|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

Reporting its Q1 results this morning, Walmart WMT was able to exceed expectations but warned that its prices will rise as the omnichannel retailer can’t avoid passing on the high costs of tariffs to its customers.

The news didn’t cause a dent to the broader market’s continued rebound as the benchmark S&P 500 was up +0.41% on Thursday, although WMT was down half a percentage point.

Walmart shares have been a pleasant hedge against market volatility and are up +7% this year, with the benchmark virtually flat. More impressive, WMT has soared nearly +100% in the last three years, making it a worthy topic of whether it's time to buy, sell, or hold Walmart stock.

Highlighting its e-commerce expansion, Walmart’s Q1 sales were up 2% to $165.6 billion and edged estimates of $165.59 billion. Walmart’s international sales grew by nearly 8%, stating its global e-commerce business grew by 22%, with each segment delivering growth of at least 20%.

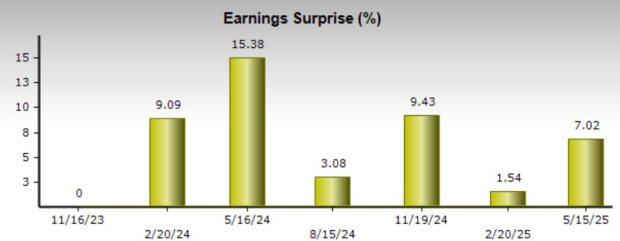

On the bottom line, Q1 EPS came in at $0.61 versus $0.60 per share a year ago and exceeded expectations of $0.57 by 7%. Notably, Walmart has reached or exceeded the Zacks EPS Consensus for 11 consecutive quarters with an average earnings surprise of 5.26% in its last four quarterly reports.

Providing guidance for the second quarter, Walmart expects Q2 sales to increase by 3.5%-4.5%, which falls in line with Zacks' estimates of $174.71 billion or 3% growth. However, Walmart withheld its Q2 EPS guidance due to uncertainty around tariffs.

Optimistically, Walmart maintained its full-year forecast for annual sales growth of 3%-4% and adjusted EPS between $2.50-$2.60. Walmart CFO David Rainey also pointed out that during periods of economic uncertainty, the company tends to gain market share and expects this period to be no different.

While Walmart’s strong financial performance has captivated investors in recent years, it’s noteworthy that WMT is still trading at a noticeable P/E premium to its peers and the S&P 500’s 22.6X forward earnings multiple.

At 37.3X forward earnings, WMT is noticeably above Target’s TGT 10.6X and its Zacks Retail-Supermarkets Industry average of 14.2X. Still, Walmart does check the box in terms of price-to-sales, trading at less than 2X.

Following its Q1 report, Walmart stock lands a Zacks Rank #3 (Hold) and should remain a viable long-term investment. That said, considering Walmart’s P/E premium, more upside or downside risk may largely depend on the direction of earnings estimate revisions in the coming weeks as analysts digest the impact higher prices could have on the retailer's outlook despite maintaining its full year guidance.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 5 hours | |

| 6 hours | |

| 7 hours | |

| 10 hours | |

| 10 hours | |

| 14 hours | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 |

Stock Market Mixed With Walmart, Iran, Trump Tariff Ruling In Focus: Weekly Review

WMT

Investor's Business Daily

|

| Feb-20 | |

| Feb-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite