|

|

|

|

|||||

|

|

|

ResMed Inc.’s RMD growth in the third quarter of fiscal 2025 can be attributed to the robust performance of its Mask business. Its progress in digital health technology continues to drive overall revenue growth. However, a dull macroeconomic scenario and fierce competition put pressure on ResMed’s operations.

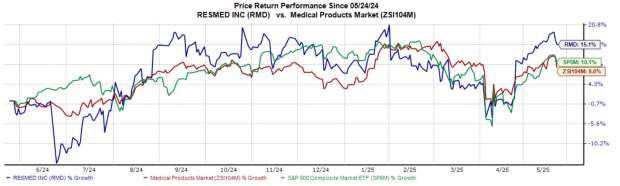

In the past year, shares of this Zacks Rank #3 (Buy) company have surged 15.1%, outperforming the industry’s 8.6% growth and the S&P 500 composite’s 10.1% rise.

The renowned medical device company has a market capitalization of $36.00 billion. RMD has an earnings yield of 3.9%, outpacing the industry’s 0.5%. The company’s earnings surpassed estimates in each of the trailing four quarters, delivering an average surprise of 4.23%.

Let’s delve deeper.

Robust Mask Sales: Resmed continues to see strong demand for its market-leading mask portfolio, gaining from a competitor’s recall. Continued product development is driving growth within this business globally. The company has successfully introduced a full suite of masks in its AirFit, AirTouch and other ranges. Further, to promote greater patient adherence, Resmed offers advanced and expanded integrations of its therapy-based software solutions, including AirView.

The company’s AirFit F40 is performing extremely well in the U.S. market. It expects to expand the AirFit F40's availability across additional global markets. In the previous quarter, Resmed launched AirTouch N30i, the world’s first unique fabric-based patient interface, in selected markets. Early feedback for AirTouch N30i is a positive.

During the fiscal third quarter, revenues from Masks and other businesses grew 11% year over year globally, including an increase of 13% in the United States, Canada and Latin America. In line with this, masks and accessories’ double-digit growth was augmented by the ongoing rollout of ReSupply program and new patient setups. Additionally, Resmed witnessed top-line growth of 7% in Europe, Asia and other regions combined.

Potential in Digital Health: ResMed is progressing across several digital health technology initiatives to further increase the value proposition for its connected healthcare ecosystem. The company’s two key global customer-facing software products — AirView and myAir — are 100% in the cloud.

Currently, Resmed is investing in a portfolio of artificial intelligence-driven capabilities, as well as customer-facing AI products in its ecosystem. The company has continued to roll out these products in its AirView ecosystem, such as Compliance Coach in the United States. These AI-driven data products will provide personalized suggestions to increase patient therapy adherence and ultimately improve patient outcomes. Resmed is pleased to see that the early testing feedback in both customer groups has been positive.

Challenging Macroeconomic Scenario: Global macroeconomic conditions, primarily headwinds arising from the Middle East conflict, are denting growth. Further, fluctuations in foreign currency exchange rates and volatility in capital markets could continue to affect Resmed’s results of operations. Furthermore, with the sustained inflationary pressures in the future, the company may struggle to keep its operating expenses, as a percentage of net revenue, in check. These factors might dent Resmed’s profitability. SG&A expenses rose 6.7% year over year. R&D expenses increased 8.9%.

Competitive Landscape: The market for sleep-disordered breathing (SDB) products is highly competitive with respect to product price, features and reliability. The disparity between the company's resources and those of its competitors may increase due to consolidation in the healthcare industry. Moreover, some of Resmed's competitors are affiliates of its customers, which may make it difficult for the company to compete with them.

The Zacks Consensus Estimate for fiscal 2025 earnings has moved north 0.3% to $9.48 per share in the past 30 days.

The consensus estimate for fiscal 2025 revenues is pegged at $5.12 billion, which indicates a 9.3% increase from the year-ago reported number.

Some better-ranked stocks in the broader medical space that have announced quarterly results are Integer Holdings Corporation ITGR, AngioDynamics ANGO and CVS Health Corporation CVS.

Integer Holdings has a long-term estimated growth rate of 18.4%. ITGR’s earnings surpassed estimates in three of the trailing four quarters and missed once, the average surprise being 2.8%. Its shares have surged 1.1% compared to the industry’s 13.4% decline over the past year.

ITGR currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

AngioDynamics, currently sporting a Zacks Rank #1, has an estimated fiscal 2026 earnings growth rate of 27.8% compared with the S&P 500 composite’s 10.5%. The company surpassed earnings estimates in each of the trailing four quarters, the average surprise being 70.9%. Shares of the company have rallied 63.9% against the industry’s 13.4% decline.

CVS Health, carrying a Zacks Rank of 2 (Buy) at present, has a long-term estimated growth rate of 11.4%. CVS’ earnings surpassed estimates in each of the trailing four quarters, delivering an average surprise of 18.1%. Shares of the company have rallied 11.1% against the industry’s 19.4% decline.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Mar-24 | |

| Mar-24 | |

| Mar-19 | |

| Mar-18 | |

| Mar-18 | |

| Mar-16 | |

| Mar-12 | |

| Mar-12 | |

| Mar-12 | |

| Mar-12 | |

| Mar-12 | |

| Mar-11 | |

| Mar-11 | |

| Mar-11 |

CVS Health's Aetna to Pay $117.7 Million to Resolve False Claims Act Allegations

CVS

The Wall Street Journal

|

| Mar-11 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about Finviz Elite