|

|

|

|

|||||

|

|

|

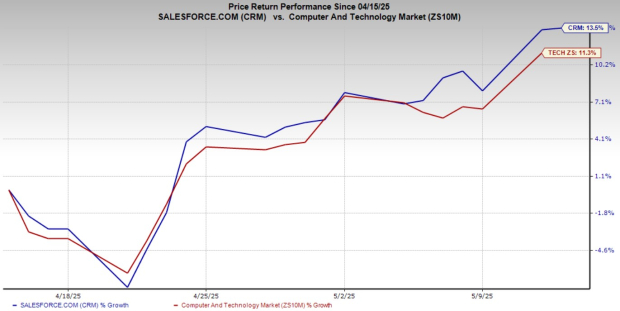

Salesforce, Inc. CRM has seen its share price soar 13.5% over the past month. This surge has significantly outperformed the broader Zacks Computer and Technology sector, which gained 11.3% during the same period.

This outperformance raises the question: Should investors book profits and exit or continue holding the stock?

Salesforce’s recent rally stemmed from broader market optimism. Progress in U.S.-China trade negotiations has been boosting market sentiment since late April. Protracted trade tensions had previously dampened global economic forecasts and corporate earnings expectations due to tariffs and retaliatory measures.

Earlier this week, the United States and China reached a deal to slash tariffs temporarily. The United States has agreed to lower its overall tariffs on Chinese imports to 30% from 145%. On the other hand, China will reduce duties on U.S. imports to 10% from 125%. The new adjustments will be effective for 90 days.

The recent trade deal suggests easing tensions between the two largest economies and smoother international trade flows. This improved outlook fostered investor confidence, leading to a rally in the equity market as fears of further economic disruption subsided and prospects for global growth seemed brighter.

Apart from Salesforce, this broader market optimism also boosted share prices of other enterprise software makers, including Oracle Corporation ORCL, Microsoft Corporation MSFT and SAP SE SAP. Over the past month, shares of Oracle, Microsoft and SAP have soared 21.2%, 16.4% and 10.6%, respectively.

Salesforce’s long-term growth potential, along with invigorated investor optimism, makes the stock worth holding at the moment.

Salesforce remains the undisputed leader in the field of customer relationship management (“CRM”) software. The company continues to outpace competitors such as Microsoft, Oracle and SAP, holding the largest market share, according to Gartner’s rankings. This dominance isn’t fading anytime soon.

Salesforce has built an extensive ecosystem that integrates seamlessly across enterprise applications. Its acquisitions — such as Slack and, more recently, the Own Company — demonstrate a long-term strategy of expanding its footprint beyond CRM into enterprise collaboration, data security and artificial intelligence (AI)-driven automation.

AI is a key part of Salesforce’s growth engine. Since launching Einstein GPT in 2023, the company has embedded generative AI capabilities across its entire platform, allowing customers to automate workflows, enhance decision-making and improve customer interactions. As generative AI adoption accelerates across industries, Salesforce is positioned to capitalize on this trend.

Another long-term tailwind is rising global spending on generative AI. Gartner estimates that worldwide generative AI spending will hit $644 billion in 2025, implying a 76.4% year-over-year increase. Enterprise software, a key segment for Salesforce, is expected to grow even faster, with a projected 93.9% increase. Even if economic conditions slow down spending in the short term, digital transformation remains a top priority for businesses, ensuring steady demand for Salesforce’s solutions.

Despite the recent rally, Salesforce shares are trading at a discounted valuation multiple compared to the Zacks Computer – Software industry. The stock currently trades at a forward 12-month price-to-earnings (P/E) multiple of 25.24X, below the industry average of 31.77X.

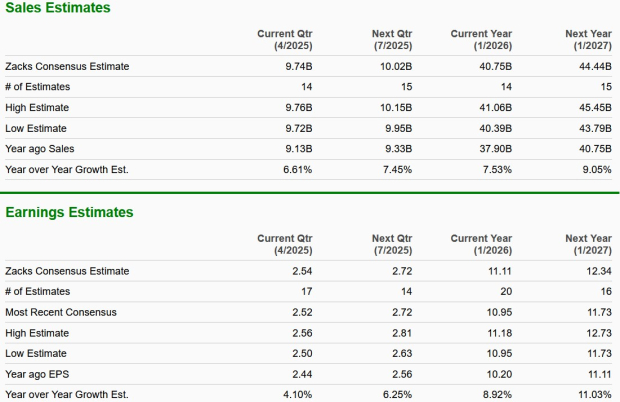

While Salesforce’s long-term prospects shine brightly, the company faces significant near-term challenges. Revenue growth has decelerated from its historical double-digit pace to single-digit increases in recent quarters. This slowdown reflects cautious enterprise spending amid economic uncertainty and geopolitical pressures. Analysts anticipate that this trend will persist, with mid-to-high single-digit growth expected for fiscal 2026 and 2027.

The slowdown highlights a shift in enterprise behavior, with businesses favoring smaller, incremental projects over large-scale digital transformations. For Salesforce, this means recalibrating its approach to maintain relevance in a changing IT spending environment.

Salesforce remains a dominant player in enterprise software with strong positioning in AI and the CRM software market. Its current valuation is reasonable, and long-term tailwinds like AI adoption and digital transformation continue to support the growth story. Though slowing sales growth remains a major concern, the company is expected to witness a strong recovery once the macroeconomic and trade environment improves.

So, for investors with a long-term view, holding the stock is the right move. CRM carries a Zacks Rank #3 (Hold) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 3 min | |

| 8 min | |

| 12 min | |

| 20 min | |

| 21 min | |

| 37 min | |

| 42 min | |

| 46 min |

Salesforce Stock Falls Amid Weaker-Than-Expected Fiscal 2027 Revenue Outlook

CRM

Investor's Business Daily

|

| 46 min | |

| 47 min | |

| 50 min | |

| 52 min | |

| 54 min | |

| 54 min | |

| 57 min |

Salesforce Sees Stable Sales Growth Amid Concerns of AI's Threat to Software

CRM

The Wall Street Journal

|

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite