|

|

|

|

|||||

|

|

|

New Feature: See Wall Street analyst ratings directly on Finviz charts for deeper context into price action.

Shares of Astronics Corporation ATRO have surged a solid 48% over the past month, outperforming the S&P 500’s return of 15.3%. The stock has also surpassed the Zacks Aerospace-Defense Equipment industry’s gain of 16.5% and the broader Zacks Aerospace sector’s growth of 15.8% in the said time frame.

Other industry players like Leonardo DRS DRS and Curtiss-Wright Corp. CW have also delivered a similar stellar performance in the aforementioned period. Shares of CW and DRS have surged 32.2% and 21.3%, respectively, over the past month.

With ATRO rallying high, backed by steadily increasing global air traffic and rapidly enhancing defense investments worldwide, investors may rush to add this stock to their portfolio right away. However, before making any hasty decision, let’s delve deep into what made ATRO’s share price shoot up, whether there is more room for growth in the near future, and if there’s any risk to investing in it.

The primary factor that drove ATRO’s share price over the past month was its impressive first-quarter 2025 results. Notably, Astronics reported an 11.3% year-over-year increase in its quarterly revenues, backed by a 17% rise in its Aerospace segment sales. Additionally, the company's gross profit improved 28.1% year over year, with gross margins expanding a solid 380 basis points to 29.5%.

Such strong profitability and a lower interest rate expense culminated in a notable improvement in ATRO’s first-quarter net income to $9.5 million from the year-ago quarter’s reported net loss of $3.2 million. The company also achieved record bookings of $279.7 million in this quarter, which translated into a backlog of $673 million as of March 2025, marking the highest backlog recorded in Astronics’ history.

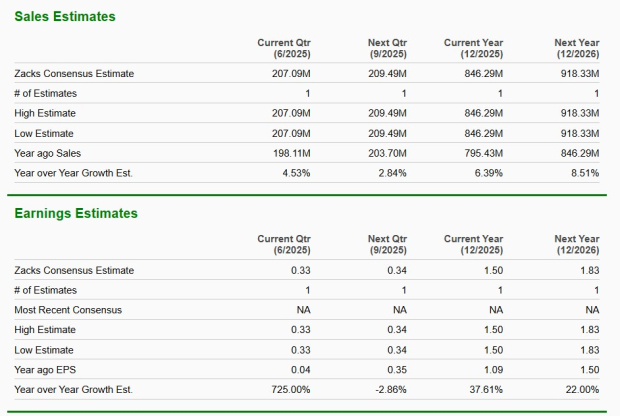

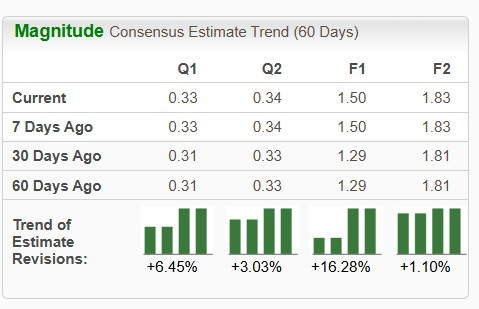

No doubt, such an impressive quarterly performance bolstered analysts’ optimism regarding Astronics' earnings prospects, which got duly reflected in its improved estimates lately and thus added more impetus to its share price movement. The Zacks Consensus Estimate for the current quarter's earnings per share (EPS) has gone up 6.5% over the past 30 days to 33 cents, reflecting a havoc 725% improvement from the prior-year quarter's figure.

Astronics ended first-quarter 2025 with cash and cash equivalents of $26 million, reflecting a 44.4% improvement sequentially. While its long-term debt totaled $160 million as of March 29, 2025, its current debt was nil. So, it is safe to conclude that ATRO boasts a solid solvency position in the near term, which, in turn, should enable it to invest in new technological innovation. Notably, technological innovation is Astronics’ primary unique selling proposition (USP), as the company delivers advanced technologies to the global aerospace and defense industries.

As the U.S. government continues to steadily increase its defense budget funding, with the current President Trump having proposed a 13% increase in the nation’s defense spending (to $1.01 trillion) for fiscal 2026, growth prospects remain solid for New York-based Astronics Corporation. Notably, the company offers innovative, mission-critical electronic technology solutions that are integrated into various defense weapons, ranging from aircraft cockpits to ground vehicles and missile systems.

On the other hand, as airlines expand their fleets and enhance passenger experiences, driven by rapidly growing air travel demand worldwide, there is a heightened demand for advanced cabin power systems and in-flight entertainment and connectivity (IFEC) solutions. This should bode well for Astronics, which is already capitalizing on this trend, as evident from the 13.3% year-over-year increase in its Commercial Transport sales in the first quarter of 2025.

Now let’s take a quick sneak peek at ATRO’s near-term earnings and sales estimates to check whether they also reflect similar growth prospects.

The Zacks Consensus Estimate for ATRO’s 2025 sales suggests year-over-year growth of 6.4%, while that for 2026 sales indicates an improvement of 8.5%.

The 2025 and 2026 bottom-line estimates show a similar improving trend. Moreover, the upward revision in its yearly earnings estimate indicates that investors are gaining confidence in this stock’s earnings capabilities.

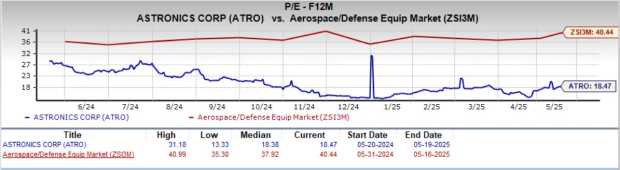

In terms of valuation, ATRO’s forward 12-month price-to-earnings (P/E) is 18.47X, a discount to its industry’s average of 40.44X. This suggests that investors will be paying a lower price than the company's expected earnings growth compared to that of its peer group.

On the other hand, ATRO’s industry peers are also trading at a discount. While CW is trading at a forward 12-month P/E of 32.45X, DRS is trading at 36.61X.

While growth opportunities in the global aerospace and defense space remain immense, some challenges persist, which investors should consider before investing in Astronics. Notably, the primary challenges that stocks like ATRO, CW, and DRS continue to face include varying levels of supply-chain pressures stemming from the residual impacts of the COVID-19 pandemic, scarcity in material availability and cost increases, and a rise in labor costs and labor availability, particularly for skilled labor.

Moreover, the recently imposed heightened tariff on the import of goods from almost all trading partners of the United States is likely to exacerbate the supply chain challenge, which, altogether, might cause a delay in ATRO delivering its finished products. This, in turn, may hurt its operational results.

To conclude, investors interested in ATRO may consider adding this stock to their portfolio, given its discounted valuation, upbeat near-term sales estimates, impressive share price performance, and upward revision in earnings estimates. The stock has a VGM Score of A, which is also a favorable indicator of strong performance.

The company’s Zacks Rank #1 (Strong Buy) further supports our thesis. You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Feb-20 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-17 | |

| Feb-17 | |

| Feb-16 | |

| Feb-13 | |

| Feb-12 | |

| Feb-12 | |

| Feb-12 |

Howmet Aerospace Pops. Earnings, Upgrade Fuel Bullish Defense Surge.

CW +5.80%

Investor's Business Daily

|

| Feb-12 | |

| Feb-12 | |

| Feb-12 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite