|

|

|

|

|||||

|

|

|

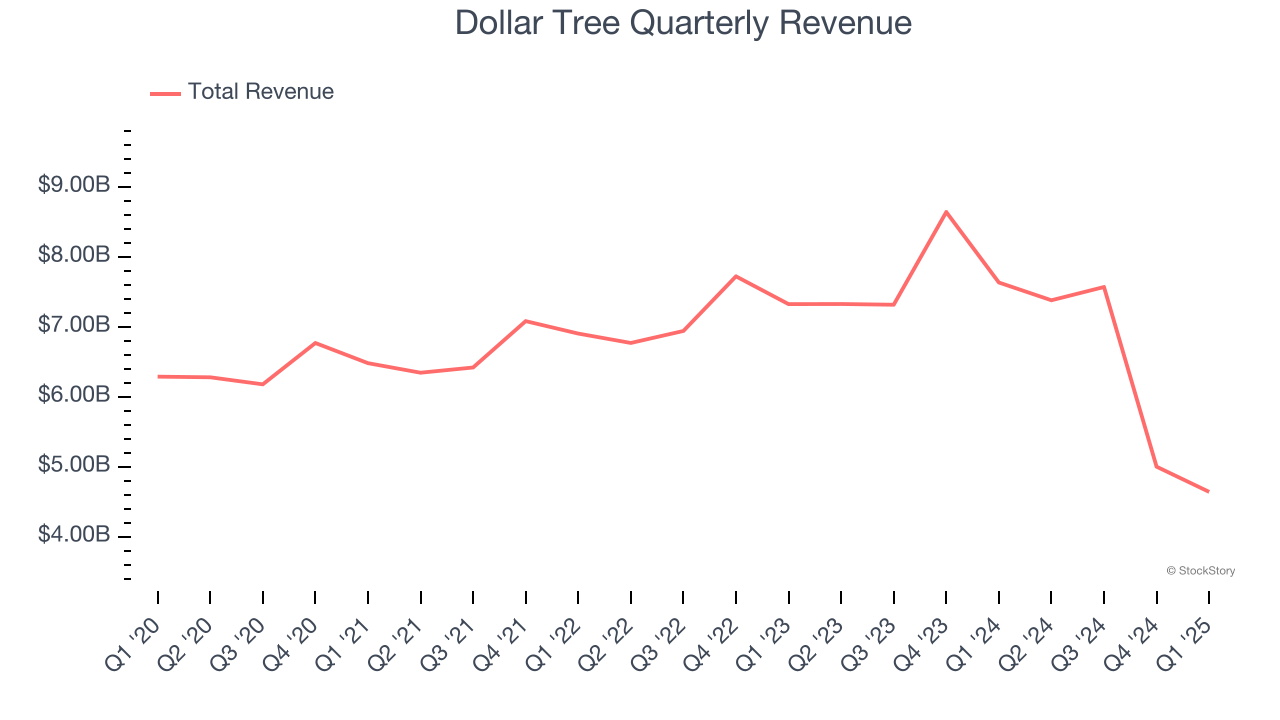

Discount treasure-hunt retailer Dollar Tree (NASDAQ:DLTR) reported revenue ahead of Wall Street’s expectations in Q1 CY2025, but sales fell by 39.2% year on year to $4.64 billion. The company expects next quarter’s revenue to be around $7.67 billion, coming in 74.6% above analysts’ estimates. Its non-GAAP profit of $1.26 per share was 4.5% above analysts’ consensus estimates.

Is now the time to buy Dollar Tree? Find out by accessing our full research report, it’s free.

“Our strong first quarter performance underscores the progress we’ve made against our strategic priorities and is a clear signal that our customers are responding positively to the changes we are making,” said Mike Creedon, Chief Executive Officer.

A treasure hunt because there’s no guarantee of consistent product selection, Dollar Tree (NASDAQ:DLTR) is a discount retailer that sells general merchandise and select packaged food at extremely low prices.

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $24.59 billion in revenue over the past 12 months, Dollar Tree is one of the larger companies in the consumer retail industry and benefits from a well-known brand that influences purchasing decisions. However, its scale is a double-edged sword because there is only so much real estate to build new stores, placing a ceiling on its growth. To accelerate sales, Dollar Tree likely needs to optimize its pricing or lean into international expansion.

As you can see below, Dollar Tree grew its sales at a sluggish 1.1% compounded annual growth rate over the last six years (we compare to 2019 to normalize for COVID-19 impacts) as its store footprint remained unchanged.

This quarter, Dollar Tree’s revenue fell by 39.2% year on year to $4.64 billion but beat Wall Street’s estimates by 2.4%. Company management is currently guiding for a 4% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to decline by 21.7% over the next 12 months, a deceleration versus the last six years. This projection is underwhelming and indicates its products will see some demand headwinds.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

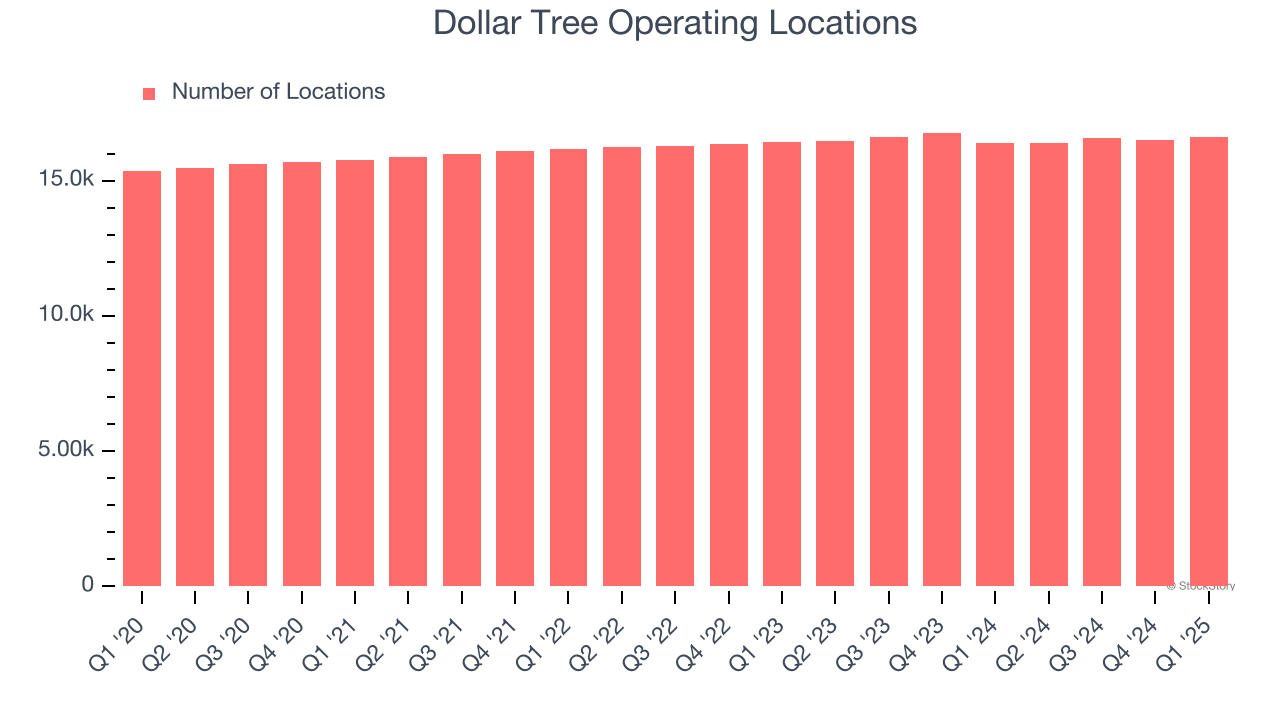

A retailer’s store count influences how much it can sell and how quickly revenue can grow.

Dollar Tree listed 16,607 locations in the latest quarter and has kept its store count flat over the last two years while other consumer retail businesses have opted for growth.

When a retailer keeps its store footprint steady, it usually means demand is stable and it’s focusing on operational efficiency to increase profitability.

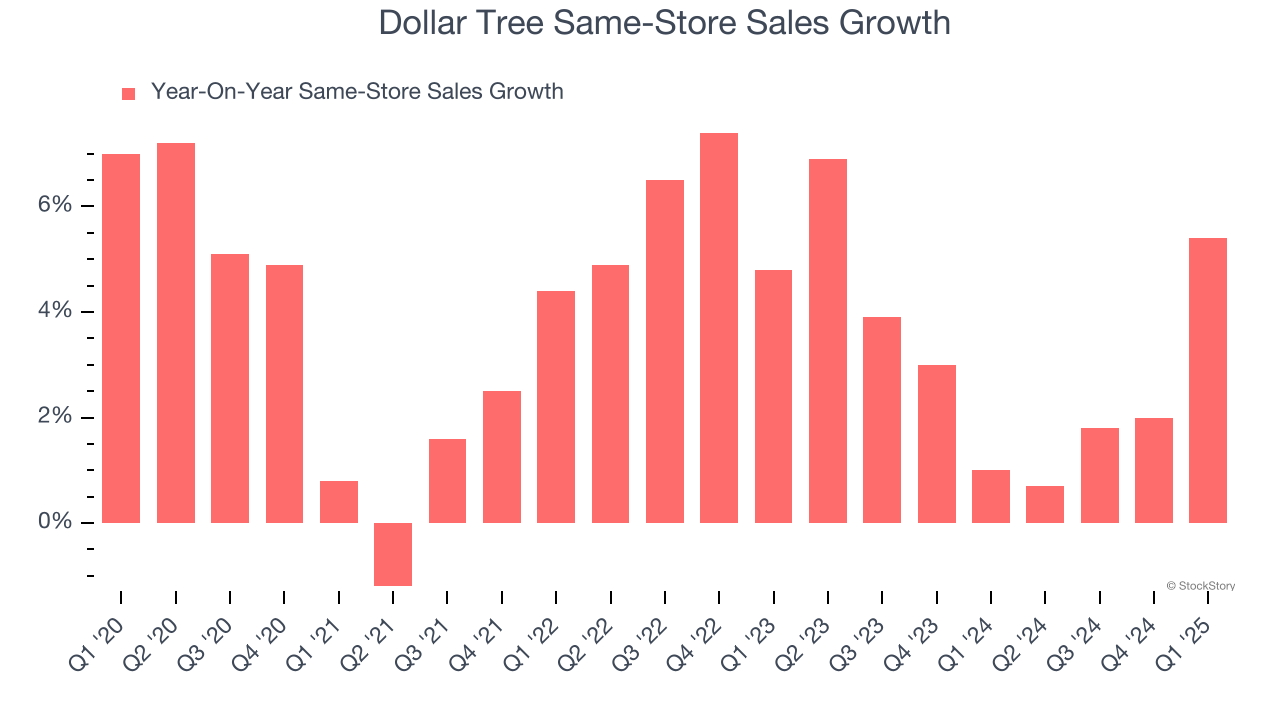

The change in a company's store base only tells one side of the story. The other is the performance of its existing locations and e-commerce sales, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales is an industry measure of whether revenue is growing at those existing stores and is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Dollar Tree’s demand has been healthy for a retailer over the last two years. On average, the company has grown its same-store sales by a robust 3.1% per year. Given its flat store base over the same period, this performance stems from not only increased foot traffic at existing locations but also higher e-commerce sales as demand shifts from in-store to online.

In the latest quarter, Dollar Tree’s same-store sales rose 5.4% year on year. This growth was an acceleration from its historical levels, which is always an encouraging sign.

It was great to see Dollar Tree raise its full-year EPS guidance and beat Wall Street’s revenue, EPS, and EBITDA estimates. On the other hand, its full-year revenue guidance slightly missed. Overall, we think this was a decent quarter with some key metrics above expectations. Investors were likely hoping for more, and shares traded down 2.8% to $93.94 immediately after reporting.

Big picture, is Dollar Tree a buy here and now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.

| Feb-24 | |

| Feb-23 | |

| Feb-21 | |

| Feb-20 | |

| Feb-20 | |

| Feb-20 | |

| Feb-18 | |

| Feb-18 | |

| Feb-18 | |

| Feb-17 | |

| Feb-17 | |

| Feb-16 | |

| Feb-16 | |

| Feb-16 | |

| Feb-15 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite