|

|

|

|

|||||

|

|

|

NVIDIA Corporation NVDA is set to report first-quarter fiscal 2026 results on May 28.

The company expects revenues of $43 billion (+/-2%) for the quarter. The Zacks Consensus Estimate is pegged at $42.71 billion, which indicates a whopping 64% increase from the year-ago reported figure.

The Zacks Consensus Estimate for quarterly earnings has moved down a penny to 87 cents per share over the past 30 days. This suggests year-over-year growth of 42.6% from the year-ago quarter’s earnings of 61 cents per share.

Earnings of the pioneer in graphics processing unit (GPU)-accelerated computing surpassed the Zacks Consensus Estimate in each of the trailing four quarters, the average surprise being 7.9%. (Find the latest EPS estimates and surprises on Zacks Earnings Calendar.)

NVIDIA Corporation price-eps-surprise | NVIDIA Corporation Quote

Our proven model does not conclusively predict an earnings beat for NVIDIA this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat, which is not the case here. You can see the complete list of today’s Zacks #1 Rank stocks here.

Though NVIDIA carries a Zacks Rank #3, it has an Earnings ESP of -5.24%. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

NVIDIA’s first-quarter top line is likely to have benefited from the continued strength in its Datacenter business. The increasing adoption of cloud-based solutions amid the growing hybrid working trend is anticipated to have boosted demand for its chips across the datacenter end market. An increase in hyperscale demand and growing adoption in the inference market are likely to have acted as tailwinds in the to-be-reported quarter.

The Datacenter end-market business is likely to have benefited from the growing demand for generative AI and large language models using GPUs based on NVIDIA Hopper and Ampere architectures. The strong demand for its chips from large cloud service and consumer internet companies is anticipated to have aided the segment’s top-line growth in the to-be-reported quarter. Our first-quarter revenue estimate for the Datacenter end market is pegged at $38.5 billion, which indicates robust year-over-year growth of 70.6%.

Moreover, NVIDIA’s first-quarter performance is likely to have benefited from the recovery across its Gaming and Professional Visualization end markets. The Gaming end market’s results have improved year over year in six out of the last seven quarters, as inventory levels with channel partners have returned to normal. The company also registered strong demand across most regions for its gaming products. Our first-quarter revenue estimate for the Gaming end market is pegged at $3.29 billion, which implies a 24.4% increase from the year-ago quarter’s level.

NVIDIA’s Professional Visualization segment performance also reflected recovery, with revenues increasing in six consecutive quarters. The trend is likely to have continued in the first quarter. Our first-quarter revenue estimate for the Professional Visualization end market is pegged at $567.6 million, which suggests a 32.9% increase from the year-ago quarter’s figure.

The company’s Automotive segment demonstrated an improvement in trends over the preceding four quarters. The positive trend is likely to have continued in the fiscal first quarter due to increasing investments in self-driving and AI cockpit solutions. Our revenue estimate for the Automotive end market is pegged at $551.7 million, which indicates year-over-year growth of 67.7%.

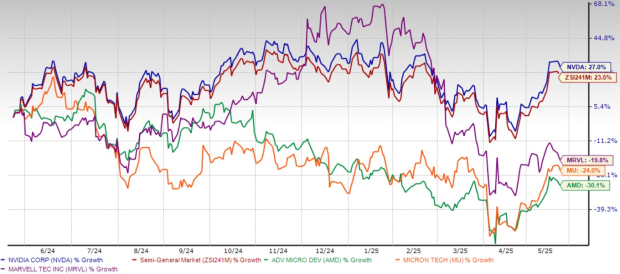

Shares of NVIDIA have remained highly volatile over the past year. NVDA stock has gained 27% over the past year, outperforming the Zacks Semiconductor – General industry’s growth of 23.5%. The stock has also outperformed major semiconductor stocks, including Advanced Micro Devices AMD, Micron Technology MU and Marvell Technology MRVL. Shares of Advanced Micro Devices, Micron Technology and Marvell Technology have lost 30.1%, 24% and 19.8%, respectively.

Now, let’s look at the value NVIDIA offers investors at the current levels. NVIDIA is trading at a premium with a forward 12-month P/S of 15.48X compared with the industry’s 13.26X, reflecting a stretched valuation.

NVDA also trades at a premium compared with other semiconductor players, including Advanced Micro Devices, Micron Technology and Marvell Technology. Currently, Advanced Micro Devices, Micron Technology and Marvell Technology trade at a forward P/S multiples of 5.37X, 2.48X and 5.94X, respectively.

Over the past year, NVIDIA’s revenue growth has been driven by robust demand for chips required for the development of generative AI models. NVIDIA dominates the market for generative AI chips, which have already proven useful across multiple industries, including marketing, advertising, customer service, education, content creation, healthcare, automotive, energy & utilities and video game development.

The growing demand to modernize the workflow across industries is expected to drive the demand for generative AI applications. The global generative AI market size is anticipated to reach $967.6 billion by 2032, according to a new report by Fortune Business Insights. The market is expected to witness a CAGR of 39.6% from 2024 to 2032.

However, the complexity of generative AI, which requires vast knowledge and immense computational power, means that enterprises will need to significantly upgrade their network infrastructures. NVIDIA’s AI chips, including the A100, H100 and B100, are the top choices for building and running these powerful AI applications, positioning the company as a leader in this space. As the generative AI revolution unfolds, we expect NVIDIA's advanced chips to drive substantial growth in both its revenues and market presence.

As a leading player in the semiconductor industry, NVIDIA has benefited from its dominance in GPUs and strategic expansion into AI, data centers and autonomous vehicles. The company's strong product portfolio, leadership in AI and relentless innovation present a compelling investment opportunity.

However, its high valuation makes it vulnerable to short-term volatility. For now, holding the stock is the smartest approach.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 24 min | |

| 25 min | |

| 55 min |

Trump Says Khamenei Killed In U.S.-Israeli Attacks. How Will Dow Jones Futures React?

MU

Investor's Business Daily

|

| 1 hour | |

| 1 hour | |

| 3 hours |

Trump Says Khamenei Likely Killed In U.S.-Israeli Attacks On Iran. How Will Dow Jones Futures React?

MU

Investor's Business Daily

|

| 3 hours | |

| 3 hours | |

| 4 hours | |

| 6 hours | |

| 7 hours | |

| 7 hours | |

| 7 hours | |

| 7 hours | |

| 9 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite