|

|

|

|

|||||

|

|

|

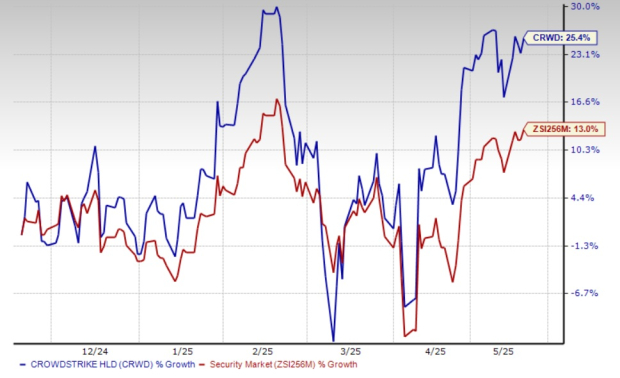

CrowdStrike CRWD has benefited significantly from the recent gains in the technology sector, as renewed optimism about the U.S.–China trade negotiations boosted overall market sentiment.

Despite experiencing significant volatility over the past six months, the stock returned 25.4%, outperforming the Zacks Security industry’s 13% growth. However, the question remains whether this growth is short-lived or if CrowdStrike stock represents a viable long-term investment opportunity.

CrowdStrike increased its Subscription revenues by 27% from the year-ago quarter to cross $1 billion in quarterly revenues in the fourth quarter of fiscal 2025. This was partly achieved due to the Falcon Flex Subscription Model, which allows customers to commit upfront and later choose modules, eliminating procurement friction.

CrowdStrike’s subscription customers, who adopted five or more cloud modules, represented 67% of the total subscription customers. Those with six or more cloud modules accounted for 48%, and those with seven or more cloud modules represented 32% as of Jan. 31, 2025.

CrowdStrike’s Falcon platform is gaining popularity as an “AI-native SOC,” with strong adoption in Charlotte AI Agentic Detection Triage, Workflows and Response. CrowdStrike is partnering with other AI companies to expand its capabilities.

CrowdStrike integrated its Falcon cybersecurity platform into NVIDIA's Enterprise AI Factory to enable enterprises to secure their AI systems, covering data ingestion, model training, and deployment. The company also collaborated with Extrahop to solve the rising concern of shadow AI. New introductions, including AI Model Scanning and AI Security Dashboard by CRWD, along with its strong partnerships, will likely help the company gain more customers.

CrowdStrike is facing several challenges related to customers’ negative sentiments since the global IT outage incident on July 19, 2024. The company has been implementing the Customer Commitment Package to retain its customers, which includes product additions and discounts, hence compressing its revenue recognition and profitability.

Despite all these measures, the company’s upsell into existing customers showed signs of slowdown and the churn rate remained moderate. Moreover, a report by Bloomberg reported that CrowdStrike is currently under federal investigation by the U.S. Department of Justice and the Securities and Exchange Commission (SEC) over a $32 million deal with Carahsoft Technology.

The deal, meant to supply cybersecurity tools to the IRS, was reportedly never fulfilled, raising concerns of financial irregularities. Authorities are examining whether CrowdStrike engaged in pre-booking or channel stuffing to inflate financial results, while CRWD maintains that it handled the transaction appropriately.

The ongoing investigation creates legal and reputational risks, softening investors’ confidence. While CrowdStrike maintains that it handled the transaction appropriately, the ongoing investigation creates legal and reputational risks, softening investors’ confidence.

Amid customer backlash and ongoing regulatory scrutiny that could damage CrowdStrike’s reputation, competitors may seize the opportunity to attract and convert its customer base. The cybersecurity space already contains players like Palo Alto Networks PANW, SentinelOne S and Cisco CSCO, who provide similar products like CrowdStrike.

For instance, CrowdStrike’s Falcon Extended Detection and Response that connects multiple layers, including email, endpoints, servers, cloud workloads, and network, to provide a comprehensive security competes with SentinelOne’s Singularity platform, which provides AI-powered endpoint protection and extended detection and response (XDR). SentinelOne also offers Autonomous threat hunting and remediation like CRWD.

Cisco also provides XDR features combined with other Cisco products. Like CRWD, Palo Alto Networks provides endpoint protection through Cortex XDR, which combines endpoint, network, and cloud data to detect and respond to threats. On the other hand, Palo Alto Networks’ Prisma Cloud competes with CRWD’s Falcon Cloud Security.

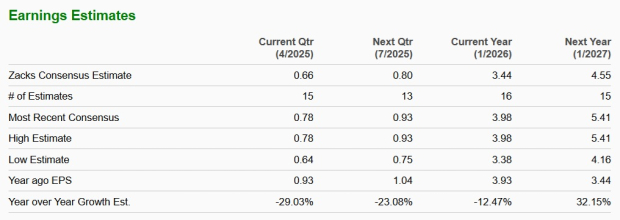

All the above factors combinedly could weigh on CRWD’s profitability in the near term. The Zacks Consensus Estimate for CrowdStrike’s fiscal 2026 earnings indicates a year-over-year decline of 12.5%. (Find the latest EPS estimates and surprises on Zacks Earnings Calendar.)

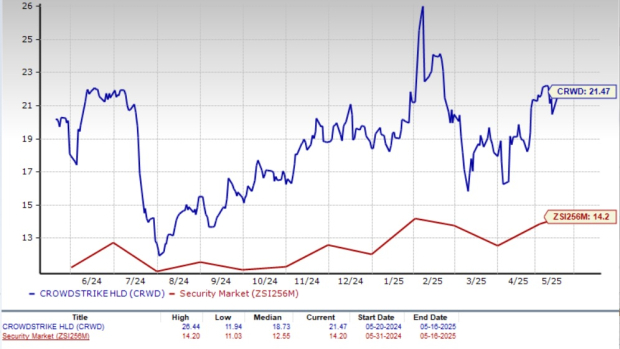

CrowdStrike is currently trading at a high price-to-sales (P/S) multiple, far above the Zacks Security industry. CrowdStrike’s forward 12-month P/S ratio sits at 21.47X, significantly higher than the Zacks Security industry’s forward 12-month P/S ratio of 14.20X.

CrowdStrike’s disappointing profit outlook for fiscal 2026, coupled with rising costs and deteriorating margins, makes this Zacks Rank #4 (Sell) stock less attractive in the near term.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 7 hours | |

| 10 hours | |

| 12 hours | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 |

How The AI Bubble Could Burst. Lessons From The Dot-Com Stock Market Crash.

CSCO

Investor's Business Daily

|

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite