|

|

|

|

|||||

|

|

|

SentinelOne S is scheduled to report first-quarter fiscal 2026 results (ended April 30, 2025) on May 28, after the closing bell.

SentinelOne closed fiscal 2025 with a strong fourth quarter that exceeded expectations across revenues, margin, earnings per share (EPS) and customer growth. Revenue rose 29% year over year to $225.5 million, beating the Zacks Consensus Estimate by 1.6% and underscoring the company’s competitive strength in an increasingly crowded cybersecurity market.

Notably, net new Annual Recurring Revenue (“ARR”) came in at $60 million, taking total ARR to $920 million, up 27% year over year. International revenue surged 36% and represented 37% of total quarterly revenues, reflecting robust global traction. Gross margin in the fiscal fourth quarter was strong, and operating margin beat guidance by over 400 basis points (bps) thanks to disciplined cost management. EPS came in at 4 cents against 2 cents loss a year ago.

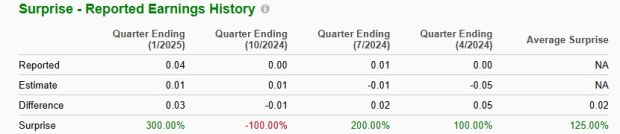

This key player in endpoint security—leveraging AI-driven tools to protect network-connected devices across a wide cybersecurity platform — surpassed earnings estimates in three of the trailing four quarters and missed on one, with an average surprise of 125%. You can see the historical figures in the chart below.

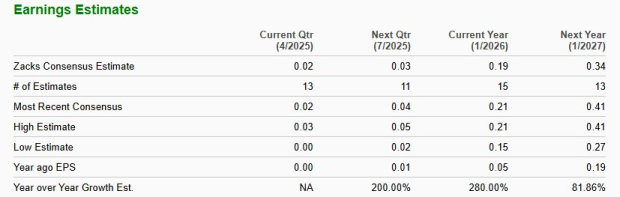

The Zacks Consensus Estimate for fiscal first-quarter earnings per share (EPS) has remained unchanged at 2 cents per share over the past 60 days. In the year-ago period, the company reported break-even earnings. The consensus mark for revenues is pinned at $228 million, suggesting 22.4% year-over-year growth.

For fiscal 2026, SentinelOne is expected to witness 22.7% revenue growth from the fiscal 2025 level. The company is expected to register a 280% year-over-year improvement in the bottom line for this year.

Our proven model does not conclusively predict an earnings beat for SentinelOne this reporting cycle. That is because a stock needs to have both a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy), or 3 (Hold) for this to happen. This is not the case here, as you will see below.

Earnings ESP: SentinelOne has an Earnings ESP of 0.00%. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Zacks Rank: The company currently carries a Zacks Rank #3.

You can see the complete list of today’s Zacks #1 Rank stocks here.

SentinelOne’s expanding adoption of AI-driven solutions like Purple AI and AI SIEM, which fueled over 300 deals in the fiscal fourth quarter, is expected to have contributed to the company’s quarterly results. Platform traction remains a bright spot, with more than 40% of large enterprise customers now adopting three or more Singularity platform modules. Strategic wins in cloud and data security, along with deepening MSSP partnerships, support the company’s broader go-to-market shift beyond endpoint protection.

SentinelOne expects fiscal first-quarter revenues of approximately $228 million, up 22% year over year. Net new ARR is expected in the low $30 million range, with near-term pressure from the retirement of its legacy deception solution, which accounts for about $5 million in expected churn this quarter. While the move reflects the company’s shift toward higher-margin, AI-driven solutions, it will temporarily weigh on ARR growth and net retention.

SentinelOne’s fiscal first-quarter operating margin is expected to land near negative 2%, reflecting seasonal expense patterns and continued platform investments. Gross margin is projected to remain strong at around 79%, supported by software scale and cloud leverage. The company’s focus remains on maintaining margin improvement while driving platform expansion.

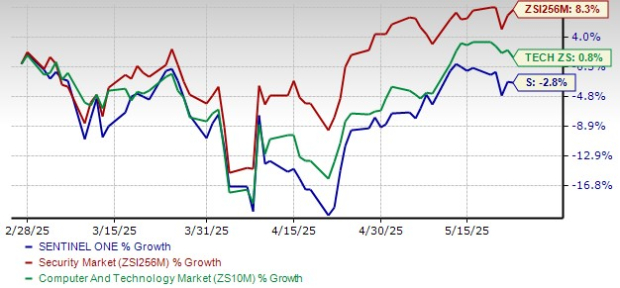

SentinelOne shares have lost 2.8% over the past three months, underperforming both the Zacks Security industry's 8.3% rise and the broader Zacks Computer & Technology sector's 0.8% growth.

SentinelOne has underperformed industry peers, including Okta OKTA and CrowdStrike CRWD, but performed better than Fortinet FTNT over the same timeframe. Okta and CrowdStrike shares have appreciated 38.7% and 19.8%, respectively. However, Fortinet shares have lost 3.7% over the same three-month period.

At its current price, the S stock represents a 32.5% discount from its 52-week high of $29.29. It also indicates a 37.9% premium to its 52-week low of $14.33.

From a valuation standpoint, the company is currently trading at a slight premium relative to its sector. In terms of the forward 12-month price-to-sales (P/S) ratio, SentinelOne is trading at 6.04X, higher than the sector’s 6.12X. Its forward 12-month P/S ratio sits below its three-year average, as shown below.

As SentinelOne prepares to report its fiscal first-quarter results, the company stands at a strategic inflection point, balancing near-term growth moderation with long-term platform and AI-driven upside. The expected revenue of $228 million, up 22% year over year, and a low $30 million range in net new ARR suggest a stable start to the year, albeit tempered by $5 million in planned churn tied to the retirement of its legacy deception solution. While this may weigh on reported metrics, the move reflects a deliberate shift toward higher-value, AI-native offerings and streamlined operations.

What distinguishes SentinelOne is its sustained momentum in expanding platform adoption. With more than 40% of enterprise customers now using three or more solution categories and more than 300 AI-related deals signed in the prior quarter, the company is demonstrating strong cross-sell traction and customer engagement. Key growth vectors, such as AI SIEM, cloud security, and Purple AI, are seeing accelerated uptake, positioning SentinelOne as a differentiated leader in the evolving cybersecurity landscape.

Despite macroeconomic uncertainty, SentinelOne’s solid gross margins, improving operating efficiency, and growing presence in enterprise and MSSP channels offer encouraging signs of durable growth. The company’s path toward surpassing $1 billion in revenues and ARR this fiscal year remains intact, supported by innovation, expanding use cases, and operational discipline.

In sum, while near-term headwinds may modestly affect fiscal first-quarter growth, SentinelOne’s long-term investment case remains compelling. Continued platform adoption, strong AI differentiation, and an improving margin profile position the company well for scalable, profitable expansion in fiscal 2026 and beyond.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 7 hours | |

| 9 hours | |

| 10 hours | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 | |

| Feb-27 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite