|

|

|

|

|||||

|

|

|

Target Corporation’s TGT first-quarter fiscal 2025 gross margin rate of 28.2% was down 60 basis points year over year, but it could have been worse. The company reported about 120 basis points of gross margin benefit from reduced shrink, a notable reversal of the elevated losses seen during 2022 and 2023. This improvement helped offset pressures from higher markdowns and digital fulfillment costs.

The company clawed back most of the 120 basis points of shrink-related headwinds accumulated over prior years, with CFO Jim Lee noting the quarter included a “catch-up” component. This shrink improvement pushed operating income 13.6% higher year over year despite a 2.8% drop in net sales, underlining just how pivotal the benefit was. Management conceded that the bulk of the shrink recovery may have now played out, and the path forward may not provide the same level of margin uplift in subsequent quarters.

Shrink improvements have proven vital to cushioning against broader margin pressure, especially as comparable sales decline and discretionary demand remains weak. However, the sustainability of this benefit is limited. With ongoing margin pressures from digital fulfillment costs, tariff uncertainties and soft traffic, the durability of Target’s profitability hinges on more than shrink. Target will need to rely on other levers, such as merchandising mix, cost efficiencies or pricing strategies, to maintain or expand margins.

Dollar General Corporation DG continues to battle shrink-related challenges, though recent progress shows signs of traction. In the first quarter of fiscal 2025, Dollar General reported a 61-basis-point improvement in shrink, contributing to a 78-basis-point increase in the gross margin. While gains are encouraging, Dollar General acknowledged persistent cost pressures elsewhere. Still, shrink mitigation remains a crucial lever for Dollar General as it works to stabilize margins in a volatile consumer environment.

Ulta Beauty, Inc. ULTA is also leaning on shrink reduction to help protect margins in a tough retail environment. In the latest quarter, Ulta Beauty’s gross margin dipped slightly to 39.1% from 39.2% a year ago, with lower shrink partially offsetting pressure from fixed costs and weaker other revenues. Ulta Beauty continues to prioritize shrink management, making it a key lever as the company works to stabilize profitability.

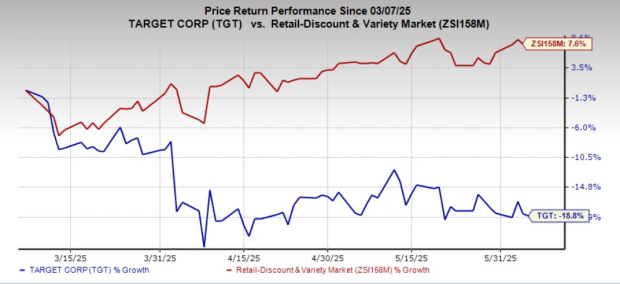

Target stock has declined 18.8% over the past three months against the industry’s growth of 7.6%.

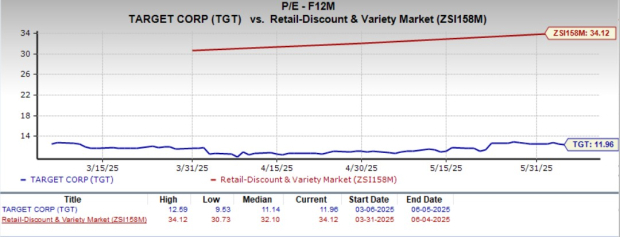

Target’s forward 12-month price-to-earnings ratio of 11.96 reflects a lower valuation compared to the industry’s average of 34.12X. TGT carries a Value Score of B.

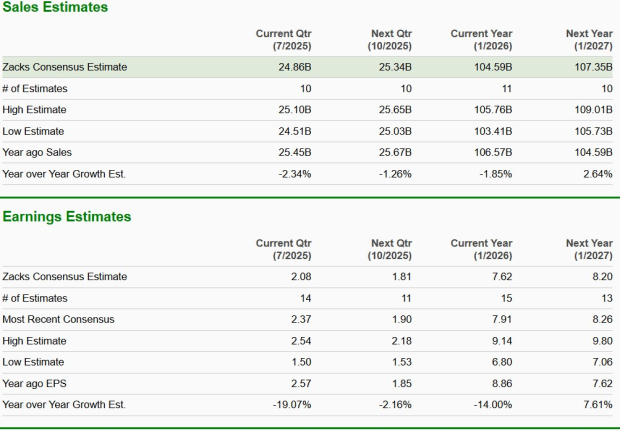

The Zacks Consensus Estimate for Target’s current financial-year sales and earnings per share implies a year-over-year decline of 1.9% and 14%, respectively.

Target currently carries a Zacks Rank #5 (Strong Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| 5 hours | |

| 7 hours | |

| 8 hours | |

| 8 hours | |

| 8 hours | |

| 9 hours | |

| 10 hours | |

| 11 hours | |

| 17 hours | |

| Feb-15 | |

| Feb-15 | |

| Feb-14 | |

| Feb-14 | |

| Feb-14 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite