|

|

|

|

|||||

|

|

|

3M Company MMM and Honeywell International Inc. HON are two prominent names operating in the Zacks Diversified Operations industry. As rivals, both companies compete in multiple sectors with significant overlap in industrial products, consumer goods and safety and security markets.

With considerable exposure in diverse markets, both companies invest heavily in research and development to innovate new products, drive growth and gain market share. But which one is a better investment today? Let’s take a closer look at their fundamentals, growth prospects and challenges to make an informed choice.

The strongest driver of 3M’s business at the moment is the Safety and Industrial segment. Strength in roofing granules, industrial adhesives and tapes, and electrical markets has been driving the segment’s performance. Significant orders for aluminum high-capacity conductors and power cable accessories, driven by growth in demand from data centers and renewable energy projects, augur well for the segment in the quarters ahead. The segment’s organic sales improved 2.5% year over year in the first quarter of 2025.

The company’s Transportation and Electronics segment is benefiting from strength in the transportation and aerospace end markets. Solid momentum in the commercial aircraft and defense-related business and project wins in the advanced materials business are proving beneficial for the segment. The segment’s adjusted organic revenues grew 1.1% in the first quarter.

3M is committed to rewarding its shareholders handsomely through dividend payments and share buybacks. In the first quarter of 2025, the company rewarded its shareholders with $396 million in dividends and $1.3 billion in buybacks. Also, in 2024, it paid dividends worth $2 billion and repurchased shares for $1.8 billion. Exiting the first quarter, the company had $6.6 billion remaining under the share repurchase program. In February 2025, it hiked its quarterly dividend by 4%.

Despite the positives, weakness in the consumer retail end markets, led by a decrease in consumer discretionary spending, remains a persistent concern. This is reflected in the Consumer segment’s results, which declined 1.4% in the first quarter. There was a particular weakness in the command and packaging expression businesses.

MMM’s high debt level remains another concern for its profitability. Exiting first-quarter 2025, the company’s long-term debt was $12.3 billion, reflecting an increase of 10.8% sequentially. Its short-term borrowings and current portion of long-term debt totaled $1.2 billion. Considering its high debt level, 3M’s cash and cash equivalents of $6.3 billion do not look impressive. It’s worth noting that MMM’s long-term debt-to-capital ratio is currently 73.1%, much higher than the industry’s 55.2%.

The company has also been subject to several litigations, including earplug lawsuits. It has committed substantial funds to resolve these disputes, as ongoing litigation might lead to additional expenses. Per the terms of the Combat Arms Earplug settlement announced in August 2023, 3M agreed to pay a sum of $6 billion to resolve the litigation case over the period from 2023 to 2029.

Honeywell is experiencing strength in its commercial aviation aftermarket business, driven by growth in air transport flight hours, higher shipset deliveries and supply-chain improvements. In the first quarter of 2025, its commercial aviation aftermarket sales increased 14% year over year. Strength in its defense and space business, owing to stable U.S. and international defense spending volumes and sustained demand from the current geopolitical climate, has also been proving beneficial. In the first quarter, sales from its defense and space business surged 23% year over year.

Solid demand for its products and solutions, led by increasing building projects, particularly in North America and the Middle East, will likely be beneficial for the Building Automation segment. Increasing order rates in data centers, airports and hospitality projects also bode well for it. Also, strength in the Universal Oil Products business, driven by higher refining and petrochemicals projects, bodes well for the Energy and Sustainability Solutions segment. Exiting the first quarter, the company’s overall backlog grew 8% year over year to $36.1 billion.

HON’s commitment to rewarding its shareholders through dividends and share buybacks is encouraging. It paid out dividends worth $732 million and repurchased shares worth $1.9 billion in the first quarter of 2025. Also, in 2024, it paid out dividends of $2.9 billion and repurchased shares worth $1.66 billion. In September 2024, it hiked its quarterly dividend by approximately 5% to $1.13 per share. Strong free cash flow generation supports the company’s shareholder-friendly activities. For 2025, it expects free cash flow to be in the range of $5.4-$5.8 billion.

However, weakness in the Industrial Automation segment has remained a concern for HON. Lower demand for smart energy and thermal solutions has been affecting the Process solutions business’ performance under the segment. Also, the weakened demand for personal protective equipment within the sensing and safety technologies business, along with softness in the productivity solutions business, remains concerning.

The company exited the first quarter with long-term debt of $25.7 billion. The high debt level was primarily attributable to the funds raised for the Civitanavi Systems, CAES, Global Access Solutions and LNG acquisitions. Considering its high debt level, its cash and cash equivalents of $9.7 billion do not look impressive. Its long-term debt-to-capital ratio is currently 58.8%, higher than 55.2% of the industry.

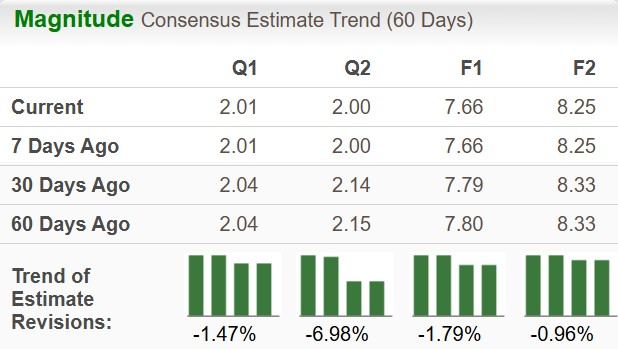

While the Zacks Consensus Estimate for MMM’s 2025 sales implies a year-over-year decline of 9.8%, the same for its earnings per share (EPS) indicates growth of 4.9%. The EPS estimates for both 2025 and 2026 have declined over the past 60 days.

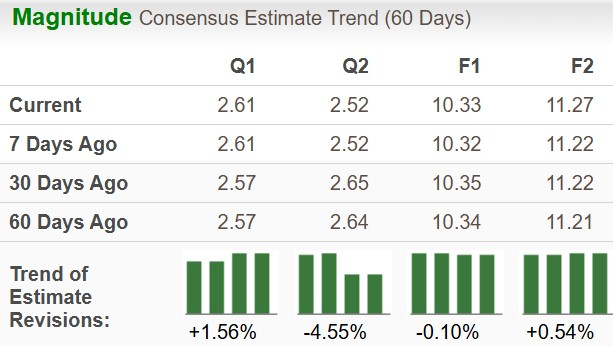

The Zacks Consensus Estimate for HON’s 2025 sales and EPS implies year-over-year growth of 4.4% and 4.5%, respectively. While Honeywell’s EPS estimates for 2025 have declined, the estimates for 2026 have increased over the past 60 days.

In the past three months, 3M shares have lost 7.4%, while Honeywell stock has gained 2.9%.

3M is trading at a forward 12-month price-to-earnings ratio of 17.62X, above its median of 12.03X over the last three years. Honeywell’s forward earnings multiple sits at 20.15X, close to its median of 20.05X over the same time frame.

3M and Honeywell have a Zacks Rank #3 (Hold) each, which makes choosing one stock a difficult task. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

3M’s strength in the safety, industrial and transportation markets has been dented by the continued weakness in its consumer retail market. The legal battle surrounding its earplug lawsuits has created a bearish sentiment around the stock. Also, MMM’s downward earnings estimate revisions for both 2025 and 2026 warrant a cautious approach for existing investors.

In contrast, Honeywell’s market leadership position, diversified portfolio, growth investments and strong dealer network provide it with a competitive advantage to leverage the long-term demand prospects in the aerospace and industrial markets. Despite its steeper valuation, HON seems to be a better pick due to strong estimates, stock price appreciation and better prospects for sales and profit growth.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-17 | |

| Feb-16 | |

| Feb-15 | |

| Feb-14 | |

| Feb-13 | |

| Feb-13 | |

| Feb-12 | |

| Feb-12 | |

| Feb-11 | |

| Feb-11 | |

| Feb-11 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite