|

|

|

|

|||||

|

|

|

Adobe ADBE shares have jumped 19% in a month, reflecting its deepening Generative AI (Gen AI) focus and innovative Gen AI-powered portfolio. A pause in tariffs that reduced macroeconomic uncertainty also helped the stock. However, Adobe’s near-term prospects remain challenging given stiff competition in the AI and GenAI space from the likes of Microsoft MSFT-backed OpenAI, as well as a lack of monetization of its AI solutions.

Adobe’s AI business is minuscule compared with the likes of Microsoft and Alphabet GOOGL. Microsoft’s Intelligent Cloud revenues are benefiting from growth in Azure AI services and a rise in AI Copilot business. Alphabet’s Google Cloud is benefiting from accelerated growth across AI infrastructure, enterprise AI platform Vertex and strong adoption of Gen AI solutions.

Stiff competition has negatively impacted Adobe shares, which have underperformed peers like Microsoft and document services & e-signature provider DocuSign DOCU over the past month, but outperformed Alphabet. Microsoft, DocuSign and Alphabet shares returned 24.9%, 20.9% and 8.2%, respectively, over the same timeframe. The challenging near-term prospect is expected to remain an overhang on the Adobe shares.

Adobe shares are also overvalued, as suggested by a Value Score of D.

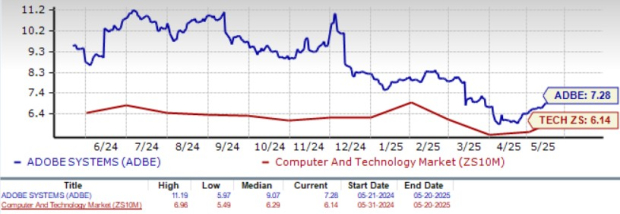

ADBE stock is trading at a premium with a forward 12-month price/sales of 7.28X compared with the broader Zacks Computer and Technology sector’s 6.14X, Salesforce’s 6.61X, DocuSign’s 5.69X and Alphabet’s 5.90X.

So, what should investors do with Adobe shares right now? Let’s dig deep to find out.

Adobe has expanded its AI portfolio with Adobe GenStudio and Firefly Services, which help brands and their agency partners collaborate on marketing campaigns. Adobe launched Firefly Video Model-powered Generative Extend in Premiere Pro, which leverages AI to instantly generate and expand the length of video and audio clips. Adobe introduced a new version of After Effects with a high-performance preview playback engine, powerful new 3D motion design tools and HDR monitoring. New Frame.io V4 upgrades include expanded storage that scales with teams.

Adobe plans to monetize standalone subscriptions for Firefly through the introduction of multiple Creative Cloud offerings that include Firefly tiering. Adobe plans to invest in its sales capacity to deliver Adobe-wide offerings across business, education and government. The integration of AI Assistant in Acrobat, Reader and Express bodes well for Adobe’s prospects. ADBE is infusing Gen AI innovations across its portfolio, including AI-first standalone and add-on products such as Acrobat AI Assistant, Firefly App and Services, and GenStudio for Performance Marketing. These factors are expected to boost top-line growth.

Adobe’s new AI book of business (more than $125 million exiting the first quarter of fiscal 2025) was a roughly low single-digit percentage of total revenues ($4.23 billion in the fiscal first quarter). ADBE expects this AI book of business to double by the end of fiscal 2025.

For fiscal 2025, Digital Media Annual Recurring Revenue is now expected to grow roughly 11%. Digital Media segment revenues are expected to be between $17.25 billion and $17.40 billion. Digital Experience segment revenues are expected between $5.8 billion and $5.9 billion, while Digital Experience subscription segment revenues are expected between $5.375 billion and $5.425 billion.

Adobe reaffirmed its total revenue guidance, which is expected between $23.30 billion and $23.55 billion ($21.51 billion in fiscal 2024). Fiscal 2025 non-GAAP earnings are still expected between $20.20 and $20.50 ($18.42 per share in fiscal 2024).

For fiscal 2025, the Zacks Consensus Estimate for earnings is pegged at $20.36 per share, down by 5 cents over the past 60 days. The figure indicates 10.53% growth over fiscal 2024.

Adobe Inc. price-consensus-chart | Adobe Inc. Quote

The Zacks Consensus Estimate for second-quarter fiscal 2025 earnings is pegged at $4.96 per share, down by a penny over the past 60 days, suggesting 10.71% growth from the year-ago quarter.

ADBE’s earnings beat the Zacks Consensus Estimate in all the trailing four quarters, the average surprise being 2.53%.

Adobe’s modest near-term growth prospect and stretched valuation makes the stock unattractive for investors.

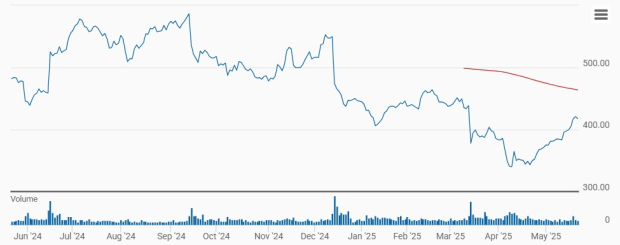

The stock is currently trading below the 200-day moving average, indicating a bearish trend.

ADBE currently has a Zacks Rank #4 (Sell), which implies that investors should avoid the stock for the time being.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 8 min | |

| 12 min | |

| 57 min | |

| 58 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite