|

|

|

|

|||||

|

|

|

The AI trade has become something of a consensus on Wall Street. From mega cap tech to speculative startups, nearly every corner of the market is angling for exposure to the next wave of artificial intelligence innovation. Yet despite the mainstream attention, some of the most critical players in the AI boom, Nvidia (NVDA), Taiwan Semiconductor (TSM), and Vertiv (VRT), are still trading at some of their most reasonable valuations in recent history.

What’s more, these aren’t speculative bets. Each of these companies is delivering strong revenue and earnings growth, with forecasts that remain robust well into next year and beyond. While many investors chase the next big AI story, NVDA, TSM, and VRT offer a grounded, but still high-upside path through the AI trade.

Below, we break down why these three names still represent compelling GARP (Growth at a Reasonable Price) opportunities within the AI ecosystem.

Taiwan Semiconductor plays a critical and irreplaceable role in the global semiconductor supply chain, especially when it comes to leading edge artificial intelligence chips. As the world’s largest semiconductor fabricator, TSM is the behind-the-scenes giant enabling advanced computing across industries. In May, the company reported a nearly 40% year-over-year jump in monthly revenue, reflecting surging demand for its cutting-edge AI chips.

Looking ahead, Taiwan Semi expects full-year sales to grow by 28.2% in 2025, followed by another 14.8% gain in 2026. Long-term, earnings are forecast to grow at an impressive 20.8% annual rate over the next three to five years, driven by sustained AI and high-performance computing demand. While TSM currently holds a Zacks Rank #3 (Hold), reflecting stable earnings revisions, the growth trajectory remains firmly intact.

Valuation-wise, the stock trades at 23.1x forward earnings—right in line with its five-year median. For a company of TSM’s strategic importance and growth potential, this multiple appears not just reasonable, but attractive. In a market where many AI plays command stretched premiums, TSM stands out as one of the most compelling large-cap opportunities in the market broadly.

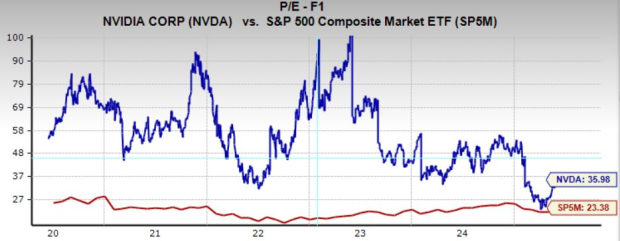

Nvidia remains the undisputed leader in AI hardware design, with its GPUs forming the backbone of nearly every major AI training and inference system in the world. Its dominance in the data center space is unmatched, and the company is already positioning itself for the next frontier—expanding into areas like robotics and quantum computing.

Fundamentally, Nvidia's growth story remains extraordinary. Analysts project earnings to grow at a staggering 28.2% annually over the next three to five years, fueled by unrelenting demand for AI infrastructure. Sales are expected to surge 51.4% this year, followed by another 25.1% gain next year, highlighting both near-term momentum and long-term scalability.

Despite this rapid growth, Nvidia's valuation is far from excessive. Shares currently trade at 36x forward earnings, significantly below the stock’s five-year median of 55x. For a company with Nvidia’s technological leadership, accelerating fundamentals, and global relevance in AI, today represents an opportunity to buy a high-growth compounder at a historically discounted valuation.

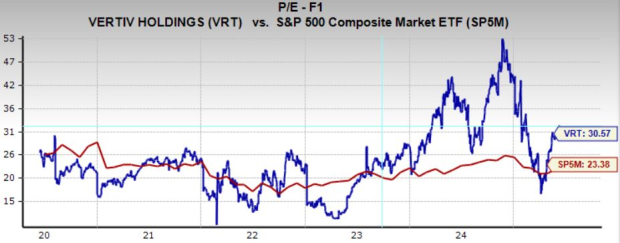

Vertiv has quickly emerged as one of the most important behind-the-scenes players in the AI boom, offering critical power and thermal management solutions for data centers—the physical backbone of the AI revolution. After a sharp but short-lived correction in April, the stock has rebounded strongly as investors refocus on the accelerating demand for data center infrastructure.

Vertiv’s business model is uniquely advantaged. It provides the hardware and services that enable hyperscalers and enterprises to build out AI-ready capacity at scale. With data center spending expected to grow rapidly in the years ahead, Vertiv is well positioned to capture consistent and expanding demand.

Vertiv’s business is firing on all cylinders. Sales are projected to grow in the high teens for each of the next two years, while earnings are expected to rise at a robust 27.2% annually over the next three to five years. Despite its recent run, gaining a dizzying 700% in the last five years, the stock still trades at 30.6x forward earnings, a premium to its five-year median of 23.3x, but justified by its exceptional growth profile. With a PEG ratio just above 1, Vertiv offers a compelling blend of momentum, earnings power, and long-term upside at a valuation that still makes sense.

There are plenty of ways to gain exposure to the AI boom, from speculative software startups to legacy tech names trying to reinvent themselves, but few companies are as essential to the AI supply chain and trade at valuations this grounded. Nvidia, Taiwan Semiconductor, and Vertiv are building the infrastructure to make AI possible.

Each company boasts strong earnings and sales growth, durable competitive advantages, and surprisingly reasonable valuations given their dominance and forward outlook. Whether you're a long-term investor seeking growth or someone trying to avoid the froth of more speculative AI names, these three stocks offer a compelling path to participate in one of the most transformative trends of this decade, and without overpaying for the opportunity.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 6 min | |

| 19 min | |

| 24 min | |

| 41 min | |

| 43 min | |

| 1 hour | |

| 1 hour |

Stock Market Today: Dow Skids As EU Makes Trump Tariff Move; These Gold Stocks Shine (Live Coverage)

NVDA

Investor's Business Daily

|

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 2 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite