|

|

|

|

|||||

|

|

|

Visa Inc. V and American Express Company AXP are both giants in the payment solutions space, operating at the heart of finance and commerce globally. Both companies benefit from the steady rise of digital payments, expanding e-commerce, and the rebound in consumer travel and spending. Despite these commonalities, their business models differ in ways that can impact investor returns.

Visa runs an asset-light, transaction-based network, making it a toll collector of sorts in the overall payment structure. Meanwhile, AmEx blends payment processing with direct lending, offering a more vertically integrated and consumer-engaged experience. With interest rates high and economic growth uncertain, these differences now carry more weight in evaluating future gains.

Let’s dive deep and closely compare the fundamentals of the two stocks to determine which one holds more promise now.

American Express continues to prove that its premium, relationship-driven model delivers results. Unlike Visa, which just processes payments, AmEx earns from both transaction fees and lending, allowing it to capture more value per customer. Its closed-loop payment system also gives it richer data, fueling targeted marketing and superior customer loyalty programs.

In the first quarter of 2025, AmEx reported 7% year-over-year revenue growth, with younger demographics (Millennials and Gen Z) driving customer base expansion. Network volumes of $439.6 billion rose 5% year over year, while total interest income of $6.1 billion increased 6%. Its first-quarter 2025 EPS of $3.64 beat the Zacks Consensus Estimate by 5.5%. It beat earnings estimates in each of the past four quarters, with an average surprise of 5.2%.

American Express Company price-consensus-eps-surprise-chart | American Express Company Quote

These users are increasingly gravitating toward AmEx’s value propositions, exclusive offers, travel perks and reward points that encourage spending. Even in a high-rate environment, AmEx’s affluent user base continues to spend, especially in travel, dining and entertainment. As one of Berkshire Hathaway’s longest-standing holdings, the company is often regarded as a quality stock.

While Visa enjoys global breadth, AmEx’s depth within its user base is unmatched. Its cardmembers spend more and stay longer. Yes, AmEx bears credit risk, but it’s managing that risk well, with delinquency rates remaining below historical averages. Provision for credit losses declined 9% year over year to $1.2 billion in the first quarter. Its robust balance sheet with cash & cash equivalents of $52.5 billion, selective underwriting, and rising interest income positions it well for continued margin expansion.

Visa’s business model is often praised for being capital-light and relatively risk-free; it simply earns fees for processing payments. Its vast global network spans more than 200 countries, and its financials show consistent revenue and earnings growth.

In the second quarter of fiscal 2025, Visa posted a 9.3% increase in net revenues, with cross-border volume leading the charge thanks to global travel trends. EPS of $2.76 outpaced the Zacks Consensus Estimate by 3% while payments volume increased 8% and processed transactions grew 9% to 60.7 billion. It beat earnings estimates in each of the past four quarters with an average surprise of 3%.

Visa Inc. price-consensus-eps-surprise-chart | Visa Inc. Quote

However, Visa’s strength is also its limitation. The company lacks direct consumer relationships and depends on partners (banks and merchants) to drive volume. In contrast to AmEx, Visa has less control over the end-user experience and limited access to the revenue upside of lending programs.

The company is investing in areas like B2B payments, real-time transfers, cryptocurrency and payment security to diversify its operations. However, Visa faces more regulatory scrutiny worldwide due to its sheer size and influence, which could weigh on long-term margins.

Visa’s dividend yield of 0.64% is a bit higher than its industry average of 0.61% but significantly lower than AmEx’s 1.11%.

The Zacks Consensus Estimate for Visa’sfiscal 2025 sales and EPS implies year-over-year growth of 12.9% and 10.3%, respectively. Similarly, the estimates for AmEx’s 2025 sales and EPS signal 8.1% and 13.7% year-over-year increases. V and AXP’s next year EPS estimates indicate further 12.6% and 14% year-over-year jumps, respectively. While Visa witnessed no earnings estimate revisions in the past week, AmEx garnered one upward movement for both 2025 and 2026, against no movement in the opposite direction.

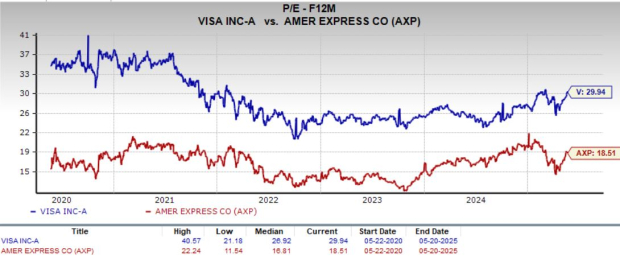

Valuation is where AmEx also pulls ahead. AXP trades at 18.51X forward earnings, offering compelling value given its double-digit growth. Visa, on the other hand, trades at 29.94 forward earnings, a premium multiple that reflects consistency, but leaves less room for upside surprises.

Given the current market conditions, investors may prefer a stock that delivers growth at a reasonable price, and AmEx fits that mold more comfortably than Visa right now.

Over the past year, both stocks have delivered solid returns, but American Express has gained momentum recently. AXP shares have rallied over 17% in the past month, driven by its premium customer base. Visa has also posted a 10.7% gain, while the S&P 500 Index rose 12.6% during this time. AXP’s momentum looks more tied to structural drivers, like generational user growth and lending revenue, while Visa’s growth appears more incremental.

Visa remains a powerful global network with a low-risk model and reliable returns. However, American Express is showing greater upside potential recently. Its dual revenue streams, strong customer loyalty, and growing appeal to younger users give it a unique edge.

With a more attractive valuation and stronger growth levers in a high-rate world, American Express has more room to run at the moment, even though both companies currently carry a Zacks Rank #3 (Hold).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 2 hours | |

| 4 hours | |

| 7 hours | |

| 10 hours | |

| 10 hours | |

| 11 hours | |

| 12 hours | |

| 16 hours | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite