|

|

|

|

|||||

|

|

|

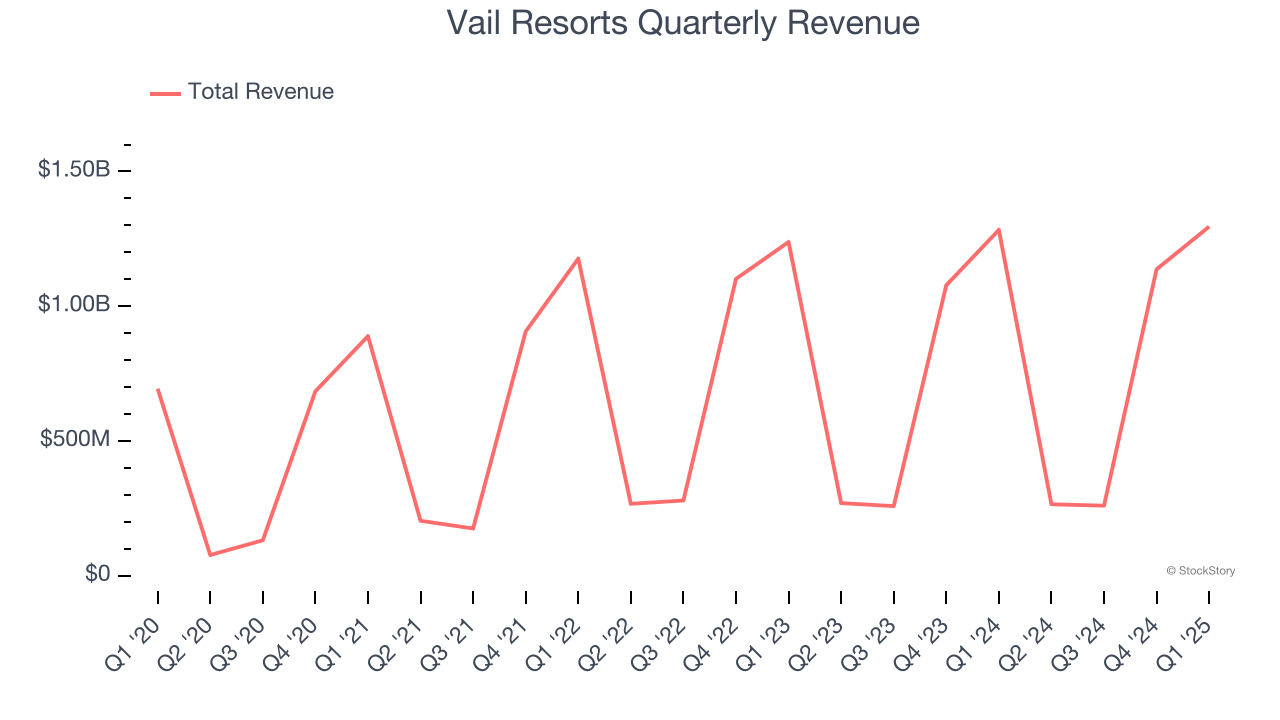

Luxury ski resort company Vail Resorts (NYSE:MTN) met Wall Street’s revenue expectations in Q1 CY2025, but sales were flat year on year at $1.30 billion. Its GAAP profit of $10.54 per share was 4.7% above analysts’ consensus estimates.

Is now the time to buy Vail Resorts? Find out by accessing our full research report, it’s free.

Commenting on the Company's fiscal 2025 third quarter results, Rob Katz, Chief Executive Officer, said, "Results in the quarter reflect the stability provided by our season pass program as Resort net revenue, excluding

Founded by two Aspen, Colorado ski patrol guides, Vail Resorts (NYSE:MTN) is a mountain resort company offering luxury experiences in over 30 locations across the globe.

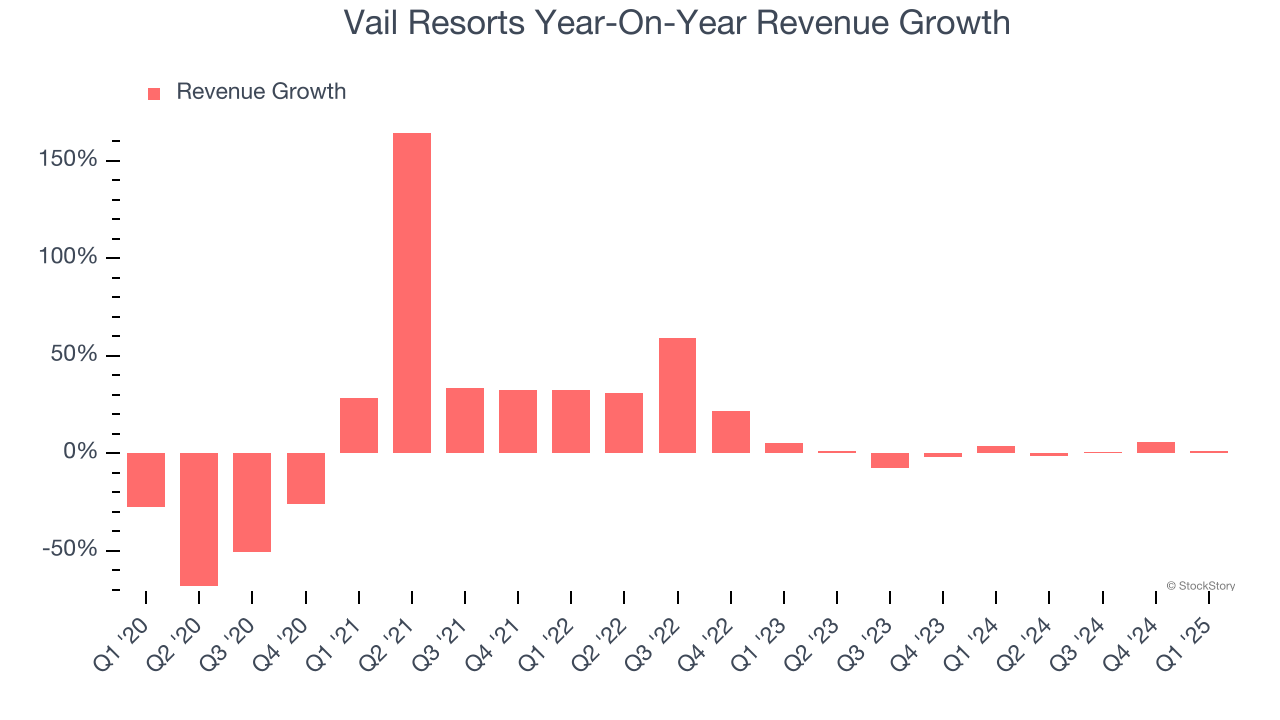

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Regrettably, Vail Resorts’s sales grew at a sluggish 6.8% compounded annual growth rate over the last five years. This was below our standard for the consumer discretionary sector and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Vail Resorts’s recent performance shows its demand has slowed as its annualized revenue growth of 1.2% over the last two years was below its five-year trend. Note that COVID hurt Vail Resorts’s business in 2020 and part of 2021, and it bounced back in a big way thereafter.

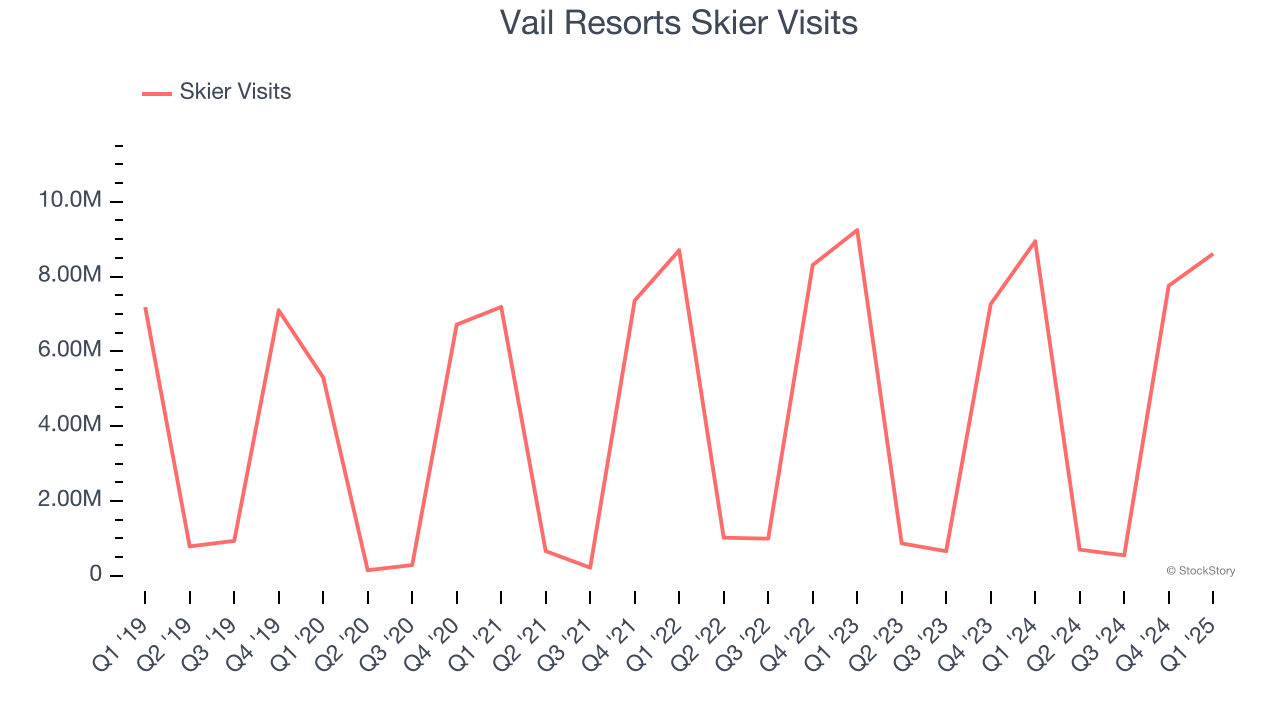

We can better understand the company’s revenue dynamics by analyzing its number of skier visits, which reached 8.61 million in the latest quarter. Over the last two years, Vail Resorts’s skier visits averaged 12.2% year-on-year declines. Because this number is lower than its revenue growth during the same period, we can see the company’s monetization has risen.

This quarter, Vail Resorts’s $1.30 billion of revenue was flat year on year and in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 4.2% over the next 12 months. While this projection suggests its newer products and services will fuel better top-line performance, it is still below the sector average.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

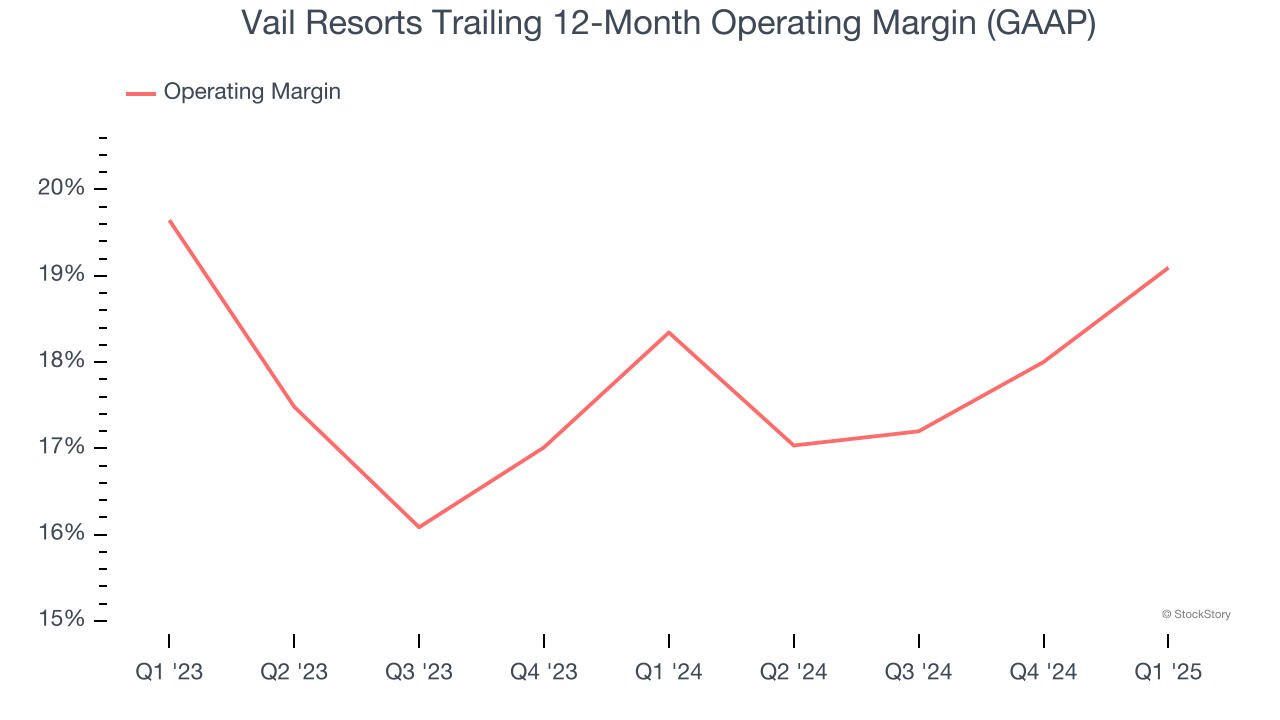

Vail Resorts’s operating margin might fluctuated slightly over the last 12 months but has generally stayed the same, averaging 18.7% over the last two years. This profitability was top-notch for a consumer discretionary business, showing it’s an well-run company with an efficient cost structure.

In Q1, Vail Resorts generated an operating margin profit margin of 44.9%, up 2.3 percentage points year on year. This increase was a welcome development and shows it was more efficient.

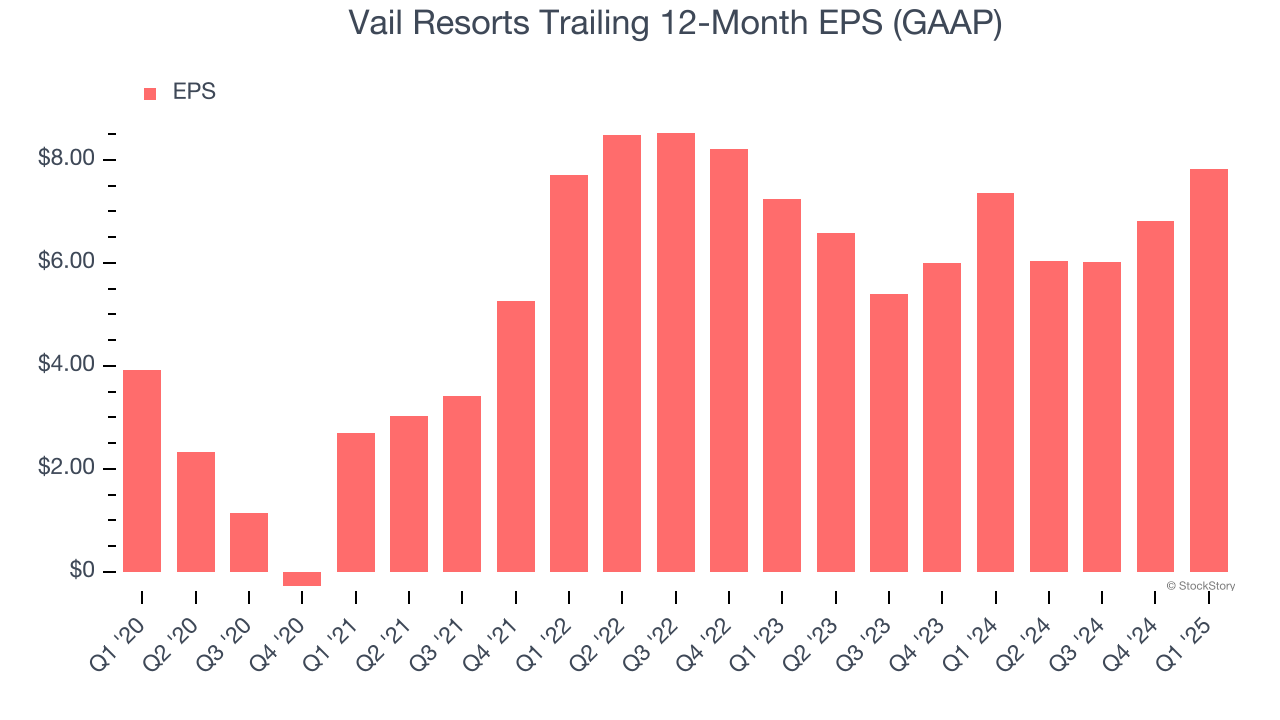

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Vail Resorts’s EPS grew at a solid 14.8% compounded annual growth rate over the last five years, higher than its 6.8% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

In Q1, Vail Resorts reported EPS at $10.54, up from $9.54 in the same quarter last year. This print beat analysts’ estimates by 4.7%. Over the next 12 months, Wall Street expects Vail Resorts’s full-year EPS of $7.82 to stay about the same.

It was encouraging to see Vail Resorts beat analysts’ EPS expectations this quarter. On the other hand, its number of skier visits missed. Zooming out, we think this was a mixed quarter. The stock traded up 1.6% to $157.59 immediately after reporting.

Big picture, is Vail Resorts a buy here and now? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.

| Feb-18 | |

| Feb-13 | |

| Feb-10 | |

| Feb-09 | |

| Feb-03 | |

| Jan-24 | |

| Jan-16 | |

| Jan-16 | |

| Jan-16 | |

| Jan-15 | |

| Jan-15 | |

| Jan-15 | |

| Jan-09 | |

| Jan-08 | |

| Jan-08 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite