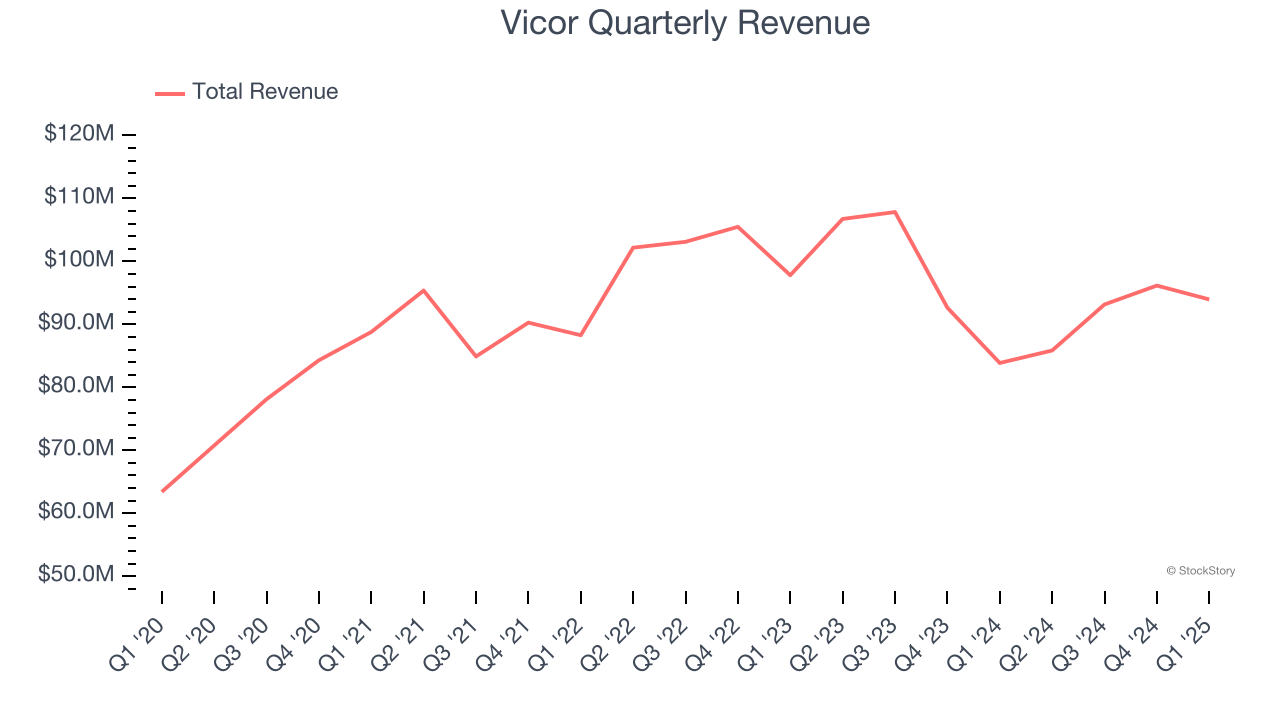

Power conversion and control solutions provider Vicor Corporation (NASDAQ:VICR) missed Wall Street’s revenue expectations in Q1 CY2025, but sales rose 12% year on year to $93.97 million. Its GAAP profit of $0.06 per share was 69.2% below analysts’ consensus estimates.

Is now the time to buy Vicor? Find out by accessing our full research report, it’s free.

Commenting on first quarter performance, Chief Executive Officer Dr. Patrizio Vinciarelli stated: “Revenues and gross margins declined sequentially, with reduced income from a licensee transitioning to a new generation of unlicensed products. Margin improvements await higher utilization of our ChiP fab and increased income from existing and future licensees. Licensing has been gaining traction with OEMs and hyper-scalers wishing to avoid infringing hardware being excluded from importation into the US.”

Founded by a researcher at the Massachusetts Institute of Technology, Vicor (NASDAQ:VICR) provides electrical power conversion and delivery products for a range of industries.

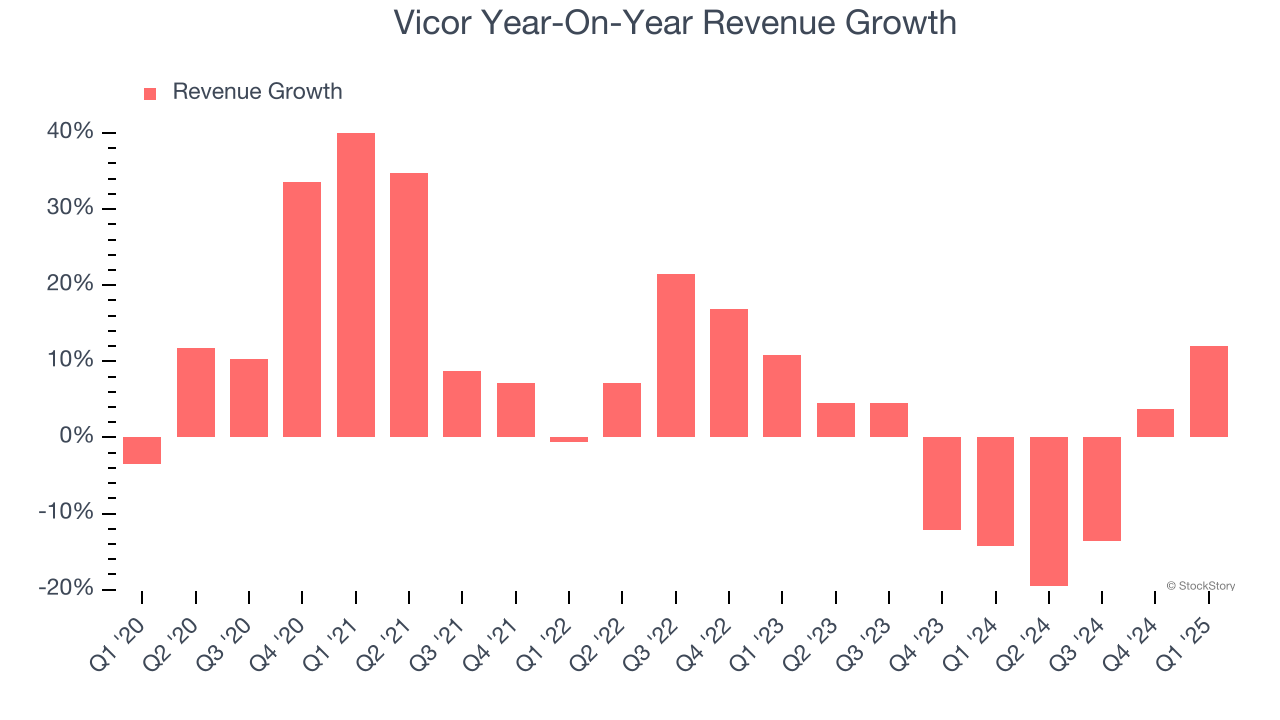

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, Vicor’s sales grew at a mediocre 7.2% compounded annual growth rate over the last five years. This was below our standard for the industrials sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Vicor’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 5% annually. Vicor isn’t alone in its struggles as the Electronic Components industry experienced a cyclical downturn, with many similar businesses observing lower sales at this time.

This quarter, Vicor’s revenue grew by 12% year on year to $93.97 million but fell short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 15.8% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and suggests its newer products and services will catalyze better top-line performance.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

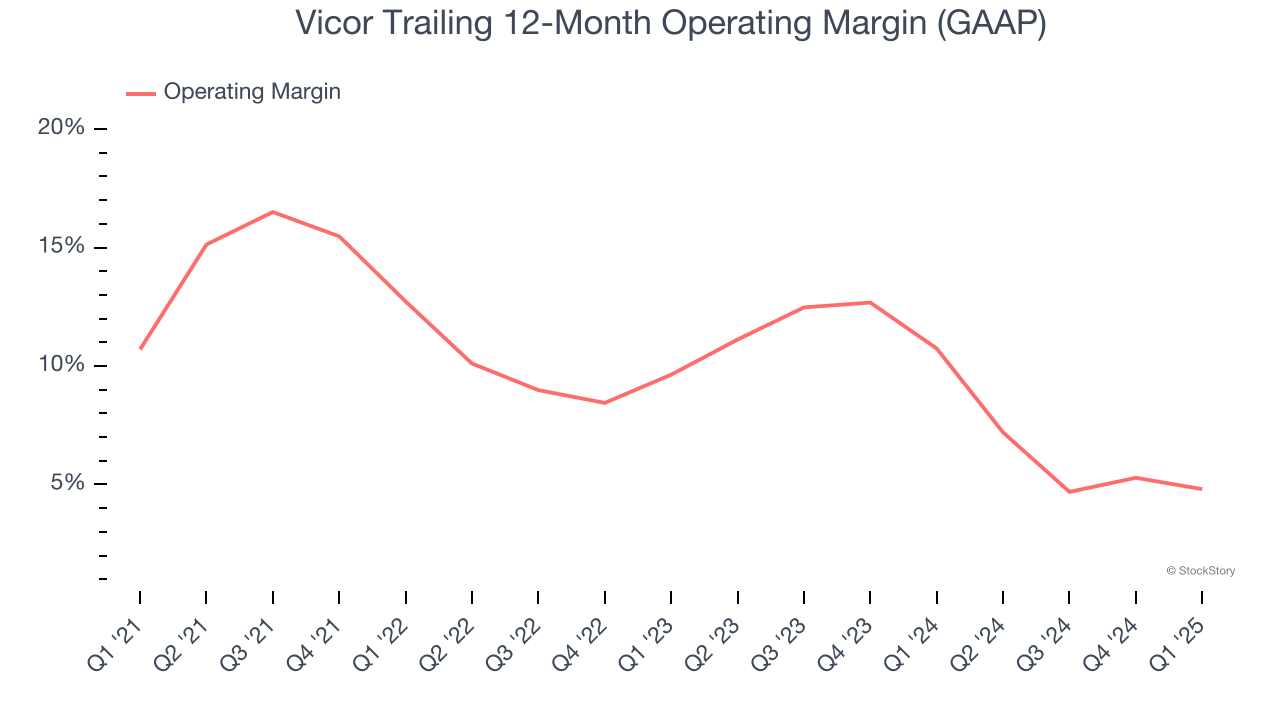

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Vicor has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 9.7%, higher than the broader industrials sector.

Analyzing the trend in its profitability, Vicor’s operating margin decreased by 5.9 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Vicor’s breakeven margin was down 1.5 percentage points year on year. Since Vicor’s gross margin decreased more than its operating margin, we can assume its recent inefficiencies were driven more by weaker leverage on its cost of sales rather than increased marketing, R&D, and administrative overhead expenses.

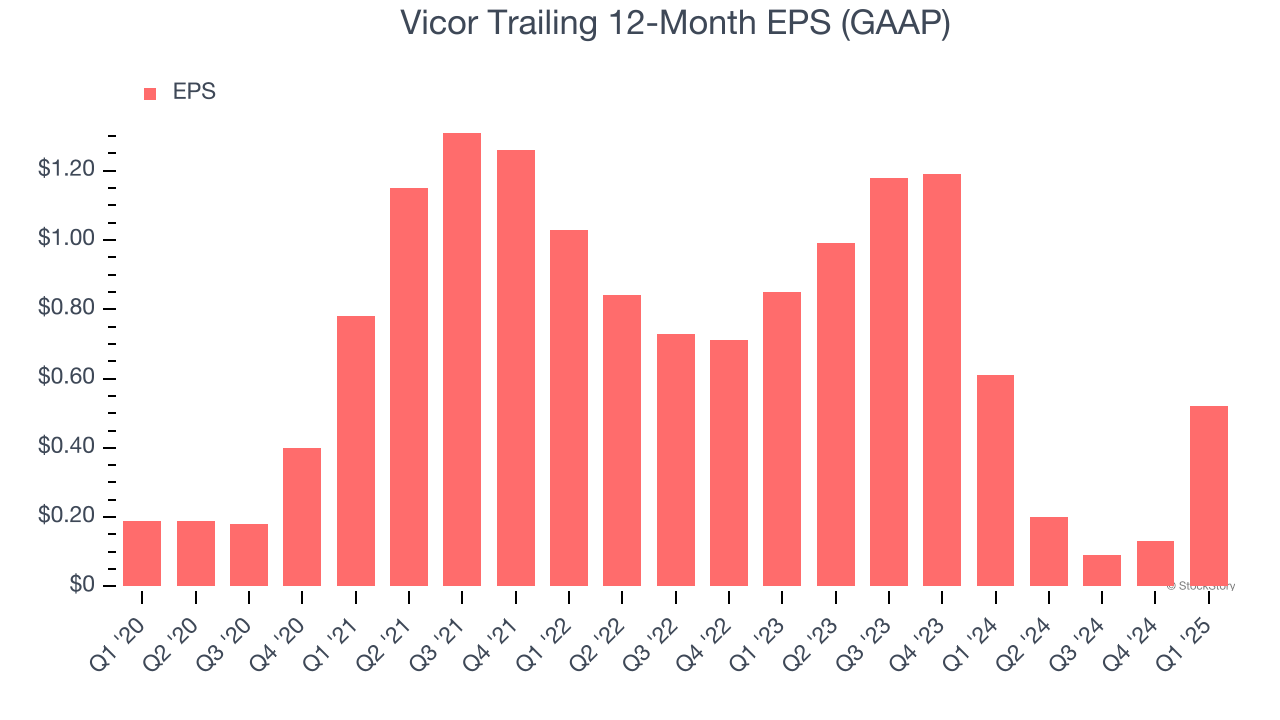

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Vicor’s EPS grew at an astounding 22.3% compounded annual growth rate over the last five years, higher than its 7.2% annualized revenue growth. However, we take this with a grain of salt because its operating margin didn’t expand and it didn’t repurchase its shares, meaning the delta came from reduced interest expenses or taxes.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

Vicor’s two-year annual EPS declines of 21.8% were bad and lower than its two-year revenue performance.

In Q1, Vicor reported EPS at $0.06, up from negative $0.33 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects Vicor’s full-year EPS of $0.52 to grow 148%.

We struggled to find many positives in these results as its revenue and EPS fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 11.5% to $46.03 immediately following the results.

Vicor may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-19 | |

| Feb-11 | |

| Feb-06 | |

| Feb-05 | |

| Feb-04 | |

| Jan-23 | |

| Jan-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite