|

|

|

|

|||||

|

|

|

While there isn't an official start date marking the artificial intelligence (AI) revolution, I personally like to use Nov. 30, 2022, as my timestamp. This is the day that OpenAI released ChatGPT to the public, virtually changing how businesses and consumers access information at the flip of a switch.

Back then, Amazon (NASDAQ: AMZN) sported a market capitalization of $835 billion. Today, the company's value is almost triple -- hovering at around $2.3 trillion.

While Amazon may not fetch as much attention as its "Magnificent Seven" peers Nvidia or Tesla, the company is quietly building a thriving AI ecosystem -- and Wall Street is finally starting to take notice. Last month, investors learned that billionaire hedge fund manager Bill Ackman initiated a stake in Amazon through his investment firm, Pershing Square Capital Management.

Let's explore how Amazon is integrating AI across its various businesses. More importantly, I'll analyze the recent price action in the stock to help make the case for why I think Amazon is positioned to become Wall Street's first $5 trillion stock.

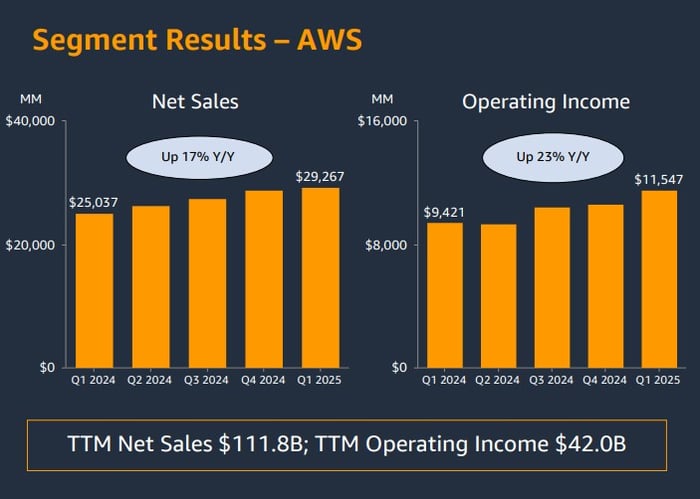

The most obvious area of Amazon's ecosystem that has benefited from the AI boom so far is the company's cloud computing segment, Amazon Web Services (AWS). Over the last couple of years, AWS has invested billions into a start-up called Anthropic, which competes with OpenAI. Throughout this partnership, AWS has witnessed notable revenue acceleration combined with significant expansion in operating margins.

Image source: Investor Relations.

This is an important notion to understand, as AWS accounts for the majority of operating profits across the entire Amazon ecosystem. Thanks to a successful partnership with Anthropic so far, Amazon now has even more financial flexibility, which it can parlay into other AI-powered services.

For instance, Amazon is also testing various forms of AI robotics in its fulfillment centers, which could theoretically bring new levels of efficiency and automation to processes previously managed by human labor.

Lastly, Amazon is also developing its own custom chipsets -- dubbed Trainium and Inferentia. In the long run, these could be more opportunities for Amazon to complement its existing hardware business while entering new markets to compete more directly with existing semiconductor designers.

Image Source: Getty Images.

As of this writing (June 11), Amazon's stock has declined by roughly 1% on the year. While that might initially come across as uninspiring, consider how sharply shares have rebounded since bottoming out at around $167 in April.

It's my suspicion that Ackman took advantage of the sell-off last month and bought the dip. I bring this up because, interestingly, Pershing Square's Amazon position was not included in the fund's 13F filing for the first quarter. Rather, Ackman's Amazon position became publicly reported following news of a call he held with his investors.

The chart below benchmarks Amazon's market cap growth relative to several of its Magnificent Seven peers since the release of ChatGPT. I purposely excluded Apple and Tesla from this analysis, as I don't see much in the way of direct competition to Amazon.

AMZN Market Cap data by YCharts.

There are a couple of notable takeaways from the trends above.

First, Amazon's valuation has risen considerably more than those of both Microsoft and Alphabet over the last couple of years. This is significant because both companies compete fiercely with Amazon in the cloud computing market, specifically. I see this as a potential signal that investors may be more bullish on Amazon's ability to maintain an edge in the cloud landscape, despite intensifying investments in AI infrastructure from the competition.

In addition, it's clear that Nvidia has been the best Magnificent Seven investment throughout the AI revolution thus far. But as I alluded to above, Amazon actually has a unique opportunity to begin competing with Nvidia through the introduction of its new chipsets.

In my eyes, Amazon has a strong foundation to continue accelerating revenue and profit growth for the long run. Despite already achieving a monster run over the last couple of years, I think investors will continue to place a premium on Amazon stock relative to its peers, leading to further valuation expansion in the years to come.

For these reasons, I believe Amazon's current trajectory supports the idea that the company could see a more than twofold rise in market cap and reach a $5 trillion valuation before its peers.

Before you buy stock in Amazon, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Amazon wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $653,702!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $870,207!*

Now, it’s worth noting Stock Advisor’s total average return is 988% — a market-crushing outperformance compared to 172% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of June 9, 2025

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool's board of directors. Adam Spatacco has positions in Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

| 54 min | |

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 4 hours |

Nvidia Stock Builds Bullish Base, Tests Key Support Level With Earnings Seen Soaring 70%

AMZN

Investor's Business Daily

|

| 4 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, backtesting, and much more.

Learn more about FINVIZ*Elite