|

|

|

|

|||||

|

|

|

In the high-stakes world of cloud computing, Amazon.com AMZN and Oracle ORCL represent contrasting approaches to capturing the explosive growth in artificial intelligence and enterprise computing. Amazon, with its dominant Amazon Web Services (“AWS”) cloud platform, continues to leverage its first-mover advantage and massive scale, while Oracle positions itself as a specialized provider of database and enterprise applications with growing cloud ambitions through Oracle Cloud Infrastructure.

Both tech giants have made significant investments in AI infrastructure and services, attempting to capitalize on the transformative technology that's reshaping industries worldwide. Let's delve deep and closely compare the fundamentals of the two stocks to determine which one is a better investment now.

Amazon's cloud division, AWS, delivered impressive first-quarter 2025 results with revenues climbing 17% year over year to $29.3 billion, establishing an annualized revenue run rate of $117 billion. This robust performance demonstrates AWS' continued market leadership despite increasing competition. Amazon's aggressive expansion of AI capabilities, including the deployment of next-generation P6-B200 instances powered by NVIDIA Blackwell GPUs, positions the company at the forefront of the AI revolution.

The company's retail business also shows remarkable resilience with record delivery speeds and strong consumer engagement. Amazon has successfully regionalized its fulfillment network, resulting in faster deliveries and lower costs. According to CEO Andy Jassy, everyday essentials grew twice as fast as the rest of the business and represented one out of every three units sold in the United States.

Amazon's strategic investments extend beyond domestic markets. The company recently announced a $5+ billion partnership with Saudi Arabia's HUMAIN to build a groundbreaking "AI Zone," demonstrating its global ambitions. Additionally, Amazon has rapidly expanded its AI model offerings in Bedrock, incorporating leading models from Anthropic, Meta, Mistral AI, and DeepSeek, creating a comprehensive AI ecosystem for developers and enterprises.

The company's financial health is equally impressive, with first-quarter operating income growing 20% year over year to $18.4 billion. Amazon beat Wall Street expectations with EPS of $1.59, exceeding forecasts by 23 cents. The company's diversified revenue streams, spanning e-commerce, cloud computing, digital advertising, and subscription services, provide multiple growth vectors and natural hedges against market volatility.

The Zacks Consensus Estimate for 2025 net sales is pegged at $693.74 billion, indicating growth of 8.74% from the prior-year reported figure. The Zacks Consensus Estimate for 2025 earnings is pegged at $6.3 per share, which indicates a jump of 13.92% from the year-ago period.

Amazon.com, Inc. price-consensus-chart | Amazon.com, Inc. Quote

Find the latest earnings estimates and surprises on Zacks Earnings Calendar.

Oracle's recent performance has failed to impress investors, with third-quarter 2025 results falling short of expectations. Revenues reached $14.13 billion, growing just 6.40% year over year but missing projections by $259.18 million. Similarly, EPS of $1.47 missed estimates by 2 cents, reflecting execution challenges in a highly competitive market.

While Oracle touts its cloud growth, the reality remains that its total cloud revenues of $6.2 billion are dwarfed by AWS' $29.3 billion quarterly revenues. Oracle's infrastructure scale limitations are evident as the company struggles to meet demand, with executives repeatedly citing "capacity constraints" as hurdles to faster growth. Despite adding its 101st cloud region, Oracle lacks the global reach and availability zones that Amazon offers.

The company's strategic focus appears scattered across multiple fronts — healthcare partnerships, financial services products, and government initiatives — without the coherent vision that Amazon demonstrates. Oracle's heavy reliance on its database business makes it vulnerable to cloud-native alternatives and multi-cloud strategies that bypass Oracle's traditionally high-margin offerings.

Though Oracle highlights its Remaining Performance Obligations (RPO) growing 63% to $130 billion, skepticism exists around conversion rates and timing. The company's guidance for 15% revenue growth in fiscal 2026 seems ambitious given its consistent execution issues and history of overpromising. Oracle's AI strategy centers around its database offerings rather than providing the comprehensive AI ecosystem that AWS delivers.

The consensus mark for fiscal 2025 earnings is pegged at $6.03 per share, down 0.3% over the past 60 days.

Oracle Corporation price-consensus-chart | Oracle Corporation Quote

Despite management's claims about cost advantages for AI workloads, Oracle lacks the semiconductor investments and specialized infrastructure that Amazon has built. The company's relatively modest $16 billion annual CapEx pales in comparison to Amazon's infrastructure investments, raising questions about Oracle's ability to compete at scale in the capital-intensive cloud and AI markets.

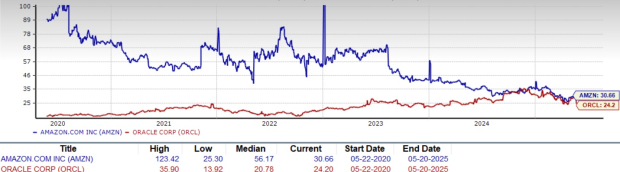

Both companies trade at premium valuations, but Amazon offers superior value considering its growth prospects. Amazon's forward P/E of approximately 30.66x is justified by its diversified revenue streams, market leadership in multiple high-growth sectors, and consistent ability to exceed earnings expectations. Oracle's forward P/E of 24.2x appears superficially cheaper but represents a questionable value given its slower growth and execution challenges.

Amazon's recent price performance reflects investor confidence, with shares climbing 3.5% year in the past 6-month period, outperforming Oracle which declined 16.6%. Oracle's relative valuation discount reflects legitimate concerns about its competitive position and ability to capitalize on the AI revolution at scale.

Amazon's enterprise value to free cash flow ratio provides a more compelling investment case, especially considering the company's proven ability to reinvest cash flows into high-return initiatives. While both companies offer cloud exposure, Amazon's diversification and scale provide a significantly more attractive risk-adjusted return profile than Oracle's narrower focus and smaller operational footprint.

Amazon emerges as the decidedly stronger investment opportunity in the cloud and AI race. Its superior scale, comprehensive AI capabilities, diversified revenue streams, and consistent execution provide a compelling foundation for long-term growth. While Oracle attempts to position itself as a specialized alternative, its smaller scale, execution missteps, and fragmented strategy make it a distant second in the cloud wars. Investors seeking exposure to the transformative potential of cloud computing and artificial intelligence would be better served by adding Amazon shares to their portfolios while reducing or avoiding Oracle positions. Amazon's demonstrated ability to continuously reinvent itself and its leadership position in multiple high-growth markets give it unmatched potential for sustained outperformance. AMZN currently carries a Zacks Rank #3 (Hold), whereas ORCL has a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 10 min | |

| 22 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 5 hours | |

| Apr-09 | |

| Apr-09 | |

| Apr-09 | |

| Apr-09 | |

| Apr-09 | |

| Apr-09 | |

| Apr-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite