|

|

|

|

|||||

|

|

|

Potbelly has been treading water for the past six months, recording a small return of 1.4% while holding steady at $10.35.

Is there a buying opportunity in Potbelly, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

We're swiping left on Potbelly for now. Here are three reasons why there are better opportunities than PBPB and a stock we'd rather own.

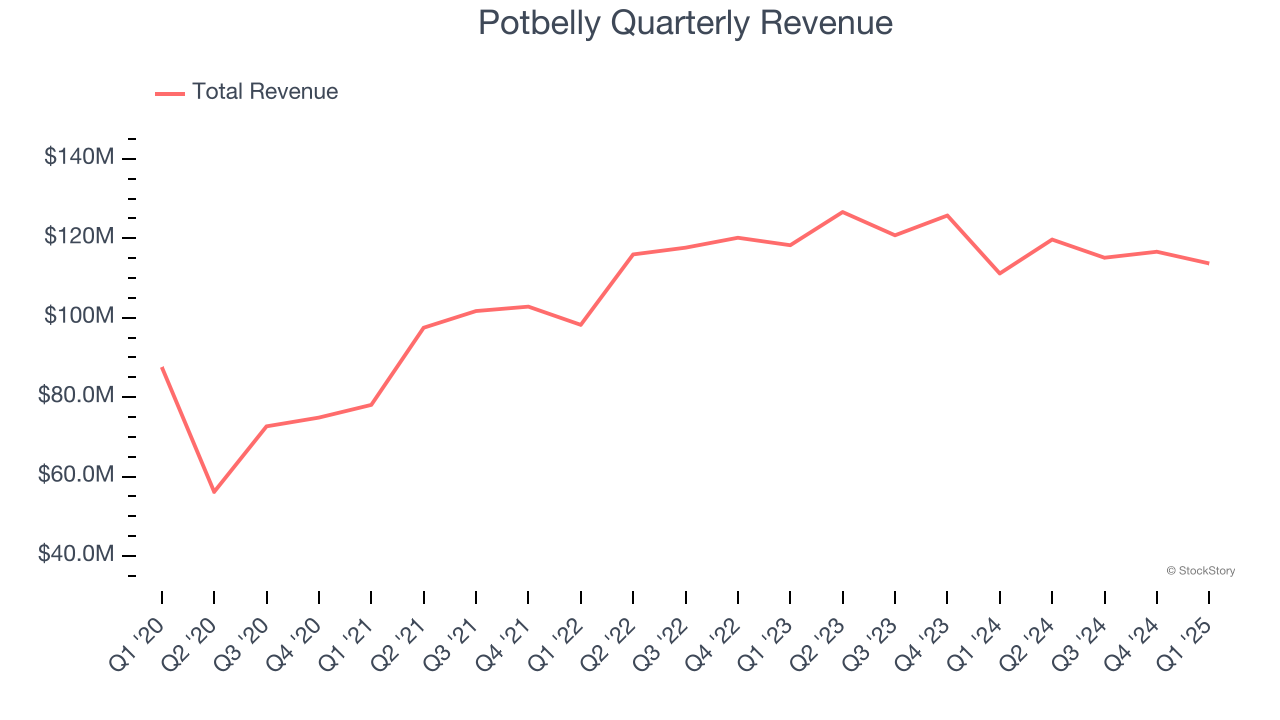

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Regrettably, Potbelly’s sales grew at a weak 1.8% compounded annual growth rate over the last six years. This fell short of our benchmarks.

With $465.1 million in revenue over the past 12 months, Potbelly is a small restaurant chain, which sometimes brings disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale.

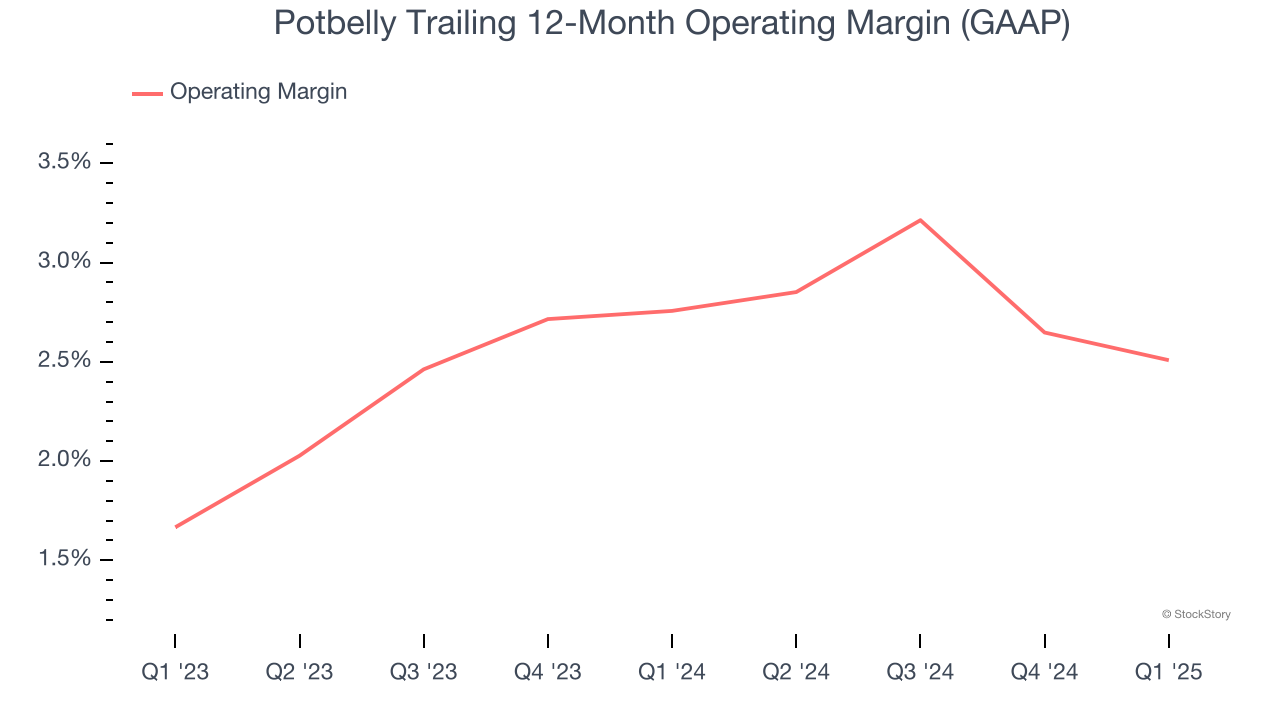

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Potbelly was profitable over the last two years but held back by its large cost base. Its average operating margin of 2.6% was weak for a restaurant business. This result is surprising given its high gross margin as a starting point.

Potbelly’s business quality ultimately falls short of our standards. That said, the stock currently trades at 10.2× forward EV-to-EBITDA (or $10.35 per share). Investors with a higher risk tolerance might like the company, but we think the potential downside is too great. We're fairly confident there are better stocks to buy right now. We’d recommend looking at a fast-growing restaurant franchise with an A+ ranch dressing sauce.

Market indices reached historic highs following Donald Trump’s presidential victory in November 2024, but the outlook for 2025 is clouded by new trade policies that could impact business confidence and growth.

While this has caused many investors to adopt a "fearful" wait-and-see approach, we’re leaning into our best ideas that can grow regardless of the political or macroeconomic climate. Take advantage of Mr. Market by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 176% over the last five years.

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

| Oct-27 |

Potbelly promotes Adam Noyes to president

Nation's Restaurant News

|

| Oct-24 |

Potbelly promotes COO to president following RaceTrac buyout

Restaurant Dive

|

| Oct-14 |

3 High-Flying Stocks We're Skeptical Of

StockStory

|

| Oct-13 |

Heartland Value Fund's Views on Potbelly (PBPB)

Insider Monkey

|

| Oct-03 |

3 Stocks Under $50 That Fall Short

StockStory

|

| Oct-02 | |

| Sep-19 | |

| Sep-17 | |

| Sep-14 | |

| Sep-12 |

RaceTrac agrees to acquire sandwich chain Potbelly for $566m

Verdict Food Service

|

| Sep-12 | |

| Sep-11 | |

| Sep-11 |

RaceTrac fills a key gap with Potbelly acquisition

C-Store Dive

|

| Sep-10 | |

| Sep-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite