|

|

|

|

|||||

|

|

|

Cisco Systems CSCO is set to release its third-quarter fiscal 2025 results on May 14.

The company anticipates third-quarter fiscal 2025 revenues between $13.9 billion and $14.1 billion. Non-GAAP earnings are expected between 90 and 92 cents per share.

The Zacks Consensus Estimate for revenues is pegged at $14.05 billion, indicating growth of 10.58% from the year-ago quarter’s reported figure. The consensus mark for earnings has been steady at 91 cents per share over the past 30 days, suggesting year-over-year growth of 3.41%.

CSCO’s earnings surpassed the Zacks Consensus Estimate in all the trailing four quarters, the average being 4.07%. (Find the latest EPS estimates and surprises on Zacks Earnings Calendar.)

Cisco Systems, Inc. price-eps-surprise | Cisco Systems, Inc. Quote

Let’s see how things are shaping up prior to this announcement.

Cisco’s third-quarter fiscal 2025 results are expected to have benefited from improved demand for networking products driven by switching, enterprise routing, webscale infrastructure, and industrial networking applications. Increasing return-to-office policies are expected to have helped improve demand for CSCO’s campus switching portfolio. Strong demand for data center switches, thanks to the availability of 800gig Nexus switches based on Cisco’s 51.2 terabit Silicon One chip, is noteworthy.

The Zacks Consensus Estimate for fiscal third-quarter Networking revenues is currently pegged at $6.76 billion, indicating a 3.6% year-over-year growth.

Cisco is benefiting from strong security growth, driven by robust demand for solutions like XDR, Secure Access and Multicloud Defense suites. The addition of Splunk has been a key catalyst. In the second quarter of fiscal 2025, Security orders more than doubled year over year, driven by the advanced threat intelligence capabilities of Splunk.

The Zacks Consensus Estimate for fiscal third-quarter Security revenues is currently pegged at $2.195 billion, indicating 68.3% year-over-year growth.

However, higher tariffs post the “Liberation Day” announcement and macroeconomic challenges are expected to have negatively impacted Cisco’s order growth in the to-be-reported quarter.

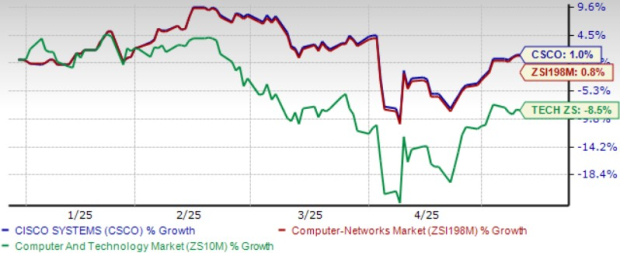

Cisco shares have gained 1% year to date, outperforming the Zacks Computer & Technology sector’s decline of 8.5% and the Zacks Computer Networking industry’s return of 0.8%, as well as industry peers like Extreme Networks EXTR. Shares of Extreme Networks have declined 11.5%.

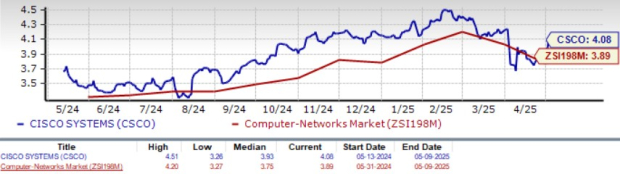

However, Cisco stock is not so cheap, as the Value Score of D suggests a stretched valuation at this moment.

In terms of the forward 12-month P/S ratio, CSCO is trading at 4.08X, higher than the industry’s 3.89X and Extreme Networks’ 1.63X.

The increase in AI-related workload presents a strong growth opportunity for Cisco, thanks to an innovative portfolio. Cisco’s aggressive investments in AI, cloud, and security are noteworthy. Cisco had AI infrastructure orders worth more than $700 million at the end of the first half of fiscal 2025 and remains on track to surpass $1 billion in AI infrastructure orders in fiscal 2025.

Cisco’s strategy of infusing AI across Security and Collaboration platforms and developing Agentic capabilities across the portfolio is a key catalyst. It is leveraging Agentic AI to improve customer experience. The launch of Renewals Agent, an Agentic AI-driven solution co-developed with Mistral, and a new Assistant to help customers digitize and de-risk Network Change Management have been noteworthy developments in this regard.

Cisco’s security business is benefiting from strong demand for both Cisco Secure Access and XDR. On a combined basis, both solutions have gained more than 1,000 customers in the trailing 12 months, and each of the products has roughly one million enterprise users. Hypershield is also gaining traction.

Cisco’s rich partner base, which includes Meta Platforms, Microsoft, NVIDIA NVDA, Lenovo and ServiceNow NOW, deserves attention.

CSCO’s collaboration with NVIDIA is helping to expand the former’s datacenter infrastructure portfolio. CSCO’s latest NVIDIA-powered AI server and AI PODs, integrated with NVIDIA’s AI Enterprise cloud-native software and managed via Cisco Intersight, simplify and de-risk AI infrastructure. The company is expanding its portfolio by unveiling AI factory architecture developed in collaboration with NVIDIA. This is expected to drive up Cisco’s AI-driven revenues.

Cisco deepened its partnership with ServiceNow, combining the former’s infrastructure and security platforms with the latter’s AI-driven platform and security solutions. The first integration brings together Cisco’s AI Defense capabilities with ServiceNow SecOps to provide more holistic AI risk management and governance.

Cisco’s near-term results are expected to benefit from an improving networking business and growing security business, along with a rich partner base. However, tariff-related issues and macroeconomic challenges are major concerns.

Cisco currently carries a Zacks Rank #3 (Hold), which implies that investors should wait for a favorable time to accumulate the stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 29 min | |

| 34 min | |

| 50 min | |

| 3 hours | |

| Jul-26 | |

| Jul-26 | |

| Jul-26 | |

| Jul-26 | |

| Jul-26 | |

| Jul-26 | |

| Jul-26 | |

| Jul-26 | |

| Jul-26 | |

| Jul-26 | |

| Jul-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite